WHAT WILL BE THE EFFECT OF THE EXPECTED PROPERTY YIELD WIDENING?

In absolute terms, European real estate has appeared expensive for the last year, as indicated by record low yields across all four property types. But, with government bond yields at record lows, there is still a significant excess return investors are making to take risk in real estate. Also, despite increasing trade frictions and political uncertainty, the economic recovery is expected to continue, albeit at a modestly slower rate. This is expected to trigger further rate hikes from the Fed and other central banks pushing out government bond yields in the next five years to levels more in line with historical averages. Based on this background, we launch our risk-adjusted return approach to answer the challenging question posed by many: What will be the effect of the expected property yield widening?

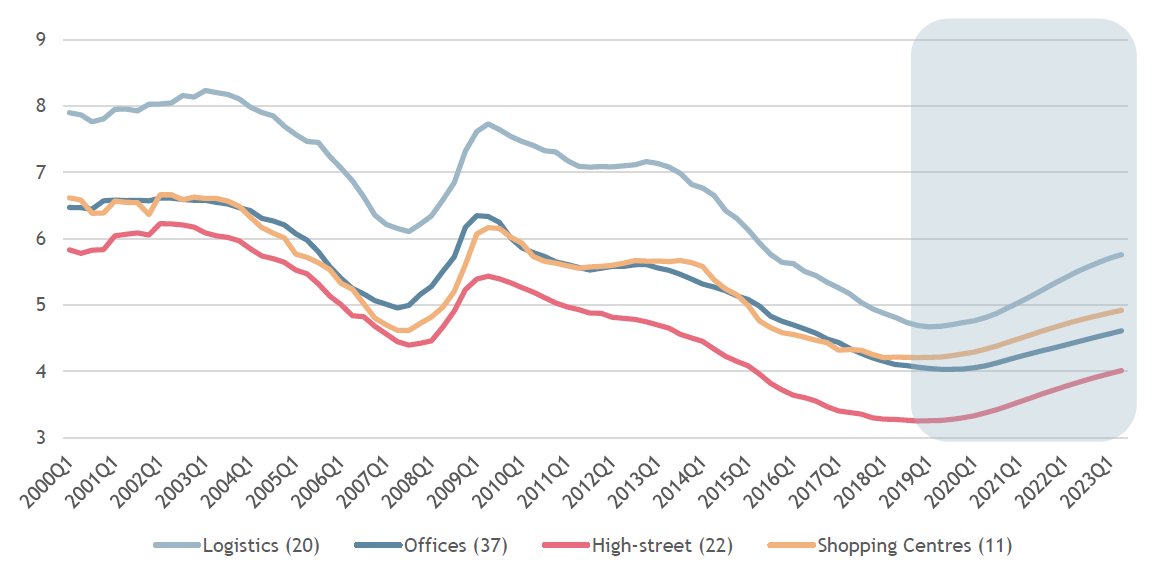

HISTORICAL (2000Q1-2018Q2) AND FORECASTED (TO 2023Q2) PRIME YIELDS PER PROPERTY TYPE (QTLY)

Source: CBRE, Natixis & AEW

EXECUTIVE SUMMARY: MORE THAN HALF OF MARKETS NEUTRAL OR ATTRACTIVE

- After a period of ever tightening property yields, bond yield normalisation is expected to push out prime property yields confirming the current late cycle stage of the European real estate markets.

- Elevated overall debt levels leave major western economies vulnerable to these widely anticipated interest rate increases, even though the macro-economic recovery has gathered force and continues for now.

- Our new risk-adjusted returns approach identifies opportunities across 90 European real estate markets by comparing the expected to the required rate of return for each market. Our back testing shows that this approach has given appropriate signals in previous market cycles.

- Given the solid momentum in most occupier markets and projected prime market rent growth, our approach identifies 51 of the 90 covered markets as neutral or attractive, despite the anticipated yield widening.

- Attractive individual asset acquisitions remain available even in less attractive markets as stock picking remains a key driver of portfolio or fund level performance.

- Finally, we expect less dramatic downside in the coming years as real estate-specific debt levels remain modest and new supply of space relatively limited compared to previous cycles.

WATCH THE VIDEO

READ THE FULL REPORT

The information and opinions presented in this research piece have been prepared internally and/or obtained from sources which AEW believes to be reliable; however, AEW does not guarantee the accuracy, adequacy, or completeness of such information.