LONG TERM TRENDS ALLEVIATE CONCERNS ON RUNAWAY INFLATION

- As the post-Covid recovery takes hold, inflation has increased rapidly to 5% in the US and over 2% in Europe triggering concerns on future interest rates, as central banks could be forced to reverse their lower-for-longer policies to meet their restated long-term inflation targets.

- Apart from quantitative easing, one of the key drivers of low inflation has been the reduced velocity of money circulating in the economy. Most concerns around inflation are centered around velocity returning to more normal and higher levels, which would support the argument for a period of above target inflation.

- On the other hand, some broader macro and demographic trends have had a dampening effect on inflation. First of all, the increasing need for seniors to save more for retirement, especially as life expectancy and medical and long term care costs have been increasing.

- Secondly, there has been a clear downward trend in Europe’s inflation as a result of globalisation, as imports from overseas allow for lower costs. Despite the recent Covid reversal, we assume that globalisation will return to its long term trend, limiting any danger of runaway inflation in the medium term.

- The third reason to expect inflation to be transitionary is the Covid-19 triggered negative output gap. This gap represents the unutilised spare capacity in the economy providing a buffer against inflation as the post-Covid recovery proceeds and continued monetary easing is absorbed first by the available spare capacity.

- From an analytical perspective, there is a positive relationship between inflation and government bond yields over the 1981-2021 period. However, this is much less the case in the last 10 years and in particular as recent bond yields have remained stable as inflation has picked up considerably. Current bond market pricing implies that inflation will be transitionary.

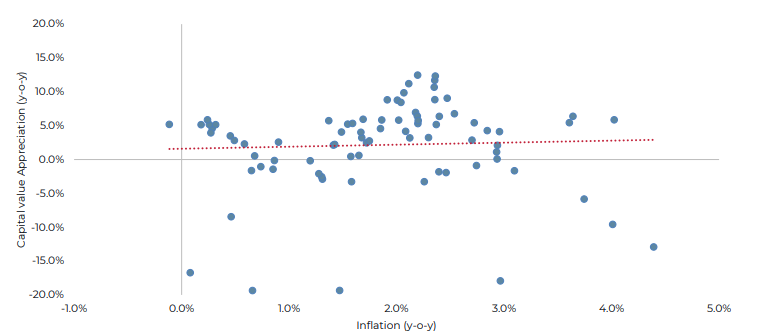

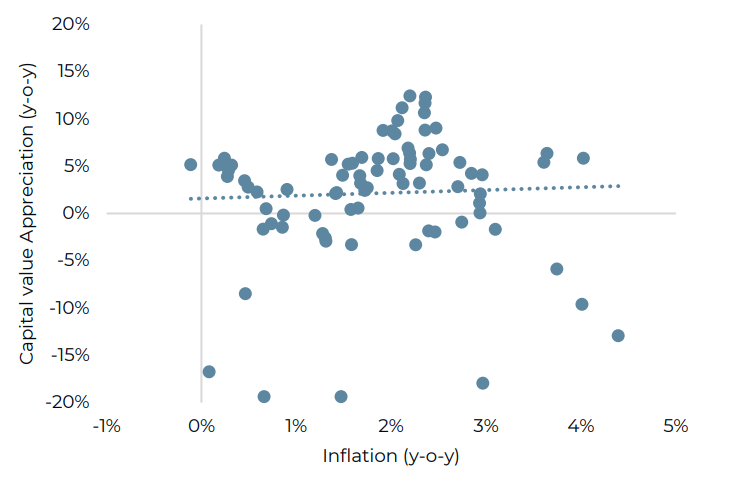

- To explore the impact on real estate returns, we note that inflation and capital value appreciation have been mostly uncorrelated since 2001. Therefore, in respect of capital appreciation, real estate is not a good inflation hedge. However, income returns as far as they are tied to index-linked rents will of course benefit from higher inflation.

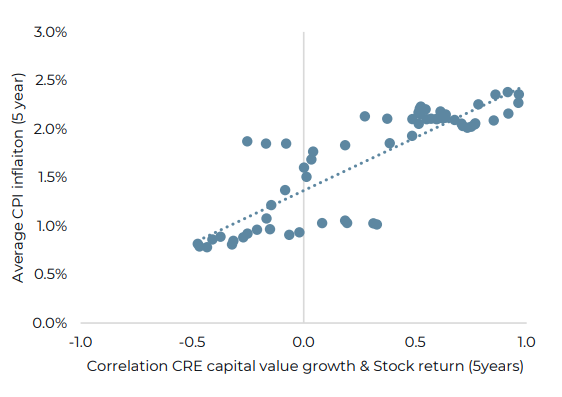

- Finally, it should be noted that stock and real estate returns are highly correlated in periods of elevated inflation which means that returns move in the same direction in times of higher economic growth and inflation. On the other hand, in periods of low inflation real estate returns are negatively correlated. This means that in low inflation environments, equity investors can realise diversification benefits from investing in real estate.

All property capital appreciation and inflation (2001-2021)

Sources: Oxford Economics, INREV & AEW Research & Strategy

INFLATION COMES INTO FOCUS

INFLATION UPTICK TRIGGERED CONCERNS ON LOW RATES

- Despite increasing vaccinations, the pandemic has entered its next phase. Since hospitalisation seems to be at reduced levels compared to previous phases, governments are starting to lift more restrictions.

- As a result of these, the economic recovery has started with Chinese and US growth leading the way. However, even in Europe employment and retail sales are rebounding strongly, albeit from a low 2020 base.

- Due to some remaining and lingering Covid-related disruptions in global supply chains and some shortages in raw materials and key components, inflation is now above 2% - the ECB’s pre-Covid target.

- This is still moderate when compared to US levels, which stand closer to 5%. Regardless of the level, many investors started questioning the consensus outlook for lower-for-longer interest rates.

- The ECB followed the FED by re-stating its inflation target to a longer horizon, reducing market concerns of a rate hike in the short term.

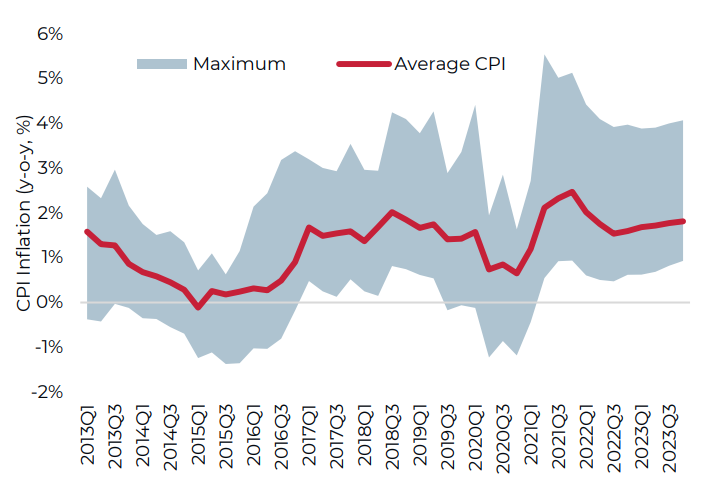

- Oxford Economics forecasts show that inflation is coming back below 2% in early 2022, but some countries’ CPI is projected to stay elevated.

Average Consumer Price Index (CPI) with Min-Max range for 19 European countries for 2013-2023

Sources: Oxford Economics, AEW Research & Strategy

CURRENT LEVELS STILL WELL BELOW HISTORICAL PEAKS

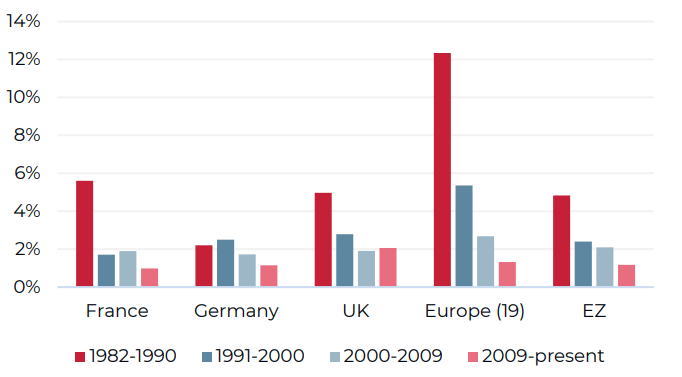

- With inflation projected to peak just below 2.5% by the end of 2021, it remains well below the historical peaks across the region.

- Given its history of hyperinflation, it is noticeable that German inflation was low in the pre-Euro eras of 1982-90 as well as well as 1991-00. France’s CPI started coming down in the run up to the 1999 introduction of the Euro as well.

- The 12% inflation across the 19 European countries in the 1982-90 period is more a reflection of the then communist CEE countries inability to control prices.

- For all key countries and aggregates the most recent 12-year period stands out as the lowest annual CPI since 1982, with the notable exception of the UK.

Average Consumer Price Index (CPI) for select European countries for various historical periods

Sources: Oxford Economics, AEW Research & Strategy

REASONS TO EXPECT HIGHER INFLATION

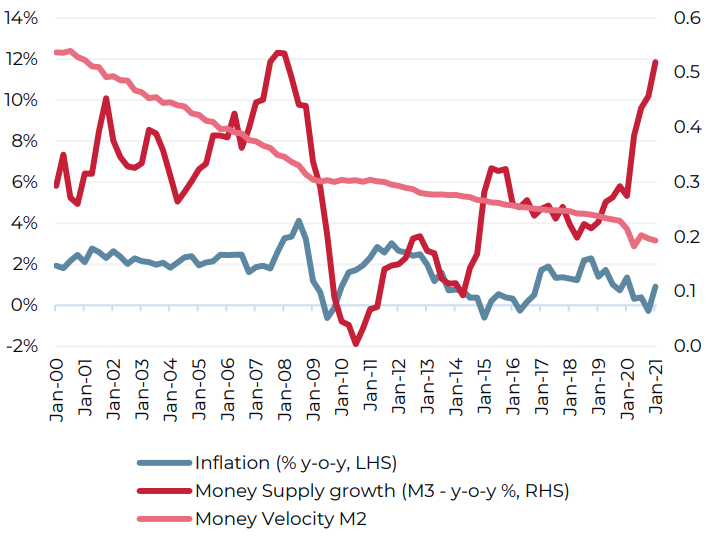

- Irving Fisher’s classical quantity theory of money states that the actual total value of all money expenditures (MV) always equals the actual total value of all items sold (PT).

- MV itself is the money supply (M) available to be spend times the speed at which it is actually spent, or velocity (V). While PT is the price level times the amount of goods & services produced.

- Post GFC and more recently in response to the Covid-19 shock, central banks have increased the money supply, in part by buying up bonds in the open market.

- This means that money supply has been increasing, while at the same time the velocity has been reducing over the last 20 years.

- The reduced velocity of money circulating in the economy is one of the reasons that inflation has been modest despite historically significant increases in money supply.

- If velocity returns to more normal and higher levels, that would a strong argument in favour of increased inflation.

- The long term validity of the Fisher equation could be in question given some demographic changes in advanced economies.

Eurozone inflation, money supply and money velocity 2000-21

Sources: Oxford Economics, AEW Research & Strategy

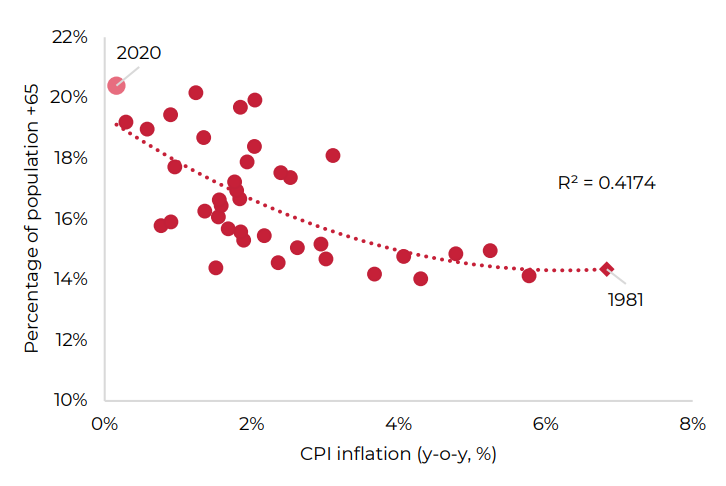

AGEING POPULATION DRIVES INFLATION DOWN

- Despite the pandemic’s short term disruption of earnings, consumption and savings, long term demographic trends will also drive the inflation outlook.

- Over the last 40 years, the increasing share of seniors has had a dampening effect on inflation, as indicated by the chart. This is expected to remain as the share of seniors further increases in future.

- It can be explained by the increasing need for seniors and soon-to-be seniors to save more for retirement, especially as life expectancy and medical and long term care costs have been increasing.

- Their savings needs are further boosted by the growing lack of government funding for pensions and care as well as the low yields on fixed income investments in many private pension pots.

- As seniors are forced to save more, they are also spending less. Since they make up an increasing share of the population this will limit GDP growth from consumption and lower the velocity of money.

- Low and falling overall population growth will further amplify this dampening effect on inflation, as already seen in Japan.

Correlations between age and Inflation – 65+ population vs CPI Inflation (Y-o-Y, %) in Germany, France and the UK for 1981-2020

Sources: Oxford Economics, AEW Research & Strategy

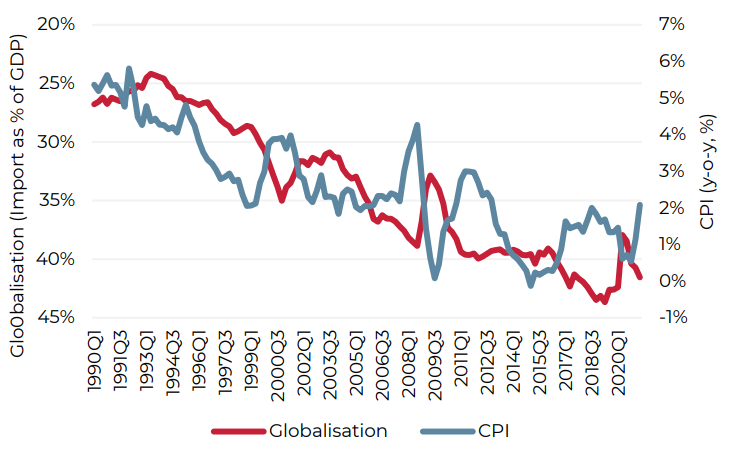

COVID REVERSAL ASIDE, GLOBALISATION LIMITS INFLATION

- Covid-19 restrictions reduced European imports (defined as globalisation) to below 38% of GDP in Q2 2020 – their lowest in 10 years. But, for Q2 2021 a rebound to near 42% is already projected.

- As the chart shows, in the last 30 years there has been a clear downward trend in Europe’s inflation as a result of globalisation, as overseas producers allow goods to be imported at ever lower costs.

- There have been other reversals in the long term trend of globalisation, like post GFC and Trump’s recent China-US trade war. Each time there was such a reversal in globalisation, there was an increase in inflation.

- Therefore, if we assume that globalisation will return to its long term trend, as more countries are vaccinated and restrictions are lifted, this should limit the danger of runaway inflation in the medium term.

- Short term problems with overcomplicated global supply chains and specific commodities or component shortages will be resolved and European consumers can again benefit from low cost imports.

- As a result, inflation concerns should be alleviated.

Globalisation and CPI Inflation (Y-o-Y, %) in Europe for 1990-2020

Sources: Oxford Economics, AEW Research & Strategy

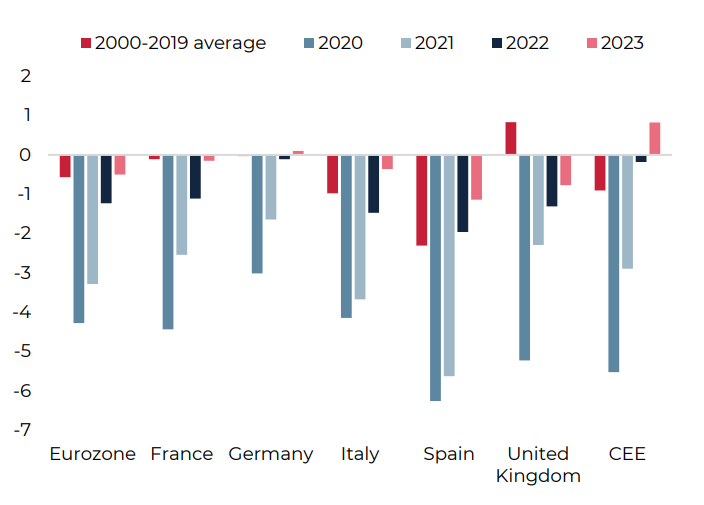

COVID-19 OUTPUT GAP TO CUSHION EUROZONE INFLATION

- Covid-19 has triggered an increase in the negative output gap across most European countries - well ahead of their historical averages.

- This negative output gap represents the unutilised spare capacity in the economy and comes from unemployed or underemployed workers that can be mobilised without increasing wage costs.

- As a result, it provides a buffer against inflation as the post-Covid recovery proceeds and continued monetary easing is absorbed first by the available spare capacity.

- The patterns across European countries is pretty logical, as the countries with the most severe Covid impacts in 2020 have seen the biggest increase in the output gaps.

- The UK and France are among the countries with the biggest increase in output gap. Spain and Italy also saw significant increases but had a bigger structural gap to begin with and were slower to reduce it.

- CEE stands out with a big impact in 2020, but quick recovery and positive output gap projected for 2023, a testament to its more dynamic economies.

Output Gap scenarios as % of GDP per country and region for 2000-2023

Sources: Oxford Economics, AEW Research & Strategy

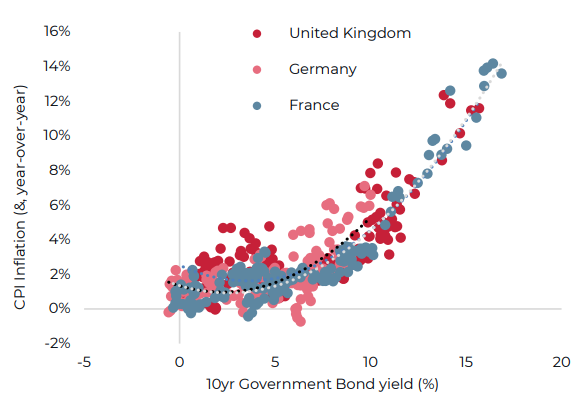

CURRENT INFLATION EXPECTED TO BE TRANSITIONARY

- In our Apr-21 mid-year outlook we included an upside scenario to highlight the implications of higher inflation for real estate returns. Higher inflation leads through higher bond and property yields to lower total returns compared to our base-case.

- A closer look at how government bond yields have responded to changes in inflation regimes is given by plotting the historical correlation from 1981 onwards for the UK, Germany and France.

- A positive relationship exists between inflation and government bond yields over the 1981-2021 period. The latter is highlighted by the fitted line (the dotted line for the three different countries) using the polynomial function instead of the linear function.

- However, if we look at the last 10 years and in particular at the current situation we observe that inflation has picked up considerably but that bond yields have remained low (similar to the US situation).

- Based on this, we expect that higher inflation will be transitionary and not structural.

Inflation and 10yr government bond yields (1981-2021)

Sources: Oxford Economics & AEW Research & Strategy

PAST CAPITAL APPRECIATION & INFLATION UNCORRELATED

- Given that we expect only a transitionary inflation spike, we investigate the historical relationship between capital value appreciation and inflation for the last 20 years across Europe.

- As the chart shows, inflation and capital value appreciation have been mostly uncorrelated, showing at a small positive (0.05). Please note that our sample only allows us to start in early 2000 and not in the late 70’s early 80’s when we had higher inflation regimes.

- Of course, it is important to note that during the GFC inflation was particular high and capital values fell substantially. If we disregard the GFC, we find a stronger relationship (correlation of 0.20) between capital appreciation and inflation.

- Based on our limited data, it is difficult to confirm that real estate, in respect of capital appreciation, is a good inflation hedge.

- However, income returns as far as they are tied to index-linked rents will of course benefit from higher inflation.

All property capital appreciation and inflation (2001-2021)

Sources: Oxford Economics, INREV & AEW Research & Strategy

HIGHER INFLATION INCREASES RETURN CORRELATIONS

- In the last step of our analysis, we explore the diversification between stock and real estate returns over different inflationary periods.

- To do this, we take the average stock-market performance for the five largest countries (UK, FR, DE, ES & IT) and correlate that to the INREV all fund returns on a five year holding period basis.

- The graph shows that stock and real estate returns are highly correlated in times of higher inflation which means that returns move in the same direction in times of higher economic growth and inflation.

- On the other hand, in periods of low inflation real estate returns are negatively correlated, implying that returns move in opposite directions.

- This means that in low inflation environments, equity investors can realise diversification benefits from investing in real estate.

- All in all, this means that if we stay in an era of modest inflation diversification benefits between stocks and real estate remain likely.

5 year inflation VS 5-year stock and CRE return correlations (2005-2021)

The information and opinions presented in this research piece have been prepared internally and/or obtained from sources which AEW believes to be reliable; however, AEW does not guarantee the accuracy, adequacy, or completeness of such information.