IS CRE DEBT PRICED EFFICIENTLY ENOUGH FOR INVESTORS?

Analysis on the cost of debt for real estate investors across Europe has been historically limited by the lack of available granular loan level data. There have been a number of lender surveys, including the UK Cass Business School (formerly DeMontfort University) survey started in 1999 that allows for some useful trend analyses. Additional surveys have been launched for Germany (IREBS) and further expansions for similar lending surveys are expected for France (IEIF) and Spain (Cass & Universidad de Alicante). Some leading brokers share city and property type level data on prime lending costs, but the underlying granular loan level data has been available only to central banks and regulators (via the ECB’s AnaCredit Data initiative) as they have shifted from their initial stress testing of existing troubled bank loan books a few years ago to monitoring the current lending and refinancing activity. In this report, we share our initial analyses of loan-level data from both internal AEW and external sources. Despite sometimes significant differences between individual loans and credits, we focus on pricing and risk trends on a detailed loan-by-loan level. This should allow us to answer the question: is commercial real estate debt priced efficiently for investors in European markets?

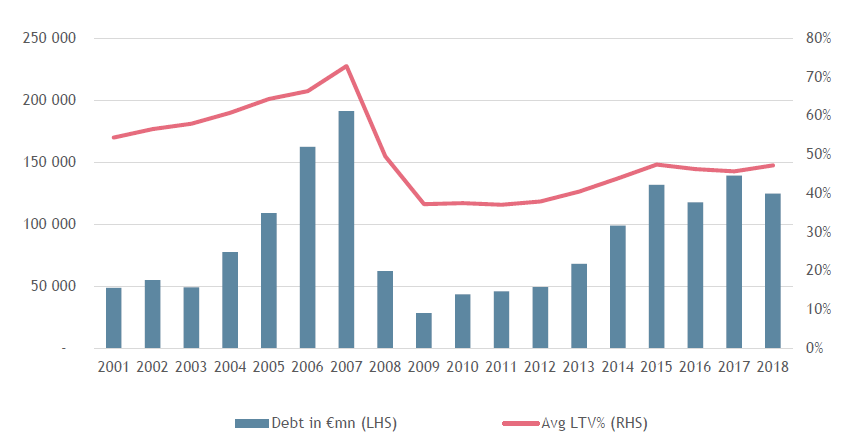

ANNUAL LOAN ORIGINATION FOR ACQUISITIONS WITH SYSTEM-WIDE LTV

Source: AEW, CBRE & RCA

EXECUTIVE SUMMARY

- In this report, we evaluate all-in interest rates and loan margins for commercial real estate (CRE) investors in the European markets by using for the first time granular loan-level data and estimating historical CRE loan loss rates.

- Our granular loan-level database shows a number of interesting trends:

- Loan margins remain elevated at about 200bps, despite coming down from 260bps peak in 2013

- The average all-in interest rate for European CRE loans is at a historically low level of 2.1% pa as of 2Q19

- This is only possible, since the 5-year swap rate is at unprecedented near-zero historic lows, in line with bond yields

- German all-in rates have been consistently low, due to strong lender competition and efficient covered bond funding

- Retail loans have become more and logistics loans less expensive, as lenders adjust pricing for changing fundamentals

- Despite record low borrowing costs, restraint and discipline by investment fund managers and institutions helped by regulatory-constrained banks limits the system-wide risk of excessive financial leverage.

- Our CRE loan-level model shows strong results in predicting the all-in interest rate by using LTV, origination year, property type and collateral locations as explanatory variables.

- At current CRE loan pricing, lenders are able to absorb potential losses through their loan margins and other fees as long as they are in line with historical averages. Our top-down estimate for historical CRE loan losses are 70bps pa for European banks and 93bps pa for UK banks. Both are ahead of CMBS-funded CRE loan losses of 21 bps pa for Europe and 24bps pa for UK.

READ THE FULL REPORT

The information and opinions presented in this research piece have been prepared internally and/or obtained from sources which AEW believes to be reliable; however, AEW does not guarantee the accuracy, adequacy, or completeness of such information.