LIGHT INDUSTRIAL BENEFITS FROM STRONG LOGISTICS MOMENTUM

- With many investors focusing on large scale logistics warehouses, we examine in this report the fundamentals of the smaller scale light industrial and urban logistics markets.

- After doubling its share of total retail sales between 2012 and 2019, Covid-19 further boosted e-commerce sales growth during the lockdowns. Consequently, more urban logistics is needed to deal with the growing number of parcels and to provide faster and more affordable services.

- In addition, Europe is experiencing a 4th industrial revolution focusing on high value-add industrial production, triggering an increased need for modern and flexible light industrial space close to highly-skilled workers.

- Scarcity of land together with strong demand should provide a solid driver for high land values and sustainable rental growth for some time to come for urban logistics and light industrial (re)-developments.

- In response to the traditional scepticism on light industrial tenant quality, we have confirmed both the diversity and average credit score (BB) across a large sample of such tenants. This is in line with other property types and should not prove a hurdle.

- Although lockdowns had some impact on industrial take up, the German, French and Dutch markets proved resilient after reaching a near-record 17.4 million sqm in 2019.

- Unsurprisingly prime rents for light industrial are ahead of logistics as it comprises smaller buildings with a higher office component and located in more dense urban locations. In addition, rental growth for light industrial over the 2015-20 period has been broadly in line with strong growth in prime logistics rents.

- Prime yields for light industrial across the German, French and Dutch markets have come down by 220bps over the last five years to reach 5.3% at mid-year 2020.

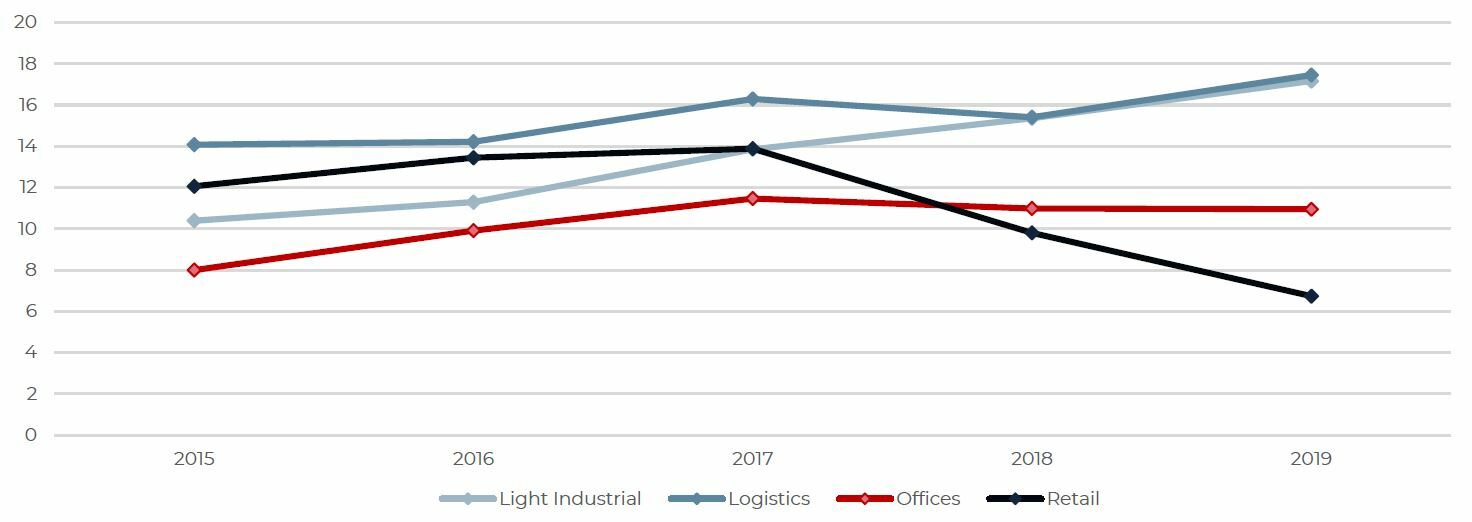

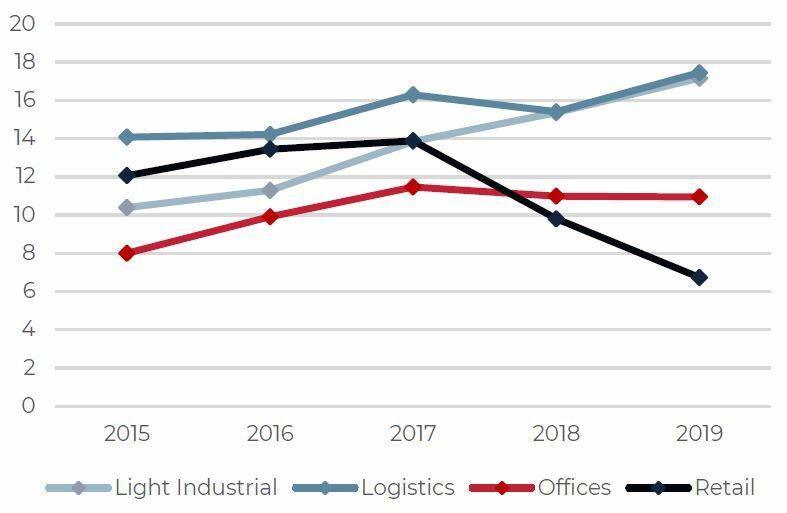

- Surprisingly, prime light industrial returns across the three most established Western European markets are in line with prime logistics for both 2018 and 2019. Since 2017, light industrial returns have been ahead of both offices and retail.

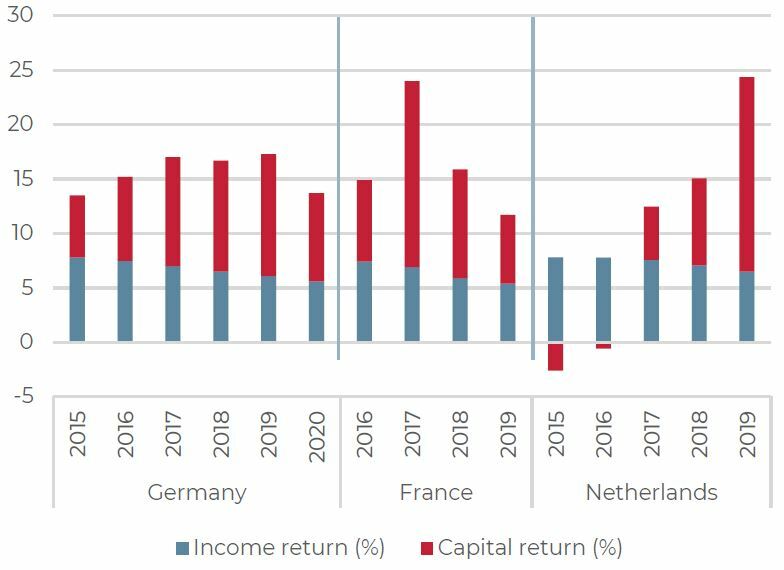

HISTORICAL TOTAL RETURNS IN GERMANY, FRANCE AND THE NETHERLANDS (3-YEAR ROLLING AVERAGE)

Sources: CBRE, JLL, Bulwiengesa, AEW Research & Strategy

SOLID FUNDAMENTALS

E-COMMERCE INTENSIFIES NEED FOR URBAN LOGISTICS SPACE

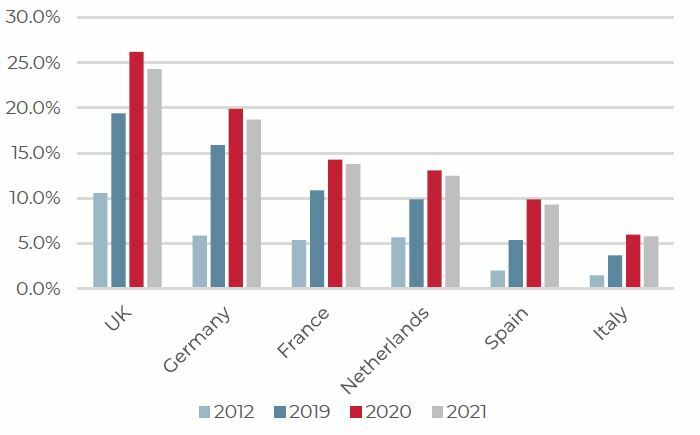

- E-commerce has steadily increased its share of retail sales since the GFC. After doubling between 2012-2019 in most European countries, online sales penetration rates surged in 2020 due to Covid-19 lockdowns.

- This happened both in well-established e-commerce markets such as the UK and Germany as well as in countries with lower e-commerce use.

- Penetration rates are expected to come down a bit in 2021, as the vaccines allow for consumers to return to normal patterns. But they should remain ahead of pre-Covid levels, as many new habits will last and mobile app-powered sales will continue to support the e-commerce expansion.

- Consequently, more logistics networks are needed to deal with the growing number of parcels and to provide faster and more affordable delivery services.

- These fundamentals drive demand for logistics space up, especially for units located close to consumers near Europe’s main urban centres.

Online sales as % of total retail sales – Historical actuals and post-covid forecasts

Sources: Centre for Retail Research, eMarketer, AEW Research & Strategy

4th INDUSTRIAL REVOLUTION DRIVES DEMAND FOR MODERN LIGHT INDUSTRIAL SPACE

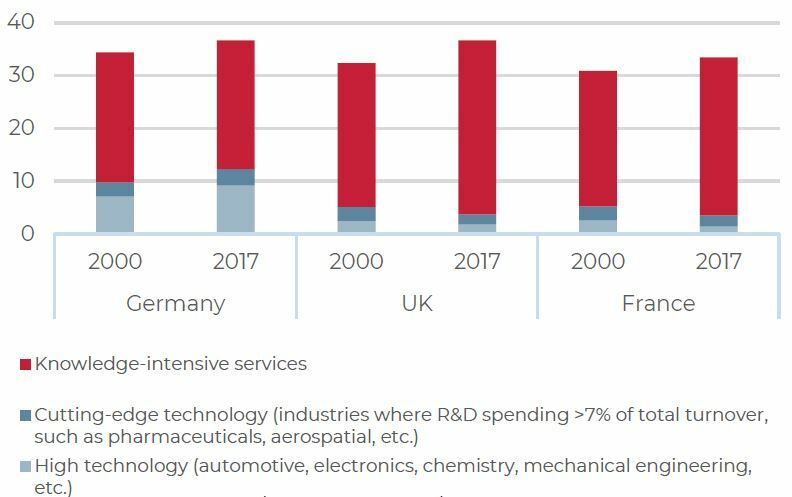

- The 4th industrial revolution currently under way combines digitalised and automated production with the increased need for flexible and customised processes.

- The Covid-19 crisis emphasised the challenges associated with supply chain risk management. Delivery times suffered from global supply chain disruption and highlighted the need to locate closer to consumers, especially for strategic sectors such as medical supplies.

- Nevertheless, reshoring of manufacturing activities will certainly not signal a complete reversal of past trends, as labour costs remain high in Europe.

- Also, the European reindustrialisation is more focused on high value-add industrial and knowledge-intensive services, as highlighted on the chart.

- Apart from skilled labour, manufacturing businesses will therefore also need more modern light industrial and flexible space located in areas with high quality supporting infrastructure, such as fast data access, affordable energy supply and efficient transport.

High value-add industries and knowledge-intensive services as % of total GVA, 2000 & 2017

Sources: OECD, Eurostat, EU Klems & AEW Research & Strategy

LAND SCARCITY DRIVING LAND VALUES AND RENTS UP

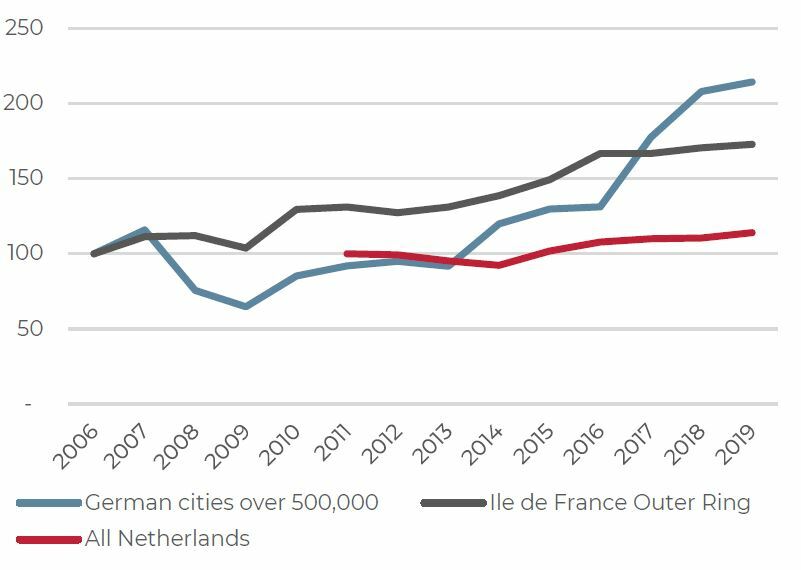

- Increasing urbanisation and a further tightening of already long-standing restrictions on new land developments have been pushing land values up, as illustrated in this chart.

- In addition, new regulations to reduce congestion and the environmental impact of large trucks in city centres are also pushing demand for smaller urban logistics and light industrial parks. This upward-trending demand for light industrials and urban logistics is therefore projected to continue.

- The scarcity of available land can be expected to intensify and is likely to perpetuate an already chronically under-supplied land market in the future.

- Continued land scarcity should provide a strong driver for high land values and justification for higher rents for light industrial and urban logistics.

- Growing rents will progressively allow urban logistics and light industrial projects to compete with other building types where permitted.

Land values in France, Germany and Netherlands, Index 100 = 2006 (Fr, Ger) & 2011 (Nl)

Sources: Deutsche Statistische Bundesamt, Observatoire Regional du Foncier, Kadaster, AEW Research & Strategy

STRONG OCCUPIER MARKET DYNAMICS

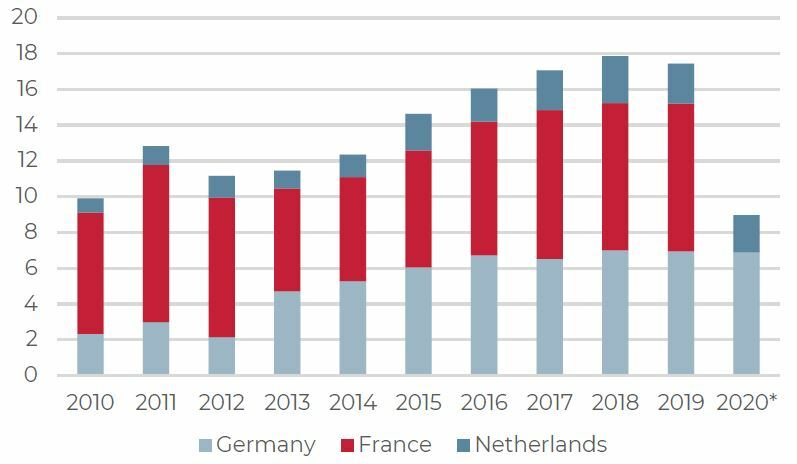

LONG-TERM GROWTH IN INDUSTRIAL TAKE-UP

- All industrial take-up across the German, French and Dutch markets reached 17.4 mn sqm in 2019, well-above the 10-year average of 14 million sqm and down marginally from 2018 historical high of 18 million sqm.

- Covid-19’s impact has proven limited on 2020 German and Netherlands take-up, respectively down by 1% and 7% compared to 2019.

- In France, light industrial take-up, excluding logistics, accounts for 46% of all industrial take-up over the 2010-2019 period.

- German industrial real estate has historically been dynamic, benefitting from the country’s historical leadership in Europe’s manufacturing output.

- Take-up in the Netherlands has been growing modestly as a result of limited availabilities, with the vacancy rate across Amsterdam, Rotterdam and Utrecht markets reaching 2.2% in 2019, an historical low.

- In fact, vacancy rates are near historical lows in Germany and France also.

Annual industrial take-up (million sqm) – 2010-2020

Sources: CBRE, AEW Research & Strategy

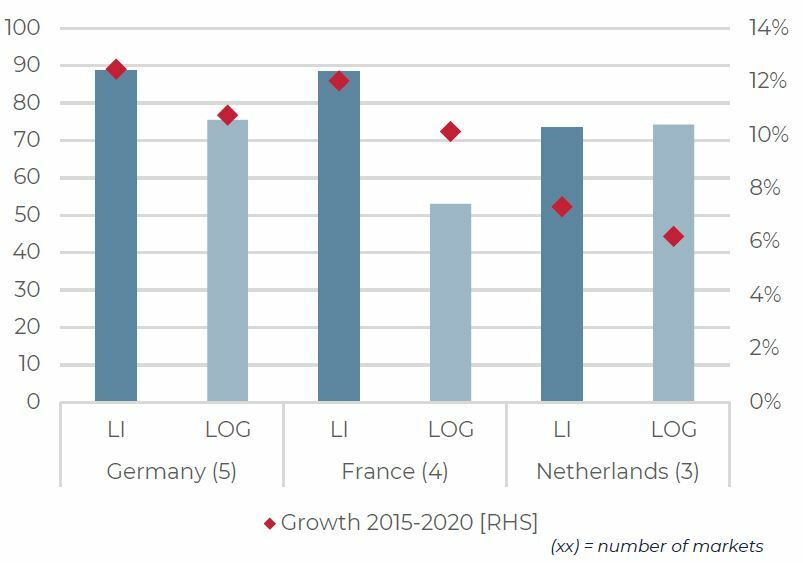

LIGHT INDUSTRIAL RENTS AHEAD OF LOGISTICS

- It should be no surprise that prime rents for light industrial are above those for logistics, as light industrial buildings are generally smaller with a higher office component and located in more dense urban areas with more intense competition from other uses.

- Light industrial average prime rents stands at €89/sqm/pa in France and Germany and at €73/sqm/pa in the Netherlands.

- For both Germany and France, light industrial rents are ahead of logistics rents, with the Dutch market being the notable exception.

- The larger gap between light industrial and logistics rent recorded in France when compared to other countries might be explained by its overall lower urban density on a national level allowing for lower logistics rents.

- Prime light industrial rental growth over the 2015-20 period across the three markets outpaced prime logistics rental growth during the same period. Prime rental growth recorded in Germany and France reached 12% for light industrial and 11% for logistics. In the Netherlands, prime rental growth was 7% for light industrial and 6% for logistics, which is stronger than most sectors.

Light industrials (LI) vs logistics (LOG) prime rents (€/sqm/year) - Q2 2020

Sources: CBRE, BNP RE, JLL, AEW Research & Strategy

DIVERSIFIED LIGHT INDUSTRIAL TENANTS SHOW AVERAGE CREDIT RISK

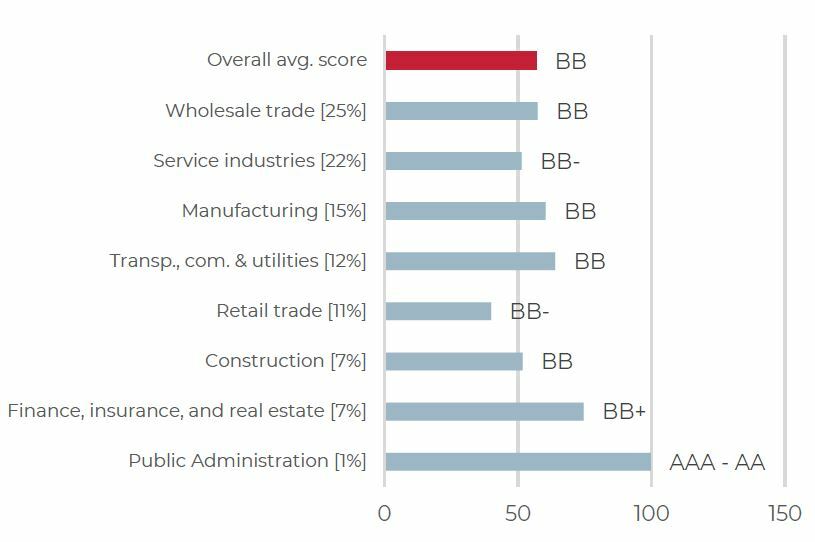

- To address traditional investors’ concerns on poor light industrial tenant quality, we gathered a sample dataset of 1,000 light industrial tenants in June 2020 and analysed the credit scoring of each tenant together with consultants Income Analytics and credit data provider D&B.

- Our analysis showed an average BB equivalent bond rating, which corresponds to a default probability of 0.7% over the next 12 months, in line with tenants in other sectors. It should be noted that default probability does directly not equate to ability to pay rents.

- Despite the BB average, still 42% of the tenant sample has an investment grade equivalent bond rating.

- A wide range of industries are presented in our light industrial property tenant sample although transportation and logistics dominate at around 47% of the dataset. This provides diversification benefits, as these assets tend to be multi-let and supports the sustainability of income returns.

- Finally, the loss severity of a tenant default is always less significant than the loss severity of a defaulting corporate bond, since a defaulting tenant can always be replaced with another tenant.

Industry categories and share of total sample of light industrial tenants [%] & average credit score

Sources: INCANS, D&B, AEW Research & Strategy

AN EMERGING INVESTMENT MARKET

LIGHT INDUSTRIAL YIELDS REMAIN WELL AHEAD OF LOGISTICS

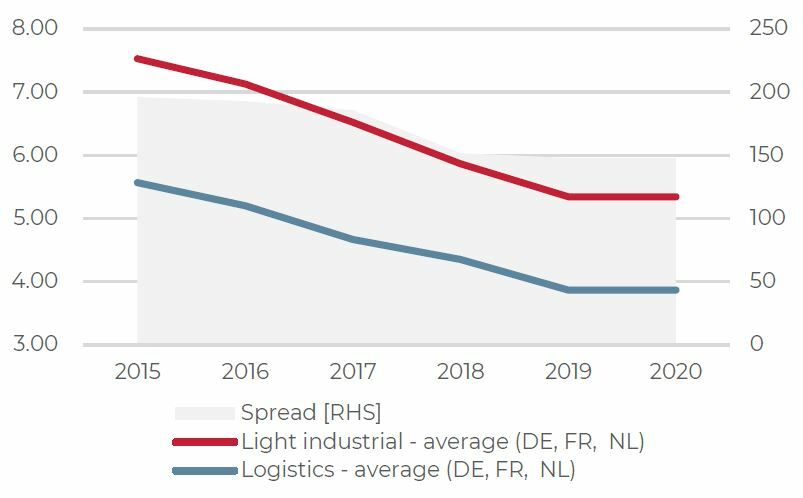

- With strong tenant demand for space and record low bond yields, prime yields for light industrial across the German, French and Dutch markets have come down by 220bps from 7.50% in 2015 to 5.30% at mid-year 2020.

- By contrast, prime logistics yields came down by 170 bps from 5.60% to 3.90% over the same period.

- This means that on an absolute basis the excess yield spread for prime light industrial has come down from 190bps to 150bps over the last five years.

- On a relative basis, as a percentage of the current prime logistics yield, this excess spread has in fact increased from 34% to 38%.

- If we accept the UK is a more mature market with a smaller yield spread, and that continental European markets will follow its lead, we can expect further yield tightening.

Light industrial vs logistics yield (%) and spread (bps)

Sources: CBRE, JLL, AEW Research & Strategy

DIVERSIFICATION OFFERS BENEFITS TO LIGHT INDUSTRIAL INVESTORS

- When considering the historical income and capital returns for light industrial across the three countries, it should be noted that the German figures show less volatility. This is partly due to the fact that they contain a larger number of German markets (100+) when compared to France (4) and Netherlands (3).

- Dutch data on light industrial returns confirms the two years of capital value declines in 2015-16 being offset by near 25% total returns in 2019.

- Going forward more modest capital returns can be expected. But, regardless of the different cyclical patterns of historical returns across these three national light industrial markets, portfolio diversification should offer benefits to investors over time.

- In the end, light industrial offers good stable income returns due to its diversified tenant base and multi-let nature.

Comparison of light industrial income and capital return per country

Sources: CBRE, JLL, Bulwiengesa, AEW Research & Strategy

LIGHT INDUSTRIAL RETURNS IN LINE WITH LOGISTICS

- Prime light industrial returns across the three key countries under review are in line with prime logistics for both 2018 and 2019. Since 2017, light industrial returns have been ahead of both offices and retail. We suspect that this will come as a surprise to many investors, not consciously considering light industrials previously.

- As highlighted above, light industrial benefits from solid fundamentals, such as the rapidly increasing share of e-commerce and the reindustrialisation trend. These drive up tenant demand for light industrial space across a number of different industry sectors.

- As a result, take up of industrial space has exceeded 15 million sqm pa in the three main markets during the 2017-19 period. Due to the limited Covid-19 impact on 2020 take-up, based on available data to date, it would not be unreasonable to expect a rebound in 2021.

Historical total returns in Germany, France and the Netherlands (3-year rolling average)

Sources: CBRE, JLL, Bulwiengesa, AEW Research & Strategy

The information and opinions presented in this research piece have been prepared internally and/or obtained from sources which AEW believes to be reliable; however, AEW does not guarantee the accuracy, adequacy, or completeness of such information.