- Despite its well documented political problems, Italy remains the fourth largest economy in Europe. Italian government bonds have more recently tightened to historical lows and are now more in line with the rest of Europe, helped by the ECB’s quantitative easing policy and a solid domestic base of private investors.

- Across office, retail and logistics markets, Italy has shown the most attractive returns compared to other European markets over the last five years. However, our forecasts for the next five years are less optimistic with further recovery in capital values limited by our outlook on bond yields, with Italian returns expected to be broadly in line with the rest of Europe.

- Investment volumes have been increasing since 2012 and are estimated at €8bn for 2019. Italian volumes have been at 5% of the European total over the last five years, just below the 5.5% share of Spain. Offices made up 60% of Italian volumes and cross-border investors had a comforting high share of 67% over the last five years.

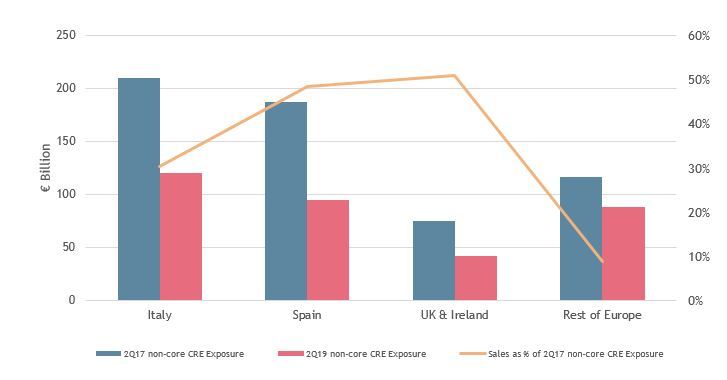

- At €120bn, Italian non-core loan exposure remains the highest of any single EU country. Italian NPL sales have been slower than Spain’s and other high NPL countries; this delay means that there are still more NPL sales to be done. The related second order sales of former NPL collateral across Italy will offer value add and core investors further liquidity in the upcoming years.

- Finally, Italian offices offer strong diversification benefits for UK, German and French investors, based on historically low covariance’s between Italian office market returns compared to other key European markets. Fund managers have not yet taken advantage of this diversification benefit as only c. 5% of Pan European fund strategies target Italy.

MORE ITALIAN NPL DEAL VOLUMES WILL TRIGGER MORE LIQUIDITY DOWN THE LINE

Sources: Evercore & AEW

The information and opinions presented in this research piece have been prepared internally and/or obtained from sources which AEW believes to be reliable; however, AEW does not guarantee the accuracy, adequacy, or completeness of such information.