30 APRIL 2020

NOT ALL LOWER FOR LONGER CREATED EQUAL

- Recent IMF government bond yield projections underline the impact of central banks’ Covid-19 induced quantitative easing policies and confirm that our assumption of lower for longer government bond yields remain relevant.

- Not all lower for longer yields are created equal as shown by the elevated excess spreads over German government bonds for some of Europe’s peripheral countries, confirming that investors are now pricing in risk more carefully.

- While investors reprice risk more carefully, real estate excess spreads over high yield corporate bonds have turned negative. However, they remain well below GFC and euro-crisis levels and might normalize if the ECB follows the FED and expand into purchasing high yield bonds.

- In direct real estate, investors have demonstrated disciplined pricing for secondary offices and retail compared to post GFC, as excess spreads required for secondary over prime assets have not returned to their record-low 2007 levels and are unlikely to do so in the coming years.

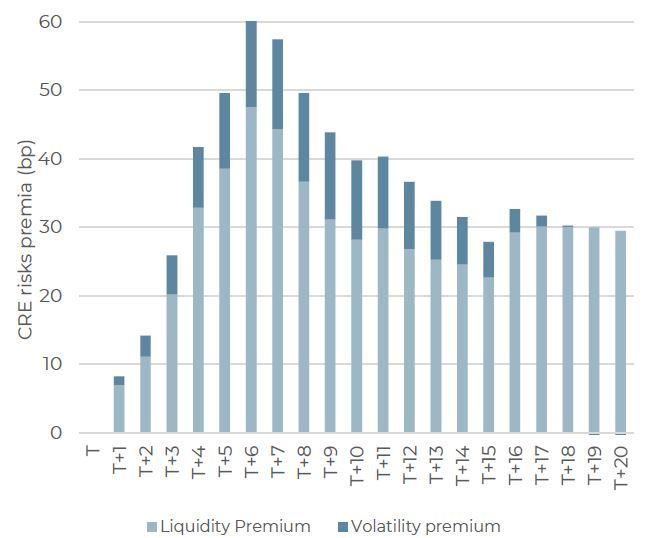

- Property yields will be impacted by investors requiring higher risk premiums for lack of liquidity and increased volatility immediately after a crisis. After the GFC, we estimated an increase of 60bp over the first six quarters, eventually settling down to below 30bp after 15 quarters following the start of the crisis.

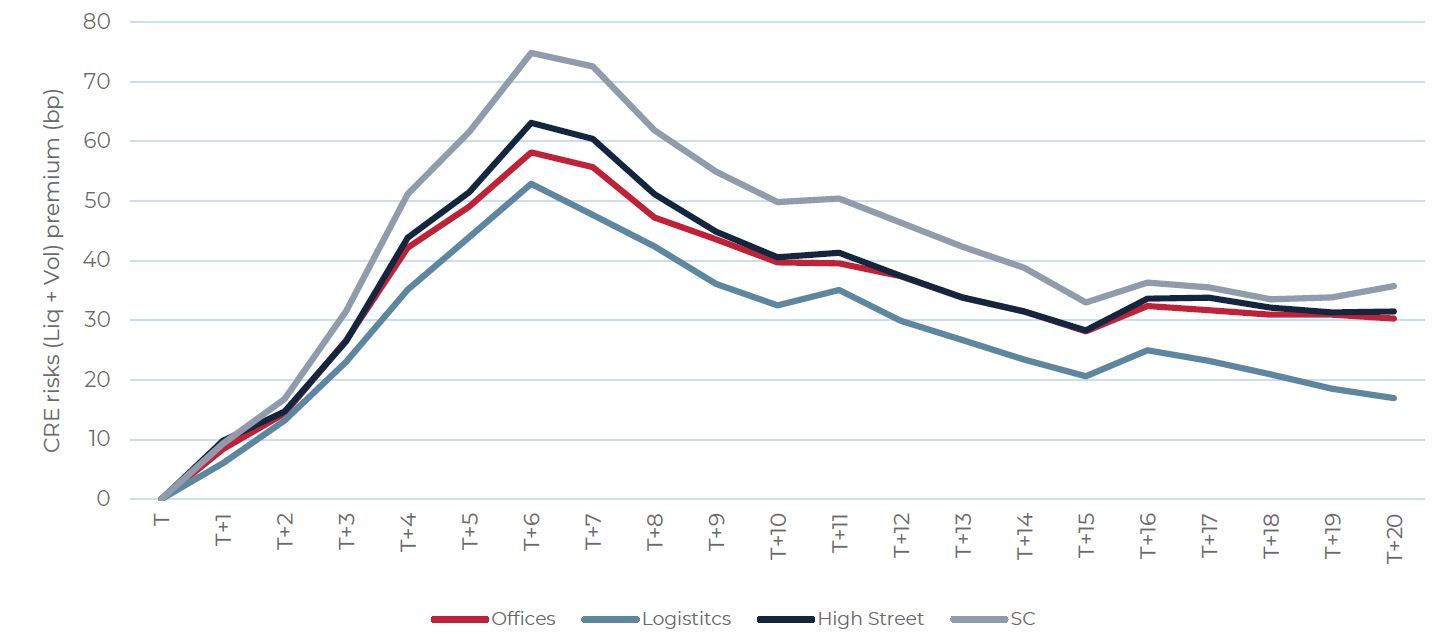

- Risk premia behaved differently among the sectors, as shopping center risk premia spiked the most and remained ahead of the other sectors, while logistics widened by 50bp before coming down to just below 20bp.

PROPERTY SECTOR LIQUIDITY AND VOLATILITY RISK PREMIA SINCE 2008 (T = QUARTER SINCE MARKET PEAK)

Source: RCA, CBRE, AEW

LOWER-FOR-LONGER BOND YIELDS ARE HERE TO STAY

- The ECB has been much quicker than with the GFC to respond to the Covid-19 crisis as it announced in quick succession €120bn and €750bn emergency bond purchasing programs to ensure monetary stability, keeping interest rates low in the Eurozone since mid March.

- The ECB will also offer loans to banks at the lowest interest rate ever (-0.75%). These new quantitative easing policies are the basis for our assumption that government bond yields will remain lower for longer, despite some widening in peripheral jurisdictions.

- With eligibility criteria for bond purchasing shifting to include below investment-grade corporate bonds, corporate yields will further settle down as well.

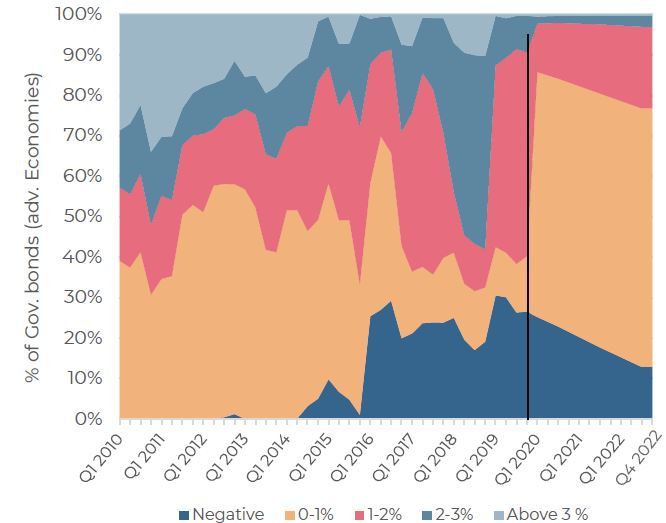

- Recent IMF analyses across advanced economies confirms this lower for longer assumption. At year-end 2019, the IMF reports that over 40% of outstanding government bonds have a below 1% or negative interest rate. This is forecast to increase to over 85% in Q1 2020, before coming down to 77% by year-end 2022.

Government bond yields of advanced economies

Sources: IMF, AEW

NOT ALL LOWER-FOR-LONGER YIELDS ARE CREATED EQUAL

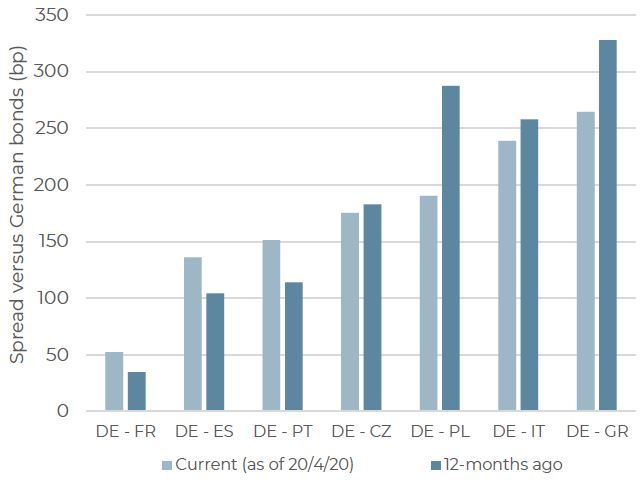

- As fixed income investors price in both the impact of Covid-19 and the recently announced over €850bn ECB emergency bond purchasing programs, we do note some bond yield widening in peripheral jurisdictions, like Spain, Italy, Portugal and Greece. This means that with the purchasing program only re-started 3-4 weeks ago the final impact on peripheral yields remains uncertain.

- Based on current pricing, it is clear investors are pricing in near 250bp excess spreads for Greek and Italian over German government bonds. Both are down from a year ago.

- Polish and Czech excess spreads over German bonds are around 175bp, both down from last year – especially in Poland. On the other hand, excess spreads of Spanish and Portugese over German government bond yields are close to 150bp, both up from their 12-month historical levels. French excess spreads are also up but remain relatively low at 50bp.

- All of this confirms that investors are pricing in risk more carefully at the moment and that not all lower-for-longer yields are created equal.

10yr Government bond yield spreads

Sources: Bloomberg, AEW

NEGATIVE EXCESS SPREAD OVER HIGH YIELD BONDS BELOW GFC

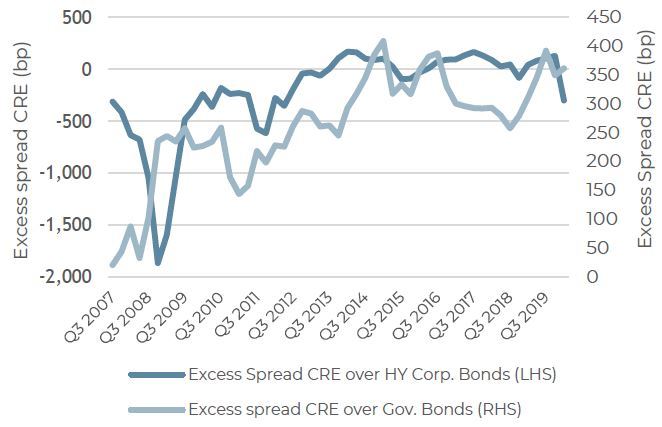

- As we highlighted in our first Covid-19 Flash report on 18-Mar-20, Euro high yield corporate bonds have widened out in response to the virus outbreak, as investors anticipate an increase in defaults and losses.

- Current Euro high yield corporate bond spreads are unlikely to reflect this week’s expanded eligibility criteria for the ECB repo funding program, which now include the acceptance of below investment-grade corporate bonds as collateral. If the ECB will follow the FED in actually buying high yield corporate bonds, it can be anticipated that this will tighten bond spreads in the future.

- Regardless of where Euro high yield corporate bond spreads will eventually end up after the policies are fully implemented, the excess spread for real estate investors has now turned negative at -300bp. This is a reversal from the last 7-8 years. However, this relative pricing signal is still well below what the 2008 GFC and even the 2011 Euro-crisis showed.

Property spreads over government and corporate bonds

Sources: Federal Reserve Economic Data, Bloomberg, CBRE, AEW

SECONDARY EXCESS SPREADS DIVERGE FOR OFFICES AND RETAIL

- If we expand our analyses from prime into secondary property, we note that investors have shown disciplined and divergent pricing for secondary offices and retail assets compared to prime since the GFC. As shown in our chart, excess spread required for secondary over prime assets have not returned to 2007 levels.

- In fact, only in offices has there been some normalisation of secondary excess spreads across the eight countries covered by the CBRE data series.

- Interestingly, we did see that secondary shopping centres showed strong repricing from 2013 to 2015. However, have since then showed a massive increase in secondary excess spreads to catch up with high street retail. This is mostly due to impact of e-commerce on non-prime shopping centres, which are unable to replace tenants with F&B or other lifestyle tenants.

Prime vs secondary property yield spread

Sources: CBRE, AEW

PAST SPIKES IN RISK PREMIA SETTLED DOWN AFTER 6 QUARTERS

- Taking a closer look at historical investor pricing for prime assets, we estimate liquidity and volatility premiums since the outbreak of the GFC. Based on the same scientific methodologies applied in our risk-adjusted return approach, investors required an increase of 60bp in yields, as a result of reduced liquidity and increased total return volatility following the GFC.

- As highlighted in previous reports, our estimate for the liquidity premium is tied to actual historical trading volumes anchored by London offices. The volatility premium is based on total return volatility over the period relative to the overall European universe.

- However, as the crisis matured and solutions were found for overleveraged asset situations, the required risk premia came down to below 30bp after 15 quarters. We note the brief reversal as a result of the Euro-crisis in the 16th quarter.

- Given that most institutional real estate investors have a long term horizon, short term volatility in yields is unlikely to raise big concerns. Assuming government bond yields remain lower for longer for at least the next five years, a similar to GFC 30bp risk-premium driven increase in yields is unlikely to have a big impact on total returns over the entire five year forecast period.

Average liquidity and volatility premia since 2008

Sources: RCA, CBRE, AEW

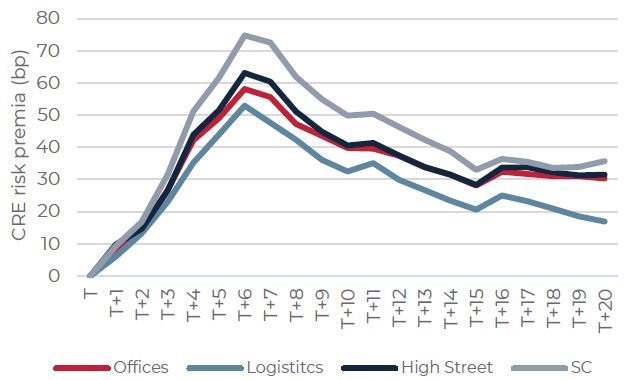

SECTOR-SPECIFIC RISK PREMIA MIGHT DIVERGE MORE IN FUTURE

- Broadening our risk premium analyses from an average all prime property across each of the sectors, pricing of liquidity and volatility risks for offices, logistics and retail assets since the outbreak of the GFC was fairly consistent.

- As shown in our chart, estimated risk premia for shopping centers spiked most and still remain ahead of the other sectors. This reflects the lack of liquidity in this sector compared to pre-GFC.

- In fact, logistics has shown the fastest normalisation of risk premia, from 50bp at the peak to back down to just below 20bp after five years. This reflects the secular change as logistics has matured as an investment sector and is aided by stronger occupier fundamentals.

Property sector liquidity and volatility premia since 2008

Sources: RCA, CBRE, AEW

READ THE FULL REPORT

The information and opinions presented in this research piece have been prepared internally and/or obtained from sources which AEW believes to be reliable; however, AEW does not guarantee the accuracy, adequacy, or completeness of such information.