Is new development an imminent risk for European offices?

Over-supply of new office space has posed significant challenges for European investors in the past. New development of office space is typically planned at times of low vacancy rates and abundant availability of debt finance. Due to the time needed to develop new office properties, many of these new developments would be delivered at a time when demand for space has already slowed. This has historically resulted in the ‘typical’ market cycle of increased vacancy rates and declines in market rents. In this report, we look at the imminent risk of new development to trigger such a down cycle in rents in the short term. We do this by considering granular historical data on land acquisitions for new development and investment transactions of existing office buildings for purposes of redevelopment and conversions across the eight gateway European office markets. In addition, we compare this bottom-up analysis with the historical trends and forecasts of aggregate stock data.

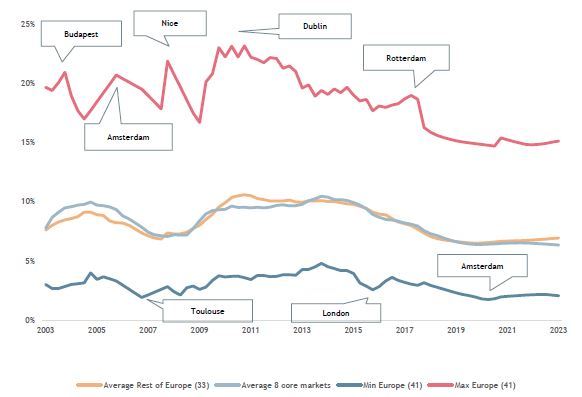

MODERATE DEVELOPMENT LOWERS VACANCY RATES FOR EIGHT GATEWAY OFFICE MARKETS IN NEXT FIVE YEARS

Source: CBRE & AEW

EXECUTIVE SUMMARY:

- In past cycles, increased development activity has been a precursor for increased vacancy and declining rents.

- Current transaction and lending trends show a mixed picture on new development. Development lending as a percentage of lenders’ total book has increased to 13% in both the UK and Germany, despite only a 6% share of development-related deals in total European office sector volumes.

- Our new bottom-up estimate of office stock is a leading indicator of new office space to be delivered to the market as measured by the traditional top-down approach.

- Despite a near doubling from the last five years, our forecasts for office stock growth for the next five years remain at only about half the actual levels seen in the five years leading up to the GFC, with non-gateway markets showing stronger development growth.

- Net absorption of office space across all our 41 markets is forecast at about 5mn square meters p.a., about half the level of 2003-07. This is due to a slowdown in employment growth in the next five years, as many markets have reached full capacity.

- With supply and demand projected to be broadly in balance, average vacancy rates across both the eight gateway and 33 non-gateway markets are projected to be at all-time lows at 6.5% and 6.7%, respectively.

- As a result, our forecasts for prime rental growth in the next five years for both the gateway and non-gateway markets are at 2.8% and 2.0% p.a., respectively. In line with historical trends, the average hides more extreme movements for individual markets.

The information and opinions presented in this research piece have been prepared internally and/or obtained from sources which AEW believes to be reliable; however, AEW does not guarantee the accuracy, adequacy, or completeness of such information.