28 MAY 2020

EUROPEAN CAPITAL VALUES NOT IMMUNE TO COVID-19

- In this fourth update since the onset of the Covid-19 crisis, we update and combine some of our initial thoughts about the impact of the lockdowns and expected restrictions going forward.

- To quantify the short term impact on prime capital values across our European market coverage, we built upon our previous risk premia work and introduce two new scenarios (May-20 L-Shape and May-20 V-Shape) which reflect more refined analyses and additional data.

- Our three key assumptions across our recent and new scenarios are:

- Declines in market rents due to the COVID-19 are expected to impact contracted rents over time;

- Loss of received cash rents are seen to affect 2020 income from COVID-19 related rent concessions to tenants (Retail -18%, Offices -6% and Logistics -4%);

- Increases in initial yields in 2020-21 amid higher risk premia but less severe than during the GFC.

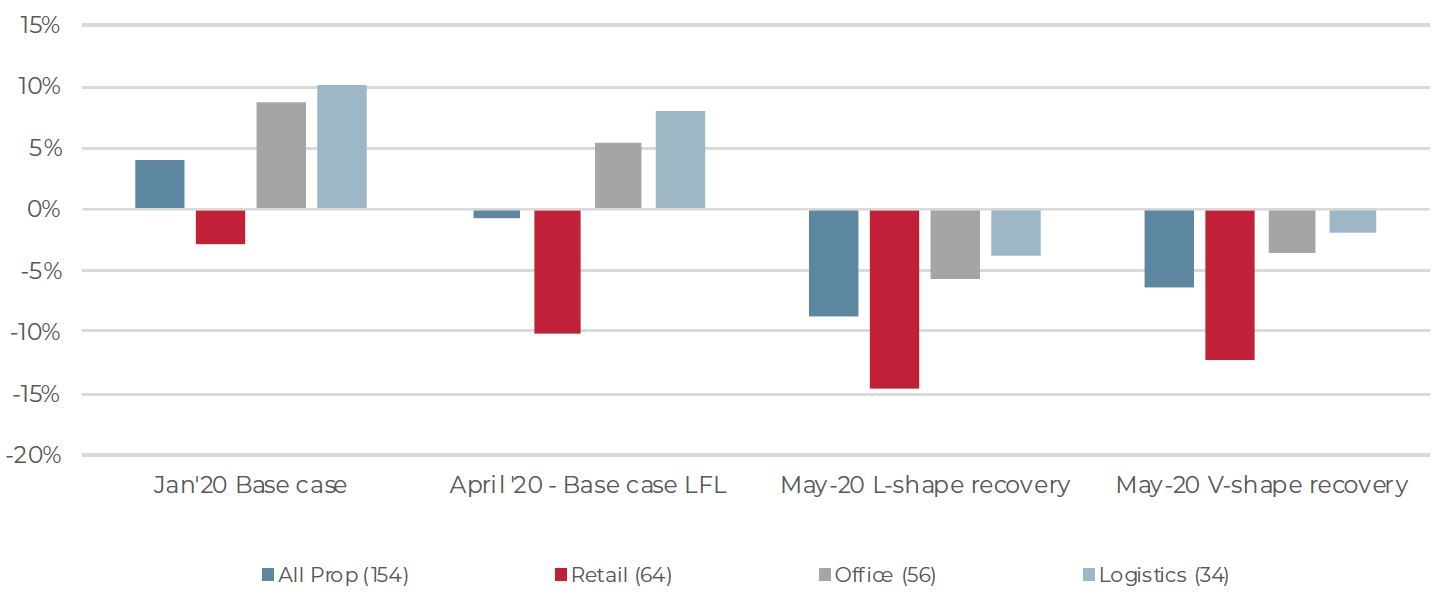

- The cumulative 2020-21 value impact for prime property across all sectors in our L-shape scenario is estimated at -9%, consisting of -15% move in 2020 offset by a 7% recovery in 2021.

- Our V-shape scenario shows a cumulative value impact of -6% across all asset classes over the two years, consisting of a more dramatic decline of -19% in 2020 offset by a strong 15% recovery in 2021.

- Consistent with our previous COVID-19 updates, the all property results are driven largely by the poor results in retail, which is predicted to have a 12-15% downside in capital values for 2020-21.

- Prime offices and logistics are expected to have much less downside in the two year period across the L and V-shape scenarios at -4-6% and -2-4%, respectively.

CUMULATIVE 2020-21 PRIME CAPITAL VALUES UNDER VARIOUS SCENARIOS (NUMBER OF MARKETS PER SECTOR IN BRACKETS)

Sources: RCA, CBRE, AEW

COVID-19 RELATED RENT CONCESSIONS TO IMPACT CASH INCOME DISTRIBUTION

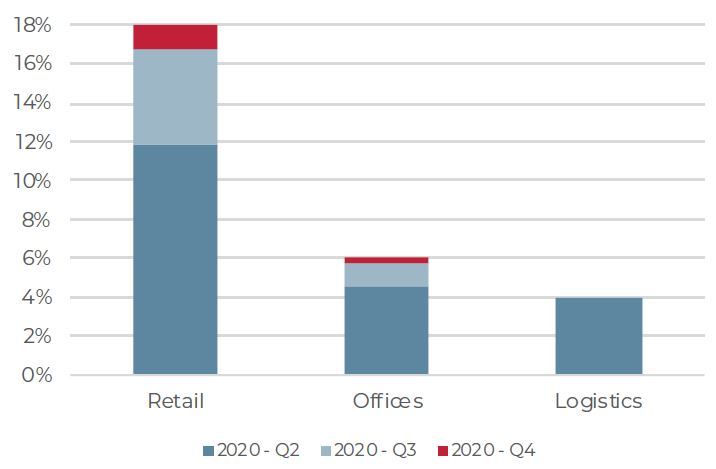

- Real estate asset owners are faced with possible income shortfalls amid the COVID-19 pandemic as rent concessions to tenants such as rent-holidays, deferrals and re-negotiations of rent (especially in retail) put pressure on the ability of investors to collect all income.

- To estimate this shortfall of income, we estimate cash shortfalls by sector as the percentage of income that will remain unpaid in 2020. This percentage is based on discussions with brokers and desk research focusing mainly on preliminary rent collection figures for the second quarter (Retail 50%, Offices 70-80%, Logistics 80-90%).

- As shown in our chart, retail (high-street and shopping centre) is expected to have the highest cash shortfall at 18%, while for offices and logistics shortfalls are much lower at 6% and 4%, respectively. In addition, the second quarter of 2020 is expected to show the highest percentage of shortfalls. However, as the COVID-19 crisis evolves the impact of rental defaults in the last 6 months is expected to decrease as lockdowns get lifted.

Cash shortfall by sector (% of total income)

Sources: CBRE, BNP, NAREIT, AEW

INCREASE IN INITIAL YIELDS, BUT LESS THAN AFTER GFC

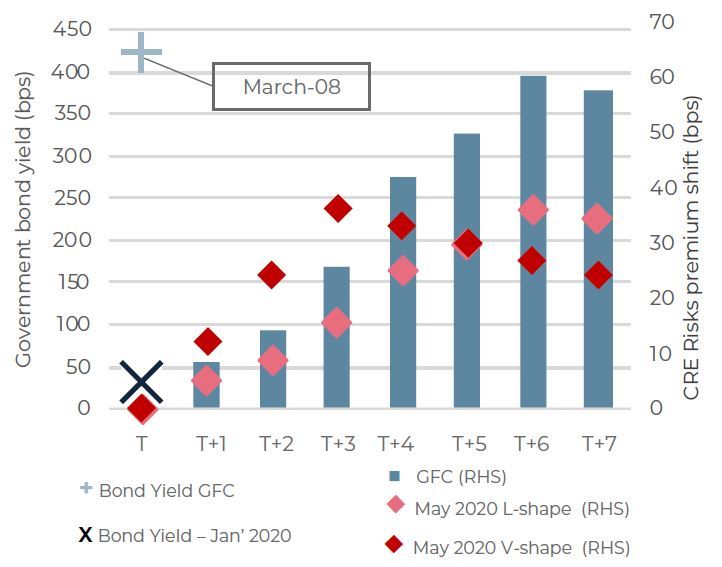

- Building on our previous GFC risk premia work to evaluate investor pricing, we estimate liquidity and volatility premia for two additional scenarios based on a May-20 L-shape and May-20 V-shape recovery.

- As highlighted in the graph, we show: i) the current government bond yield versus the one at the onset of the GFC, ii) the reference expected risk premia based on the GFC from our previous report, iii) the May-20 L-shape recovery risk premia based on a prolonged recovery and, iv) the May-20 V-shape recovery risk premia.

- The current 0.3% government bond yield environment is significantly lower from the 4.2% at the outbreak of the GFC. Therefore, we adjust for the relative difference in the yield widening by taking into account yield convexity. Less yield widening now has a similar value impact than right after the GFC.

- Based on this, we assume a 16bps yield widening for the L-shape in line with the GFC pace but a more rapid 36bps widening for the V-shape recovery by the end of 2020. For 2021, we expect a further yield widening for the L-shape scenario, but a tightening for the V-shape scenario.

Average risk premia scenarios

Sources: Oxford Economics, RCA, CBRE, AEW

LOGISTICS MOST RESILIENT FOR RISK PREMIA SHOCK

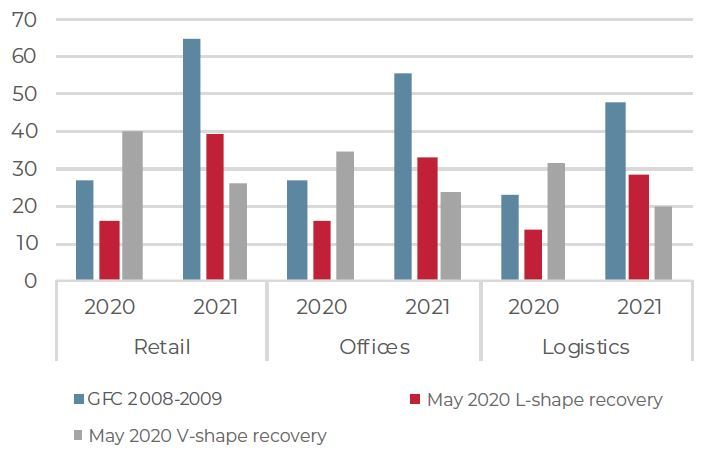

- Taking a closer look at the risk premia scenarios for the property sector level allows us to differentiate and estimate initial yields for each of the specific sectors in 2020 and 21.

- As shown in our chart, estimated risk premia for retail are higher than offices and logistics for all three scenarios. This reflects the impact of e-ecommerce, the lack of liquidity and relative high cash shortfalls in the sector. Therefore, initial yields are expected to move out further in retail compared to offices and logistics.

- Furthermore, we observe that the V-shape recovery implies a higher risk-premia in 2020 than the L-shape recovery, but a reversal of risk premia in 2021. This means that the cumulative yield impact by the end of 2021 is lower for the V-shape recovery than the L-shape recovery.

- Finally, the impact of yield convexity, i.e., controlling for the relative level of the yield, is clearly visible as the risk-premia for the L-shape and V-shape is lower than the GFC scenario.

Property sector risk premia

Sources: RCA, CBRE, AEW

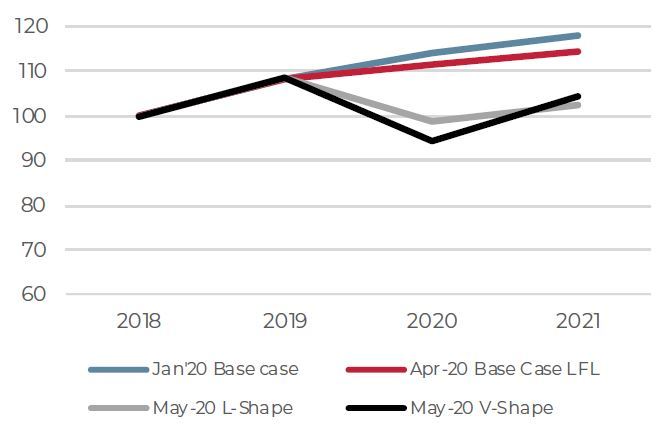

NEW SCENARIOS SHOW 4-6% DOWNSIDE IN PRIME OFFICE CAPITAL VALUES FOR 2020-21

- By combining the rental defaults, risk premia scenarios and the forecasted declines in market rents (COVID-19 flash report two) due to the COVID-19 induced recession and 2021 recovery, we can estimate Capital value changes in the short-term.

- The graph includes our previously reported Jan’20 base case and Apr’20 LFL base case together with our two new scenarios (May-20 L-Shape and May-20 V-Shape) which are explained above.

- In the case of offices, we are seeing in our L-shape scenario a cumulative value impact of -6% over the two years, consisting of - 9% move in 2020 offset by a 4% recovery in 2021.

- On the other hand, our V-shape scenario shows a cumulative value impact of only -4% over the two years, consisting of a more dramatic -13% move in 2020 offset by a robust 11% recovery in 2021.

Prime office capital values under various scenarios (indexed at 2018 = 100)

Sources: CBRE, AEW

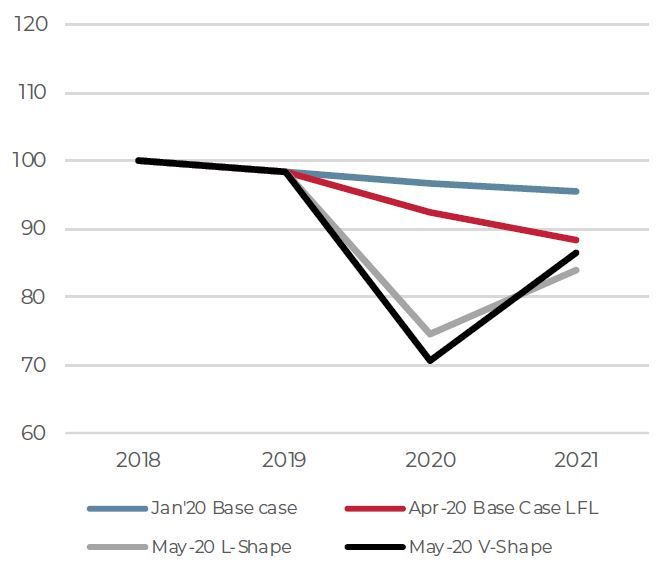

12-15% DOWNSIDE FOR 2020-21 IN EUROPEAN PRIME RETAIL CAPITAL VALUES

- Retail market rents are projected to have the biggest decline amid increased pressure from e-commerce and a relatively high sensitivity to the COVID-19 pandemic.

- Based on the most recent market evidence, retail landlords are suffering the biggest loss of received cash rents relative to offices and logistics. We assume that this will affect 2020 income only, as lower market rents and early renewals should limit continued weakness in 2021.

- Prime retail does benefit from lower increases in initial yields in 2020-21 compared to the GFC, due to lower absolute level of government bond yields.

- In balance, we expect in our L-shape scenario a cumulative value impact for prime retail of -15% over the two years, consisting of -24% move in 2020 offset by a 12% recovery in 2021. Our V-shape scenario shows a cumulative value impact for prime retail of -12% over the two years, consisting of a more dramatic -28% move in 2020 offset by a very strong 22% recovery in 2021.

Prime retail capital values under various scenarios (indexed at 2018 = 100)

Sources: CBRE, AEW

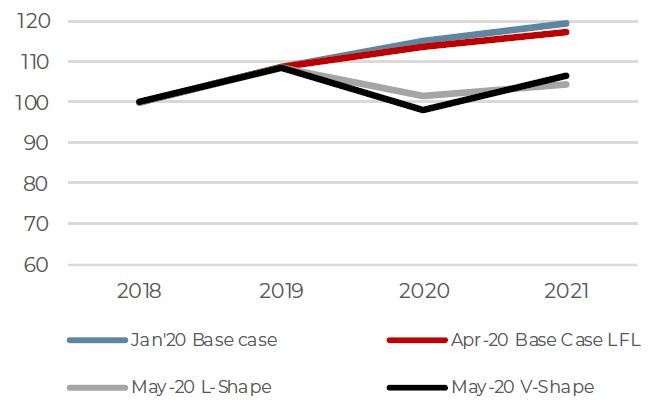

ONLY 2-4% DOWNSIDE FOR EUROPEAN PRIME LOGISTICS CAPITAL VALUES IN 2020-21

- As retail rents suffer from increased e-commerce penetration, logistics rents continue to benefit. Combined with a lower sensitivity to GDP growth and the COVID-19 pandemic, logistics rents are forecasted to have the smallest declines in market rents.

- In addition, logistics landlords are suffering only modest losses of received cash rents relative to retail.

- Like the other property types, logistics benefits from lower increases in initial yields in 2020-21 compared to the GFC.

- Based on these factors, we project that in our L-shape scenario a cumulative 2020-21 value impact for prime logistics of -4% the two years, consisting of -6% move in 2020 offset by a 2% recovery in 2021.

- Our V-shape scenario shows a cumulative value impact for prime logistics of -2% over the two years, consisting of a -10% move in 2020 offset by a 9% recovery in 2021.

Prime logistics capital values under various scenarios (indexed at 2018 = 100)

Sources: CBRE, AEW

READ THE FULL REPORT

The information and opinions presented in this research piece have been prepared internally and/or obtained from sources which AEW believes to be reliable; however, AEW does not guarantee the accuracy, adequacy, or completeness of such information.