EUROPEAN RETAIL: THE GOOD, THE BAD AND THE UGLY

- Retail spending for 2021-22 is forecasted to grow at 4% pa amid consumers’ pent-up demand. This implies that the worst might be over for retailers and investors, although the precise speed of the recovery might vary with vaccine distribution rates.

- In a reversal from the recent trend, e-commerce penetration rates are projected to come down in 2021. Although the vaccines should allow for a return to in-store shopping, e-commerce penetration rates are unlikely to drop to pre-Covid levels.

- The restaurant, health and clothing segments were the most negatively impacted during the lockdowns. But are also expected to see the strongest 2021-22 rebound. Grocery stores were the most resilient during the lockdowns and are forecasted to show low stable growth.

- As the final lockdowns are lifted in the first half of 2021, it is reasonable to expect footfall to recover similarly to what was observed during the 2020 non-lockdown periods. European shopping centres and retail parks showed the strongest rebounds, while UK retail park footfall proved to be the most resilient throughout 2020.

- UK rent collections showed tenants inability to pay rent as a result of the lockdowns, with the evictions moratorium exacerbating the problem. This triggered lease restructurings which are likely to assure a sustainable rent and better collection in a post-Covid environment.

- Lockdowns and store closings have hit European prime rents by 16%-20% for high street retail and shopping centers. Once the restrictions are eased, we expect a stabilisation of prime headline rents and a revival of credit quality amongst tenants.

- European REIT investors re-priced retail REITs over the last 6 months to a discount of 16% to NAV, a similar level as for office REITs. Investors still expect headwinds, albeit at reduced risks. This confirms that the very worst for retail might be behind us.

- Despite Covid-19 triggering yield widening of 10-35 bps across most prime retail segments, further yield widening should remain limited due to lower-for-longer government bond yields and the recent REITs pricing signal.

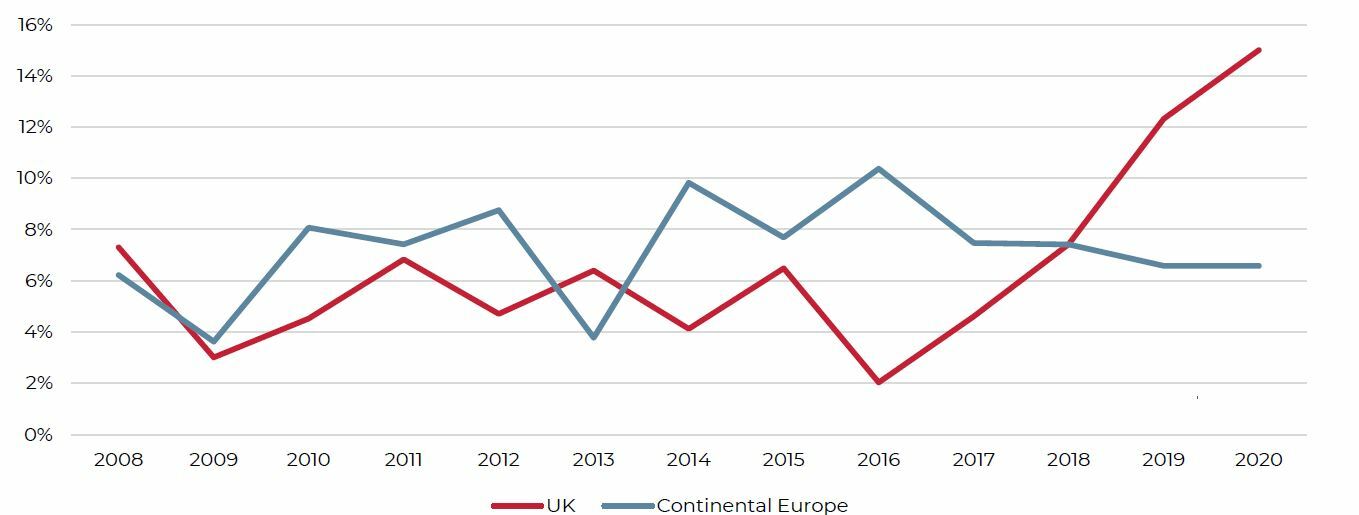

- Excess yield spreads for both secondary UK shopping centers and high street retail reached new highs in 2020 and are much higher than in the rest of Europe.

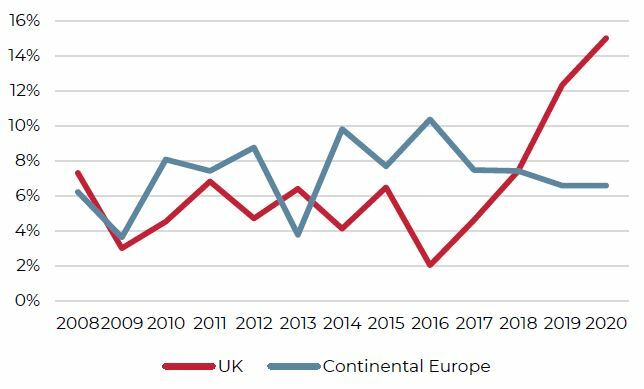

- As a result, the UK share of shopping center acquisition deals for the purpose of conversion, redevelopment and renovation has increased significantly over the last years and is much higher than for Continental Europe.

SHARE OF SHOPPING CENTER DEALS FOR CONVERSION, REDEVELOPMENT AND RENOVATION (2008-20)

Sources: RCA, AEW Research & Strategy

STRONG RETAIL SPENDING REBOUND PROJECTED

STRONG 2021-22 POST-COVID RETAIL SPENDING REBOUND EXPECTED

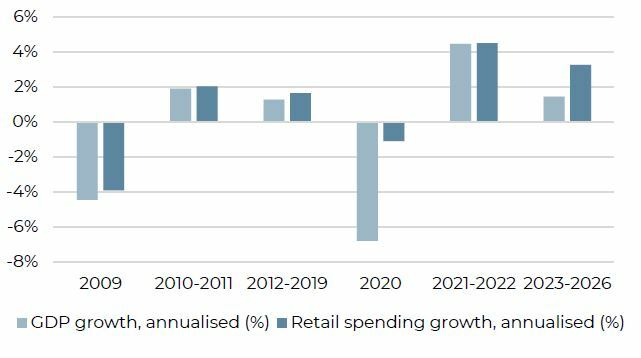

- The near 7% GDP decline in the Eurozone as a result of the Covid-19 pandemic has been well documented. In some countries, like the UK, Spain and France the declines were in the 8-10% range and worse than in the aftermath of the global financial crisis (GFC).

- Retail spending has been resilient in 2020 despite the pandemic, which is a testament to the wide range of government support policies ensuring incomes and employment as well as central banks keeping interest rates low during the Covid-19 crisis.

- As most household savings have increased during the lockdown, consumers are likely to have pent-up spending demand. In fact, the forecast for retail spending for the 2021-22 period stands at over 4% pa, in line with the Eurozone GDP growth and better than after the GFC (2010-11).

- Based on these forecasts, it is clear that the worst might be over for retailers and investors.

Eurozone real GDP and retail spending growth pa (2009-26)

Sources: Oxford Economics, AEW Research & Strategy

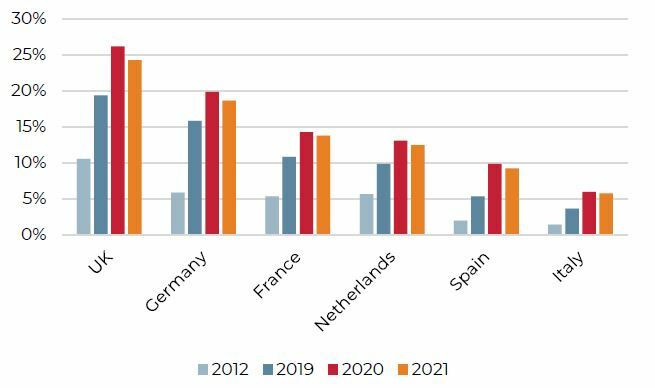

E-COMMERCE PENETRATION EXPECTED TO SLOW POST-COVID

- E-commerce has steadily increased its share of retail sales since the GFC. After doubling between 2012-2019 in most European countries, online sales penetration rates surged in 2020 amid Covid-19 lockdowns.

- As the vaccines allow for consumers to return to in-store shopping, e-commerce penetration rates are projected to come down in 2021. Despite this reversal from recent trend, they are expected to remain above pre-Covid levels. From 2022 onwards, ecommerce penetrations rates should resume their increase, albeit at a slower pace.

- Since most European governments will be more heavily indebted post-Covid, they are increasingly likely to finally become serious in properly taxing e-commerce platforms and levelling the playing field for in-store retail.

- Returned goods has hurt pure e-commerce platforms’ profitability while omni-channel retailers will be better positioned to deal with these.

- Consequently, traditional retailers should see a boost to in-store sales in 2021-22 allowing them time to optimise their store networks and implement their omni-channel strategies.

Online sales as % of total retail sales - Post-Covid Forecasts

Sources: eMarketer, AEW Research & Strategy

STRONGEST REBOUND PROJECTED FOR WORST COVID-19 SECTORS

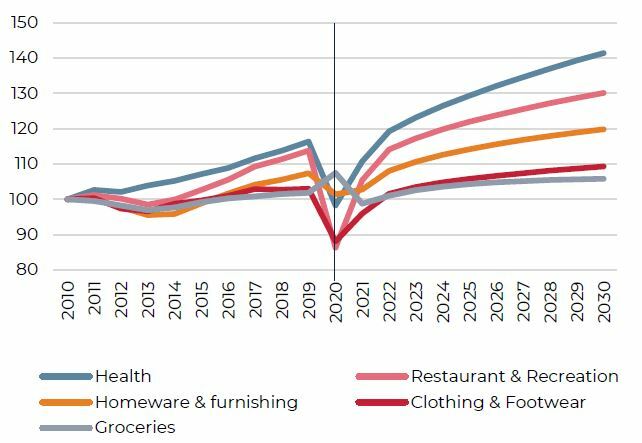

- Unsurprisingly, restaurants and entertainment retail spending was impacted most severely during the Covid-19 pandemic, followed closely by clothing & footwear and pharmacy & health.

- Grocery stores were the only retail segment that actually showed an increase in sales during the pandemic. Although with increased Covid-19 related costs, profitability of grocery retailers might not have improved as much as the top line sales growth suggest.

- Going forward, Oxford Economics projects a return to the long term pre-Covid trend growth across the various retail segments after 2022.

- This means that sales are expected to see the strongest 2020-21 rebound in the restaurant, health and clothing sectors followed by homewares. Grocery store sales are forecast to return to a stable but low growth.

Eurozone growth in spending – indexed by retail segment (2010 = 100)

Sources: Oxford Economics, AEW Research & Strategy

STRUGGLING OCCUPIERS LOOKING TO RESET RENTS

FOOTFALL TRENDS CONVERGE IN FINAL STAGE OF LOCKDOWNS

- After the hopefully final round of lockdowns, high frequency footfall data from CBRE Calibrate shows convergence at 20-25% of Feb-20 levels across a sample of 300 UK and near 300 Continental European retail locations.

- This is with the notable exception of UK retail parks (RPs), which have stabilised at 55%. European RPs showed strong resilience over the summer, but have come in line with high street retail (HSR) and shopping centers (SCs)

- UK HSR and SCs have shown continued relative weakness, but stabilised over the last month. Oversupply of space, weakening UK retailers and a higher dependency on (international) tourist spending might be driving factors.

- Continental SC footfalls beat Feb-20 levels during non-lockdown periods and should improve similarly once final lockdowns get lifted.

Footfall across sample of European retail locations (7-day moving average)

Sources: CBRE Calibrate, AEW Research & Strategy

COVID-19 RENT COLLECTIONS TRIGGER LEASE RE-STRUCTURINGS

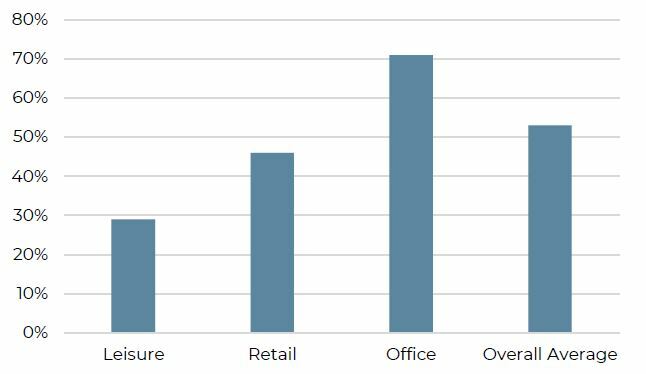

- UK retail rent collections received before their due date were reported at 46% as of year-end 2020, not far behind the 53% all sector average .

- This 53% average is a significant improvement compared to 38% as of Jun-20, when the immediate impact of the first lockdown was being felt.

- Still it shows the dramatic impact of the Covid-19 pandemic as 2019 all sector rent collections were reported at 79% on their due date.

- These data prove Covid-19’s lockdowns impacted negatively on tenants’ ability to pay rent, further exacerbated by the government’s moratorium on tenant evictions.

- On a positive note, these rent shortfalls triggered lease restructurings which should assure sustainable rental levels and better tenant-landlord alignment through percentage of sales rent clauses putting the post-Covid recovery on a sustainable footing.

UK rent collections on due date as of Dec-20

Sources: Remit Consulting Ltd., AEW Research & Strategy

PRIME RETAIL RENTS HIT HARD BY COVID-19 IN 2020

- European high street retail posted 9% pa rental growth with 4% for shopping centers, in 2012-15, ahead of offices and logistics at about 1% each.

- After a UK-driven spike in 2015, prime rental growth started turning negative for shopping centers in 2019.

- Shopping centers were hit harder by the growing share of online sales, as most (inter-)national retailers shifted up from quantity to quality.

- As a result, many retailers opened or expanded (flagship) stores in central locations, supporting prime high street rental growth, albeit at a slower pace.

- However Covid-19 lockdowns and mandatory store closings hit 2020 prime rents hard for both high street retail (-16%) and shopping centers (-20%).

- Many retailers' revenues dropped in 2020 with many forced to rightsize their stores or some going out of business, especially in the UK.

- As the Covid-19 crisis is resolved, we expect re-openings to improve cash rent collections, a revival of credit quality amongst tenants and a stabilisation of prime headline rents.

Prime rental growth for high street retail and shopping centres – European average (7 countries, index 100 = 2016)

Sources: CBRE, AEW Research & Strategy

INVESTORS STARTING TO FOCUS ON CONVERSIONS

RETAIL INVESTMENT VOLUMES TRENDING DOWN

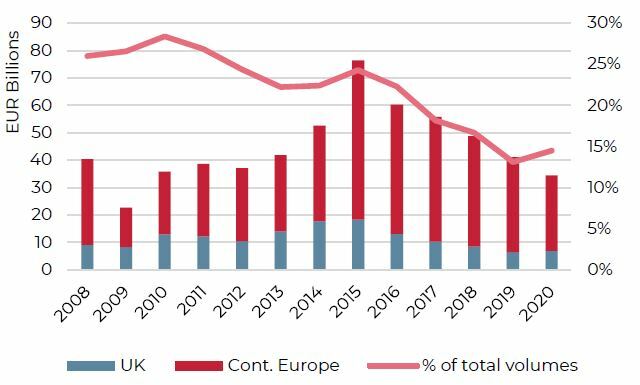

- Continuing its downward trend, 2020 investment transaction volumes for Europe, including the UK came in at EUR 33bn, less than half the EUR 77bn record volumes in 2015. But 2020 European volumes are still similar to those recorded in the 2008-13 period.

- It should be noted that UK retail volumes have not moved differently from the rest of Europe regardless of the 2016 Brexit referendum.

- Despite an uplift in 2020, the retail share of overall investment volumes has halved over the 2008-20 period from near 30% to 15%.

- Over the coming years, it is reasonable to expect a stabilisation of retail transaction volumes. If one assumes a holding period of five years, investors that bought retail in the 2015 peak year are likely to consider potential sales from 2021 either to take profit or to limit losses if LTV restrictions make refinancing difficult.

European retail investment volumes (2008-20)

Sources: RCA, AEW Research & Strategy

GROCERY ANCHORED RETAIL AMONG THE MOST RESILIENT SECTORS

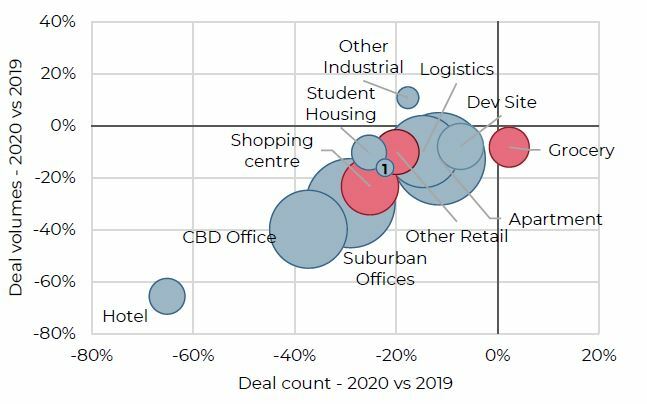

- European investment volumes declined by 25% compared to 2019 for all sectors. But there was a wide range of changes across sectors from -8% for development sites to -66% for hotels.

- Surprisingly retail investment volumes held up better than offices both in EUR bn volumes (-19% vs -35% respectively) and in deal counts (-23% and -32% respectively).

- This strong retail resilience can be explained by the fact that retail volumes have already been on a downward trends since 2015, whereas office volumes set a new record in 2019. Moreover, the sales of large portfolios and corporate acquisitions boosted 2020 retail volumes.

- Among the retail segments, grocery anchored retail assets saw the slightest drop in volumes and it is the only property type for which the number of deals increased in 2020. This positive trend also reflected in the yields movements described in the following page.

- On the other hand, both due to Covid-19 restrictions and the on-going restructuring of the retail sector, shopping centers saw the biggest drop both in deal counts and volumes.

Investment Volumes and Deal count per sector - 2020 vs 2019 (size: 2020 investment volumes)

1= Senior housing. Sources: RCA, AEW Research & Strategy

RETAIL REITS NOW PRICED AT SIMILAR DISCOUNT AS OFFICE REITS

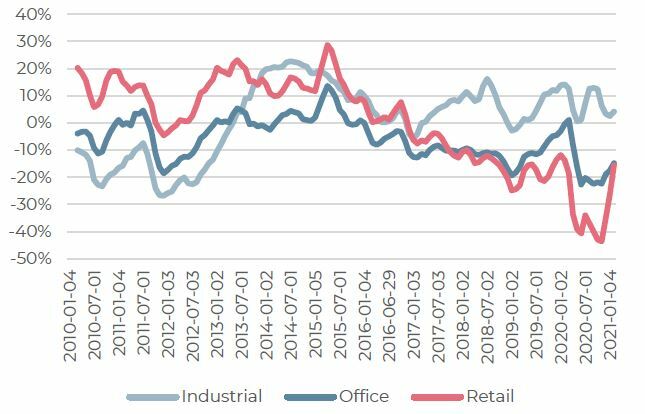

- Despite continued poor news flow on the Covid-19 lockdowns and its impact on retailers, European REIT investors have recently re-priced retail REITs. In fact, discounts to NAV for retail REITs are now similar to those for office REITs.

- This re-pricing reflects a combination of changes in stock prices as well as property valuations, where the current observed discount to NAV for retail is near 16%, according to Green Street. This means that the implied value of the REITs underlying assets is 16% above the implied company value (net of leverage) as priced by stock trading in the secondary market

- Clearly REIT investors are also expecting a strong post-Covid-19 recovery in retail spending, retail sales and leasing. Retail REITs still trade at discounts so investors still expect headwinds albeit at reduced risks.

- This price signal from the public markets can be seen as confirmation that the worst might be behind us for the broader European retail investment sector.

European REIT sectors’ observed premiums to NAV (2010-21)

Sources: Greenstreet, AEW Research & Strategy

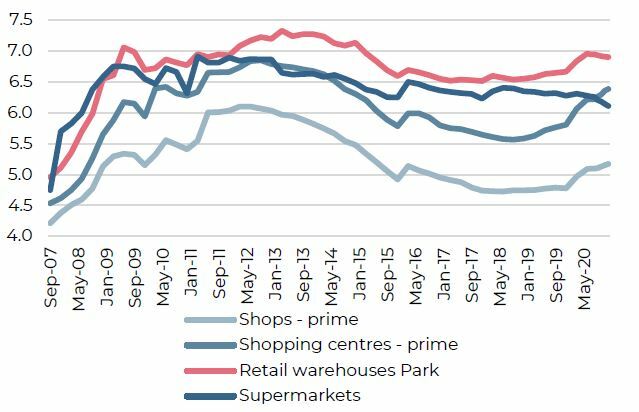

RETAIL EXPECTED TO BE PAST WORST OF REPRICING

- Most retail sub-sectors had been repricing pre-Covid, with yields trending upward since 2018. But, the Covid-19 pandemic has accelerated this yield widening ranging across segments from 7-33 bps over 2020.

- Despite this recent repricing, retail prime yields still remain below their 2012-13 post-GFC peak as of Q4 2020.

- Supermarkets were the only exception as prime yields reached a new post 2011 record low. This can be explained by the limited impact of Covid-19 on grocery sales as essential retailers were allowed to remain open.

- It would be reasonable to assume that prime retail repricing will now remain limited with the expected lower-for-longer bond yields for the foreseeable future and the attractive pricing at discount to NAV.

- Secondary retail assets on the contrary might experience still stronger repricing as already highlighted by the increasing spread between prime and secondary yields seen since the beginning of the year.

Prime yields across sub-sectors (historical) %

Sources: CBRE, AEW Research & Strategy

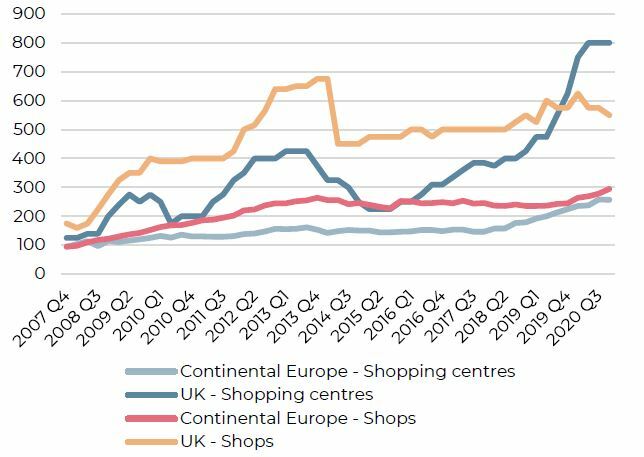

ELEVATED SECONDARY YIELD SPREADS, WITH UK AHEAD OF EUROPE

- Excess yields for secondary retail over prime are showing similar upward trends in the UK and Continental Europe despite variations in magnitude.

- Secondary UK shopping centers (SC) reached a record high 800 bps excess spread in 2020. Secondary UK high street retail shops (HSR) are at 550 bps, well below their 675 bps 2014 peak.

- Occupational weakness in secondary UK centers has been well documented, with many secondary owners likely in breach of financial loan covenants. This means many secondary centers are not getting badly needed and increasing capex allocations further eroding collateral values.

- Across pan-European secondary SC and HSR excess yield expansion has been much more muted compared to the UK reaching 300 bps in 2020.

- If the rest of Europe follows the UK, this could mean that worse is to come. However, this would not be consistent with historical trends. Also, the average retail space per capita in the UK is likely higher than in most of the rest of Europe.

UK and Continental European excess secondary yield spreads over prime (2007-20)

Sources: CBRE, AEW Research & Strategy

UK CONVERSIONS & REDEVELOPMENTS SHOW THE WAY FORWARD

- The share of shopping center acquisitions for the purpose of conversion, redevelopment and renovation could offer an additional reason for Continental European secondary yields not to follow the same upward trend as in the UK.

- The higher and more stable share of conversion and redevelopment deals in Europe up to 2018 shows investors’ more steady commitment to update existing centers compared to the UK.

- More attractive secondary UK yields have triggered this increase in shopping center transactions focusing on conversions etc. This shows that distress does offer attractive opportunities to investors able to make these changes. Useful for UK owners as well as across Europe.

- It is unlikely that all these transactions are focused on a complete change of use to residential, urban logistics or offices. But innovative owners will likely look to reduce the existing retail component and create attractive mixed-use places, especially post-Covid.

Share of shopping centre deals for conversion, redevelopment and renovation (2008-20)

Sources: RCA, AEW Research & Strategy

The information and opinions presented in this research piece have been prepared internally and/or obtained from sources which AEW believes to be reliable; however, AEW does not guarantee the accuracy, adequacy, or completeness of such information.