This report was produced in collaboration with the Real Estate Research Centre at Cass Business School.

COVID-19 PUSHES REFINANCING ISSUES TO NEAR HALF GFC LEVELS

- COVID-19 related capital value declines combined with more conservative lending will lead to refinancing problems in the coming years, despite moderate pre COVID-19 loan-to-value (LTV) levels compared to the global financial crisis (GFC).

- Our debt funding gap (DFG) methodology measures the mismatch between the outstanding principal debt amount with what is available for refinancing across both the UK and German commercial real estate markets.

- The UK DFG is estimated at £30bn for the 2020-23 period, or 16% of outstanding loans. It is less than half the £70bn (or 30%) estimated during the 2008-11 aftermath of the GFC.

- With nearly 50% of the UK DFG accounted for by retail-backed loans, it is clear that other sectors are more resilient.

- In absolute terms, the €54bn German DFG is bigger than the UK’s. But, given the larger size of the German market, the DFG percentage of current outstanding loans stands at only 10.5%. Insufficient data limits further country comparisons for now.

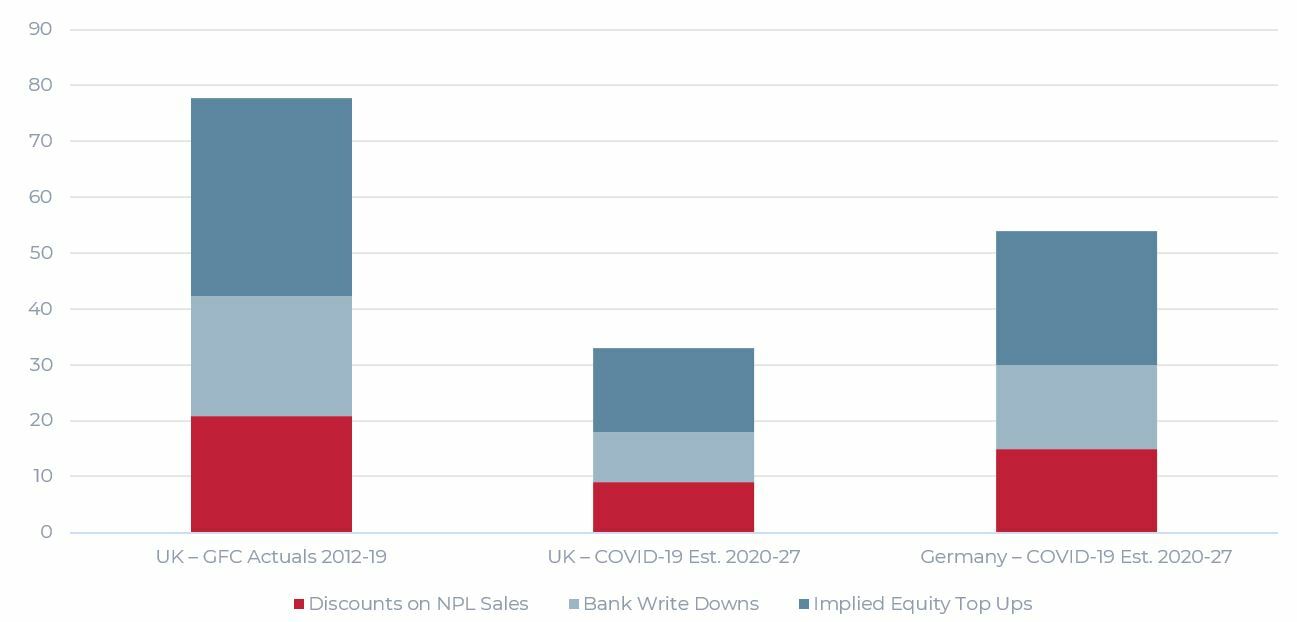

- In the 8 years following the GFC, the UK DFG was bridged by a combination of bank losses from discounted sales of non-performing loan portfolios (NPL) and loan write-downs as well as implied equity top ups from investors.

- If we assume a similar negotiated approach with lenders and investors bridging the upcoming COVID-19 DFG, €39bn will be needed from investors in the UK and Germany over the next 8 years (2020-27) to protect their debt-funded investments.

- German and UK banks have the highest capital ratios in Europe and are better positioned to take losses, which might benefit debt-funded commercial real estate investors this time around.

- Finally, initial estimates show that overall NPL ratios for German banks are not exceeding previous maximum levels, like in many Southern European countries, possibly benefitting investors’ positions.

ACTUAL AND ESTIMATED BRIDGING OF THE DEBT FUNDING GAP (UK AND GERMANY) IN € BN

Sources: AEW, Cass, IPF and IREBS.

PRE COVID-19 LTV MODERATE COMPARED TO PRE GFC

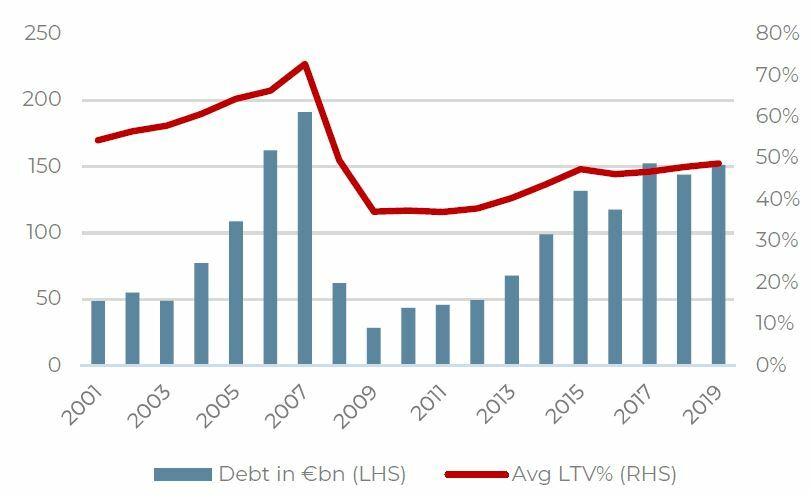

- Estimated 2019 acquisition loan-to-value ratios (LTVs) of 50% across the European markets are modest when compared with the +70% pre-GFC levels.

- Investment transactions year-to-date are down by about 20% driving down new lending volumes.

- More importantly, lenders’ LTVs have been adjusted downward during the immediate aftermath of the COVID-19 crisis and it is reasonable to expect the 2020 full year LTV to come out below 50%.

- This offers a good starting point for the overall European markets to withstand the anticipated impact of any declines in capital values and further adjustment in lender terms, as the COVID-19 induced economic recession and anticipated recovery unfold.

Estimated European acquisition debt and market-wide LTV

Sources: AEW, CBRE & RCA

COVID-19 IMPACTS RETAIL CAPITAL VALUES MOST

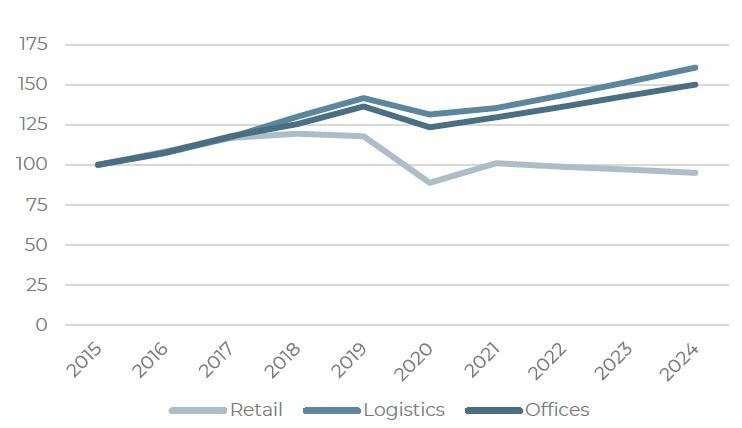

- As highlighted in our recent COVID-19 market updates, capital values are expected to decline as a result of the COVID-19 related lockdowns due to their impact on GDP growth, tenants’ ability to pay rent and increased liquidity and volatility risk premiums.

- Based on our forecasts, the impact on retail values is going to be more severe than in offices and logistics. This is mostly due to a significant one-off step-up in e-commerce penetration during the lockdowns, its long term impact on retail tenants and investors’ return requirements.

- We have indexed capital values in 2015 based on the assumption that most mortgage loans have a five year maturity. This means that the LTV for a 2015 vintage loan that needs to be refinanced in 2020 is based on the original 2015 value.

Actual and forecasted European prime capital values per sector (indexed 2015 = 100)

Sources: AEW & CBRE

DEBT FUNDING GAP QUANTIFIES REFINANCING RISK

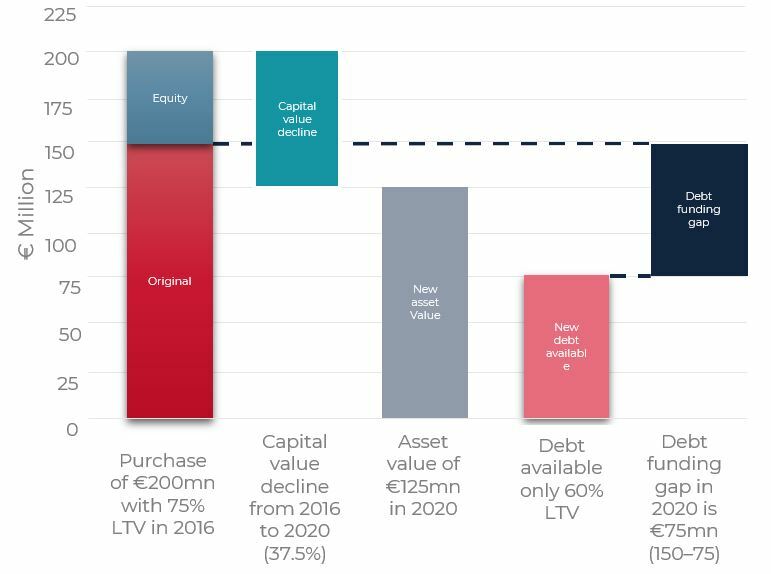

- To quantify the impact on the real estate market of excess leverage and capital value declines we estimate the DFG, as illustrated in the chart by the following steps:

- The original acquisition of a sample property at €200mn in 2016 with a loan at 75% LTV.

- COVID-19 related downside adjustment of the retail asset’s value of 37.5% over the next four years.

- Refinancing of the new asset value at the bank’s lower LTV of 60%.

- DFG is €75mn - difference between €150mn original debt and new refinancing of €75mn.

- Investors and lenders need to bridge this re-financing gap to rebalance their positions. In this respect, the lender can take write-downs or sell their loan position at a discount. Also, the investor can top up their equity to protect their initial investment against lender enforcement. We will come back to this bridging later.

- First, we estimate the extent of the problem, the debt funding gap in the UK.

Step-by-step estimation of the Debt Funding Gap for an exaggerated example UK retail-backed loan

Sources: AEW

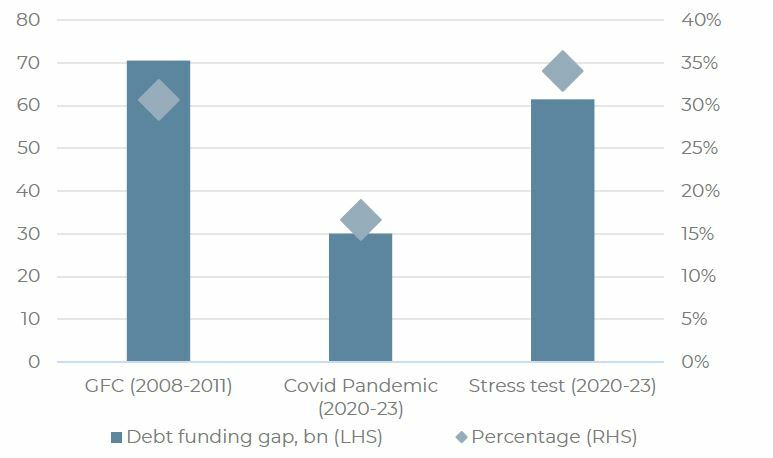

UK COVID-19 INDUCED DEBT FUNDING GAP ESTIMATED TO BE LESS THAN HALF OF GFC

- We estimate the UK commercial real estate DFG to be around £30bn, or 16% of outstanding loans for the 2020-2023 period. This is much lower than the £70bn, or 30% of outstanding loans, witnessed during the aftermath of the Global Financial crisis.

- The reason for the lower DFG in 2020-2023 is mainly because of stricter bank regulations in the aftermath and more conservative acquisition LTVs. In addition, we also expect capital value declines to be less severe compared to the GFC.

- In our stress-test scenario, we assume a similar value decline as in the GFC across all sectors. This results in a much higher funding gap of over £60bn or around 35% of outstanding loans for the 2020-2023 period compared to the base case. Also, as a percentage of outstanding loans the UK DFG would be even be higher than the one observed in the aftermath of the GFC.

UK Debt Funding Gap in £ bn and as % of outstanding loans

Sources: Cass Business School, CBRE & AEW

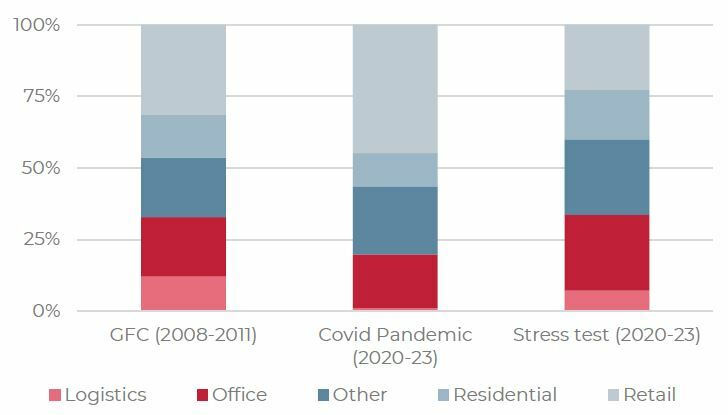

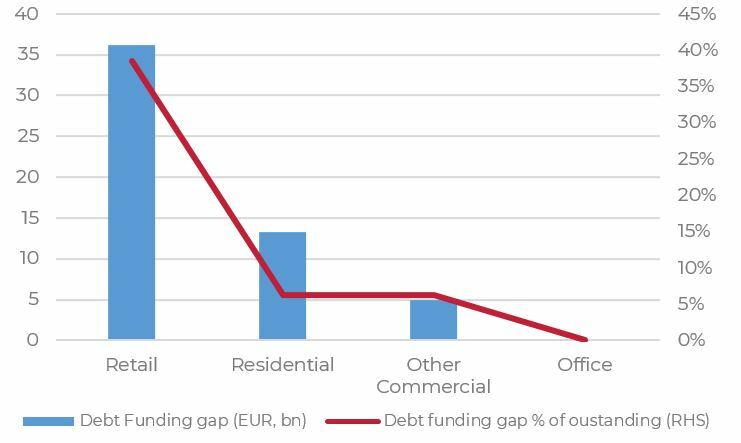

RETAIL SECTOR EXPECTED TO BE THE LARGEST SHARE OF DEBT FUNDING GAP

- The COVID-19 pandemic induced DFG in the UK is predominantly sector specific with retail estimated to be around 45% of the total DFG. Therefore, sectors such as logistics and residential are expected to be much more resilient and only contribute a small portion of the DFG.

- This highlights the differences of the COVID-19 DFG with the one in the aftermath of the GFC, which was more systematic with all sectors being influenced by the decline in values and decrease in debt availability.

- Finally, the stress-test shows the broader fall in capital values as the share of the different sectors to the DFG would be more equal with the exception of the logistics sector.

UK Debt Funding Gap per sector as % of total

Sources: Cass Business School, CBRE & AEW

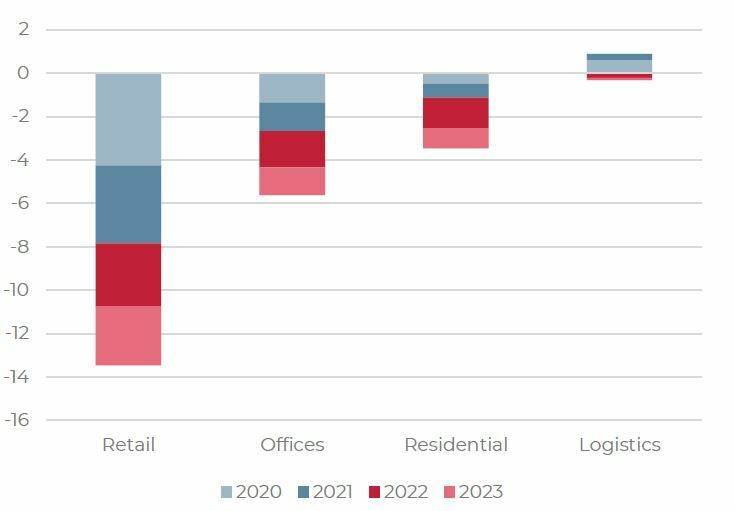

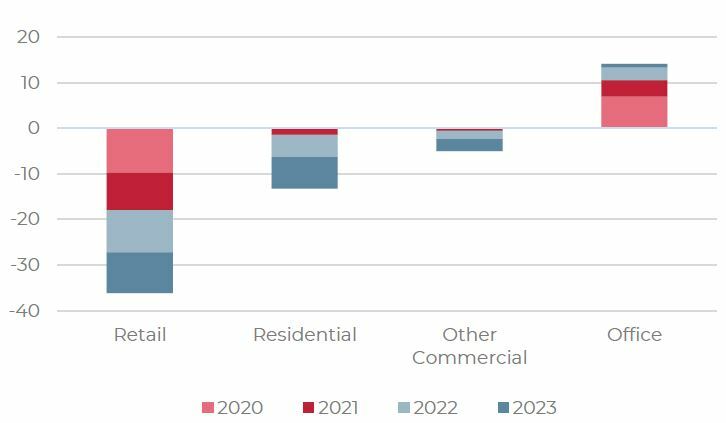

DEBT FUNDING GAP EXPECTED TO BE LARGEST IN 2022

- The DFG varies over the next four years (2020-2023) and is expected to be the largest in 2022 (£6.2bn) followed by 2020 (£6.1bn). This is interesting and highlights the strong capital value growth that we have witnessed over the 2015-2018 period.

- The residential sector confirms the latter as we expect the DFG to be the largest in 2022 and 2023 as capital values have increased over the 2016 & 2017 period. The increase in capital values offsets the initial fall in capital values in 2020 and therefore would have a greater effect on loans originated more recently.

- Lastly, we observe that the logistics sector is most resilient as capital values are expected to be less impacted driven by e-commerce trends. Also, capital value increases in the 2016-2019 period were significant and are a cushion to the DFG in the logistics sector.

- Please note that we have excluded the “other” property sector from this graph.

COVID-19 UK Debt Funding Gap by year and sector in £bn

Source: Cass Business School, CBRE & AEW

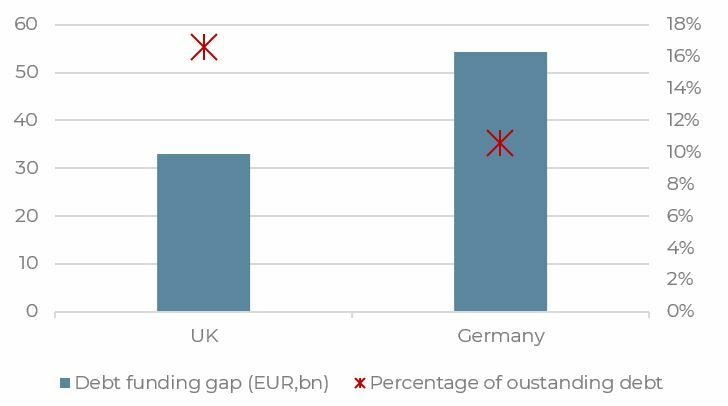

GERMANY EXPECTED TO BE MORE RESILIENT

- We estimate the German DFG to be around 10.5% of total outstanding loans, well below the UK’s 16.6%.

- Due to limited historical data availability, a comparison between the GFC and the current COVID-19 environment is not possible for Germany.

- In absolute terms, the German DFG at €54bn is larger than the €33bn DFG in the UK.

- But, the German lending market is much bigger than the UK with €515bn in outstanding commercial real estate loans, resulting in a lower percentage.

- The difference between the UK and German DFGs can also be partially explained by the fact that the German market is expected to be more COVID-19 resilient resulting in lower capital value declines than in the UK.

- Please note that insufficient data for other countries limits our ability to expand our comparison beyond the UK and Germany.

Debt Funding Gap in €bn & % of loans outstanding

Sources: IREBS, Cass Business School, CBRE & AEW

MAJORITY OF GERMAN DEBT FUNDING GAP IN RETAIL

- The DFG in Germany is largely concentrated in the retail sector at €36bn, approximately 66% of the total. Unfortunately, we have no logistics specific loan data for the German market.

- On the upside, the German office sector is an outlier amid strong performance in terms of recent capital value growth underpinned by low vacancy rates and a muted supply pipeline.

- These favourable occupancy fundamentals cushion the potential decline in future capital values and result in our estimate of no DFG for the German office market.

- In addition, the situation for the residential market is relatively stable as only 6% of the sector is estimated to face a possible DFG issue over the 2020-2023 period.

German Debt Funding Gap in €bn & % of loans outstanding

Sources: IREBS, CBRE & AEW

GERMAN DEBT FUNDING GAP BACK LOADED

- The majority of the DFG is back loaded, indicating that more recently originated deals may face more issues compared to loans originated in the 2016-2017 period. This underpins the strong growth most sectors have experienced in the 2016-2019 period.

- Therefore, we expect the largest contribution to the DFG to be in 2023 at €18bn, followed by 2022 with approximately €16bn which together account for over 60% of the total estimated German DFG.

- Finally, we observe that the impact on retail is somewhat equally distributed over the four years amplifying the secular trend the sector is undergoing.

German Debt Funding Gap by Sector in €bn

Sources: IREBS, CBRE & AEW

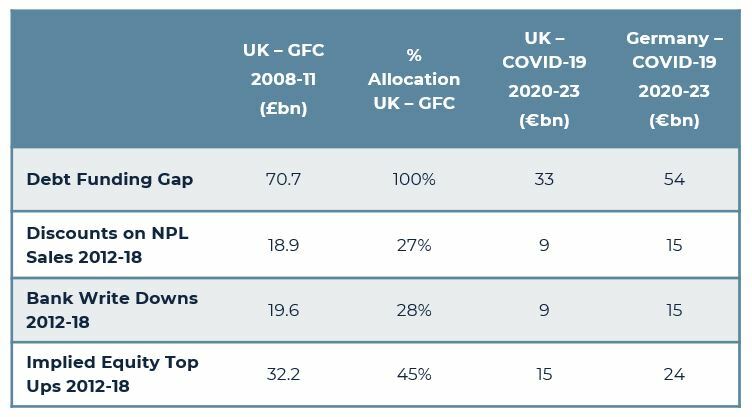

DEBT FUNDING GAP BRIDGED BY BANK LOSSES AND EQUITY TOP-UPS

- As illustrated in the table, historical data shows that the £71bn GFC DFG in the UK was bridged for 55% by discounts on NPL loan sales and bank write downs with the remaining 45% coming from equity top ups.

- If we use the same UK GFC percentage allocation for our COVID-19 related 2020-23 DFG, we estimate that equity investors need to top up by €39bn in Germany and the UK combined in the next 4-8 years.

- This will require some tough discussions between investors and lenders, but given the relative, modest system-wide LTVs it seems reasonable that many equity investors will top up to protect their principal investment.

Estimated Debt Funding Gaps and Bridging Channels

Sources: AEW, CBRE, Evercore & IPF

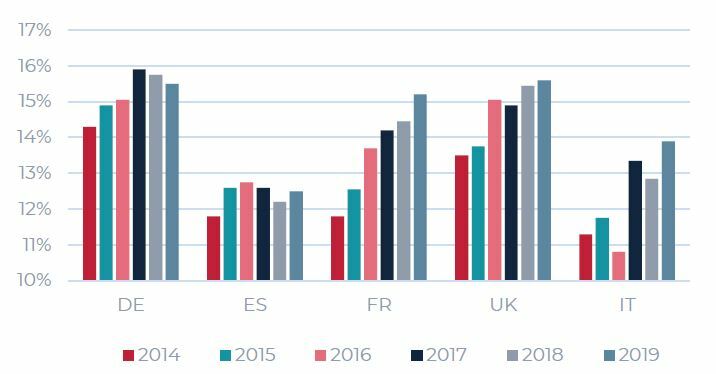

UK, GERMAN AND FRENCH UK BANKS ARE BETTER POSITIONED TO TAKE LOSSES

- Despite the significant improvement in tier 1 capital ratios for French and Italian banks, it is clear from the data that UK, German and French banks are better positioned to absorb losses than their other European counterparts.

- Clearly each individual bank’s capital reserves and profitability will impact on the extent and speed in which they are able to take write downs or might be forced to sell NPL portfolios at smaller or larger discounts.

- Given the higher overall ratios compared to the GFC, it seems reasonable to expect a more pro-active and quicker resolution of non-performing real estate loans in the post COVID-19 era.

Banks’ tier 1 capital ratio evolution, selected countries

Sources: AEW & ECB

REAL ESTATE PART OF NEW COVID-19 WAVE OF NPL’S

- The average European NPL ratio as a share of the loan book fell to a record low 3% in 2019, as NPLs were managed down from over €1.15tn in 2015 to €636bn.

- Similar as with real estate collateral, COVID-19 is expected to impact the credit quality of bank loans across most industries and borrowers and reverse much of the pro-active loan work-outs at banks.

- Advisors NPL Markets estimate that NPL ratios will exceed their historical maximums in Italy, Spain, France and the Netherlands. The UK and Germany show increases as well, but are fortunately not expected to break new records.

- As a result of these COVID-19 related increase in NPL ratios, it is likely that banks will re-start the cycle of increasing reserves, taking write downs, selling NPL loan portfolios and re-structuring existing loans. Our DFG analyses confirms this trend.

European NPL ratios to increase post COVID-19

Sources: AEW & NPL Markets

READ THE FULL REPORT

WATCH THE WEBCAST

The information and opinions presented in this research piece have been prepared internally and/or obtained from sources which AEW believes to be reliable; however, AEW does not guarantee the accuracy, adequacy, or completeness of such information.