COVID-19 SPECIAL UPDATE: LOGISTICS & OFFICES RESILIENT

- As economists adjusted their economic growth forecasts down, it seems inevitable that most leading European economies will enter recession in 2020. To place the current uncertain situation in a relative context, we present three different scenarios:

- Base case scenario which is based on the Jan-20 economic assumptions before Covid-19;

- New base case which applies the Mar-20 consensus forecast of a V-shape recovery;

- Downside scenario at -8% Eurozone 2020 GDP growth, +5% in 2021 and a convergence towards the long term average after 2021.

- As Covid-19 forced stock markets down and pushed out both corporate and government bond yields, central banks announced significant interest rate cuts and bond purchasing programmes, which have stabilised financial markets to some degree. To reflect these policies and their increased long term necessity, we use swap-implied government bond yields in the downside scenario.

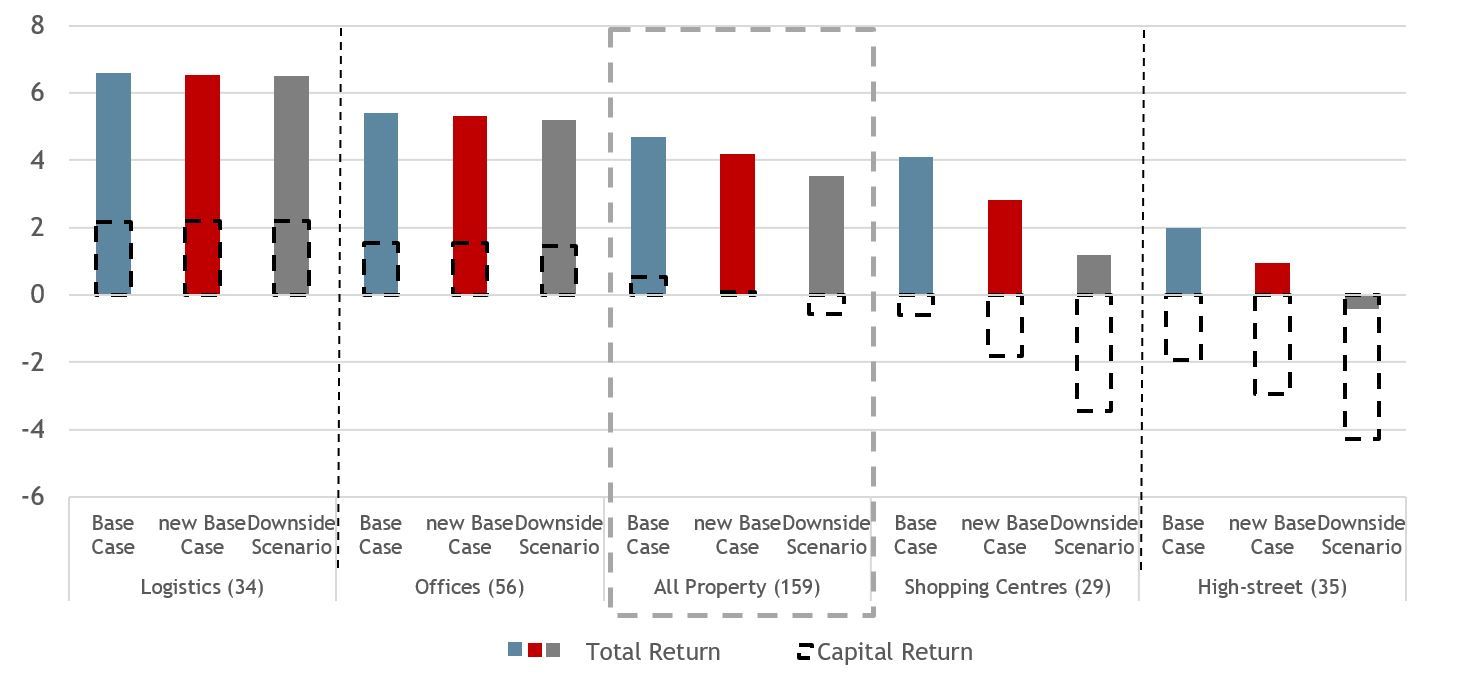

- Significant declines in prime rental growth rates for all sectors are expected, which move down from 1.6% p.a. in our January base case to only 0.5% p.a. in the new base case and -0.8% p.a. in the downside scenario based on our simplified approach. Prime retail rent growth gets hit significantly more than office and logistics as it has proven to be more than double as sensitive to past GDP growth changes.

- Our prime property yields in the downside scenario are based on swap-implied 10-year government bond yields. Given the current high excess yield and historical delay in which prime property yields adjust to bond yield changes this means that in the downside scenario property yields are, on average, holding steady. In fact, office and logistics yields are projected to remain more robust.

- Our new base case and downside scenarios show all property total returns of 4.2% and 3.5% p.a. respectively. Prime retail is more impacted due to the low yields and larger market rental declines. In contrast, total returns for prime logistics (6.5%) and offices (5.2%) stay much more resilient in the downside scenario as lower rental growth is offset by yield tightening.

ALL PROPERTY RETURNS SHOW RESILIENCE IN NEW BASE CASE & DOWNSIDE SCENARIOS OVER 5 YEARS

Sources: CBRE, Natixis, Bloomberg & AEW

READ THE FULL REPORT

Watch the English webcast here

The information and opinions presented in this research piece have been prepared internally and/or obtained from sources which AEW believes to be reliable; however, AEW does not guarantee the accuracy, adequacy, or completeness of such information.