No Place Like Home: Defensive Residential Returns Attract Investors

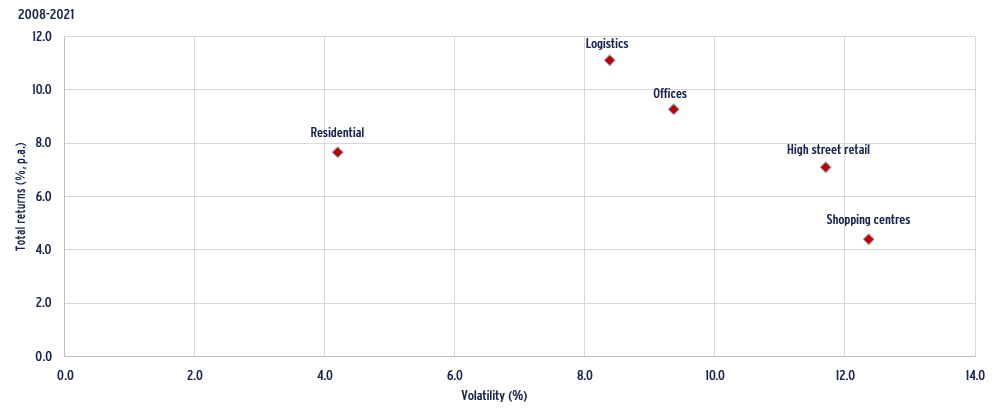

- Residential is the most resilient of all property types. Residential income streams are underpinned by a primary human need and come from a diversified individual tenant base, while supply constraints limit void periods. As a result, residential investments offer bond-like, stable and predictable cash flows. For these reasons, residential total returns have historically been less volatile than for the other property types, as highlighted by the scatter chart below, while at the same time generating prime total returns close to 8% pa. On a risk-adjusted basis, residential therefore stands out as the most attractive property sector.

- Continued lack of supply and strong demand from new household formations is driving prime rental growth in most European markets. Despite an increasing number of rental regulations to ensure affordability for tenants, prime residential rental growth is projected to be at 2.6% p.a. over the next five years on average in Europe.

- Environmental regulation is becoming more demanding every year in residential as in other property sectors. Homes with an Energy Performance Certificate (EPC) of G and F will not be allowed to be let in the near future. The transition risks are significant with steep reduction pathways expected to be met to respect the Paris accord to limit global warming to 2°C. Institutional investors are in the best position to green the residential stock by improving the energy efficiency of entire residential buildings and championing best in class developments.

- However, these rental and environmental regulations have not been deterring investors, who have committed more capital than ever in European residential in 2021. Volumes have been boosted by large portfolios sales and M&A, but also by new entrants and increasing allocation of investors already active in the sector. In less mature markets, institutional investors have to look for pre-funding opportunities with developers to build their portfolios.

- Our yield forecasts in our base case scenario are based on the outlook for swap-implied government bond yields. In this scenario, the risk premium over government bond yields is expected to remain high at 284 bps on average in 2022-2026 compared to 160 bps over the past 15 years. Over the next five years, prime total returns for the residential sector are forecast to reach 5.1% pa on average in the 24 markets covered, ranging from 3.4% p.a. in Munich to 8.1% p.a. in Manchester. A stronger inflation scenario would negatively impact residential total returns as the improved income returns would be offset by higher exit yields.

- In this research publication, we are sharing for the first time our internal forecasts on rental growth, yields and total returns in 24 different European residential markets, also known as the private-rented sector or multifamily*. In order to do our forecast modelling, we used Catella and Green Street historical data to compose our own synthetic data set on rent and yields for each of the 24 markets in our coverage universe.

PRIME EUROPEAN TOTAL RETURNS & VOLATILITY BY PROPERTY TYPE 2008-2021

Sources: Catella, Green Street, CBRE, AEW Research & Strategy

PANDEMIC HAS NOT LOWERED DEMAND IN CITIES BUT IS SLOWING SUPPLY GROWTH

DEMAND FOR HOUSING DRIVEN BY HOUSEHOLD MORE THAN POPULATION GROWTH

- Despite weak population growth in Europe, household growth remains strong in the main European metropolitan areas, driving demand for housing.

- Household growth is linked to by socio-demographic trends. Young people moving out of the parental home, divorces and an ageing population explain why the household average size has been reducing. Between 2010 and 2020, the number of single-person households increased by 20% in the EU.

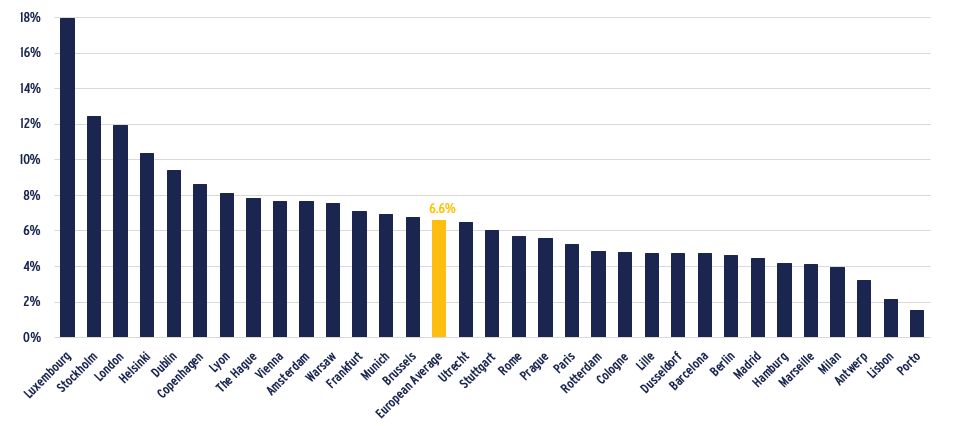

- Household growth differs across cities, with strong growth expected in Luxembourg, the Nordics & London and weaker but still positive growth forecast in Portuguese cities.

- In the short-term, the residential sector is benefiting from the post-Covid economic recovery. Furlough progammes have successfully supported income levels during the pandemic. Rental arrears have therefore been very limited despite temporary eviction bans introduced in most countries. This stronger than expected economic recovery and rising household incomes are also benefiting residential rents and prices.

- The Covid pandemic is not the death of the City. The suburbs of the largest cities and second-tier regional centres have benefited most from post-Covid internal migration.

Household growth forecasts 2021-2030 %

Sources: Oxford Economics, AEW Research & Strategy

NEW DEVELOPMENTS DELAYED BY LACK OF CONSTRUCTION MATERIALS & LABOUR SHORTAGES

- Housing completions remain insufficient to resorb the accumulated housing shortage over the years. This explains the high occupancy rates in the residential sector and limited void periods between tenants.

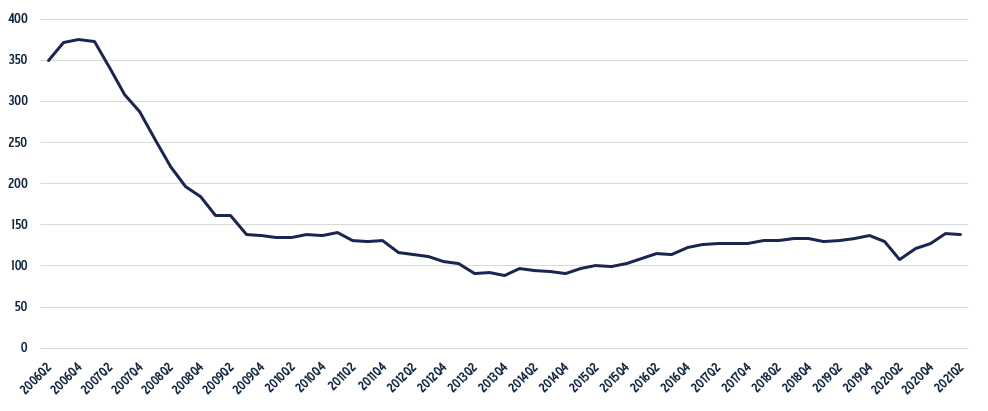

- As a result of the disruption from the lockdowns, the number of building permits filed dropped significantly in 2020. While the Covid impacts have been short-term, construction activity is expected to remain weak as the number of permits filed remains low in a historic context.

- Lack of buildable land, rising construction costs, more comprehensive environmental regulations and local planning policies are limiting residential developments. The current shortages and increased costs of labour and materials is also slowing down construction activity. As a result, demand will continue to outstrip supply.

- This lower construction activity has repercussions on the investment market as investors target new developments to build their residential portfolios.

EU building permits index (2015 = 100)

Sources: Eurostat, AEW Research & Strategy

OFFICE CONVERSIONS TO RESIDENTIAL IS DIFFICULT BUT THERE ARE SUCCESS STORIES

- Conversion of vacant office space to residential is often mentioned as a solution to housing shortages. Conversion remains however very difficult for financial, regulatory, fiscal and technical reasons.

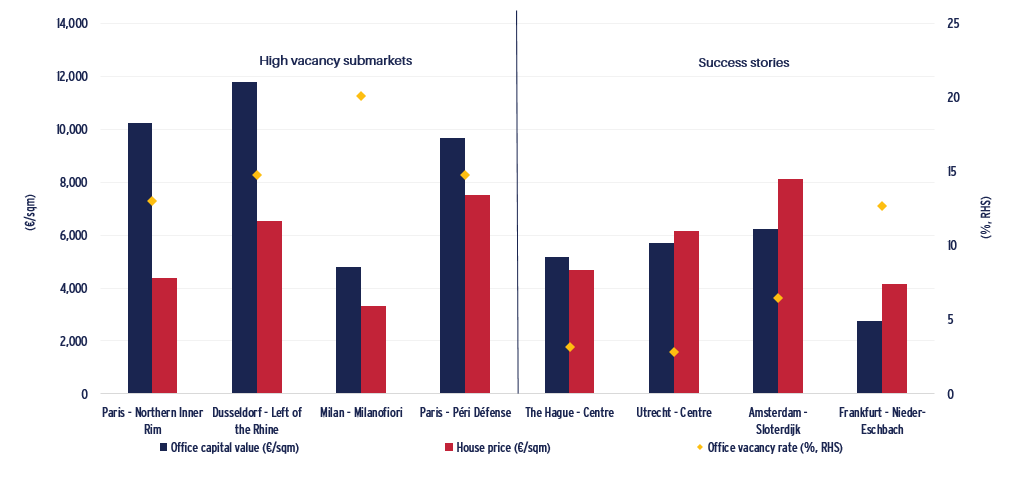

- Across Europe office vacancy rates are generally low, and much lower than post-GFC, limiting conversion opportunities. A comparison of office and residential capital values in the few office submarkets with double-digit vacancy rates highlights the challenges of repurposing obsolete offices, whose capital values remain higher than residential prices.

- Historically, conversions from office to residential has been very successful in the Netherlands and Frankfurt post-GFC when the vacancy rates were above 20%. Since the GFC, the office stock has shrunk by more than 20% in Amsterdam – Sloterdijk, in the centre of The Hague and in Frankfurt – Niedereschbach.

Office & residential capital values (€/sqm) & office vacancy rate (%, RHS)

Sources: CBRE, Immobilien scout, Meilleurs Agents, Huispedia, Idealista, AEW Research & Strategy

ROBUST RESIDENTIAL RENTAL GROWTH BUT INCOME STABILITY IS WHAT MATTERS

RENTS REFLECT RENT SETTING MECHANISMS

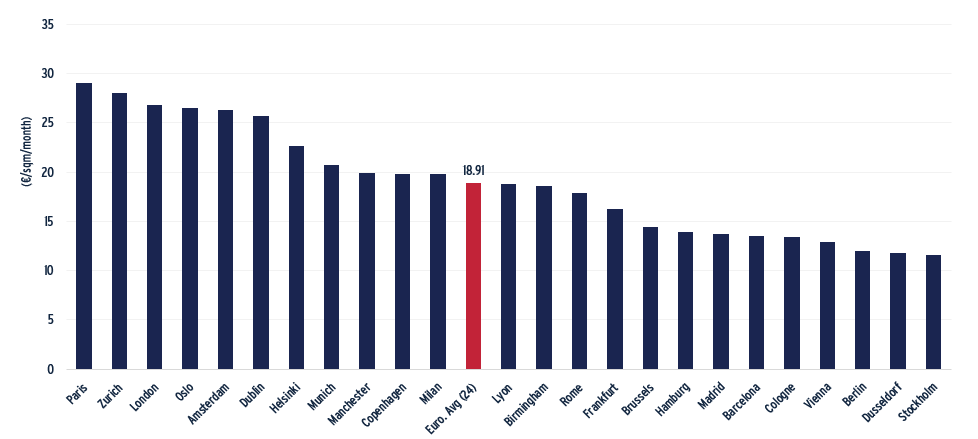

- Prime residential rents quoted in €/sqm/month are the highest in Paris, Zurich, London and Oslo, which reflects both higher disposable incomes and lack of supply.

- Regulation and market practices play a significant role. The rate at which rental levels can be increased during the term of a contract is regulated in most countries across Europe. Typical lease length of rental contracts varies: contracts are open-ended with no set duration of the lease in Denmark, Germany, Luxembourg, the Netherlands and Sweden.

- The surprising low residential rent recorded in Stockholm can be explained by the historic rent setting mechanism, based on collective bargaining between tenants’ associations and landlords.

- In Germany, residential rents are also relatively low as a result of the so-called Mietspiegel, which sets a benchmark rent that cannot be exceeded by more than 10% in areas where there is pressure on the housing market.

Prime residential rents (€/sqm/month) – Q3 2021

Sources: Catella, AEW Research & Strategy

PRIME RESIDENTIAL RENTAL GROWTH EXPECTED AT 2.6% P.A. ACROSS OUR 24 EUROPEAN MARKETS

- Looking at prime residential rents allows us to focus on new-built apartments which are exempt of rent control mechanism (with some exceptions). Please note that our forecasts do not take rental regulations into account, as it is not possible to know how regulation will evolve in the future.

- At 2.6% p.a. on average, prime residential rental growth expected between 2022 and 2026 is expected to be stronger than inflation (1.8% p.a.). This compares against 3.5% p.a. on average over the past five years.

- The regional cities Manchester, Lyon and Birmingham are expecting to outperform, as rents are typically lower than in capital cities.

- In contrast, Southern European cities are forecast to underperform the European average as a result of weaker demographic growth.

Prime residential rental growth (%, p.a.) - 2022-2026

Sources: Catella, AEW Research & Strategy

TENANT-FRIENDLY COUNTRIES ARE LARGE INSTITUTIONAL RESIDENTIAL MARKETS

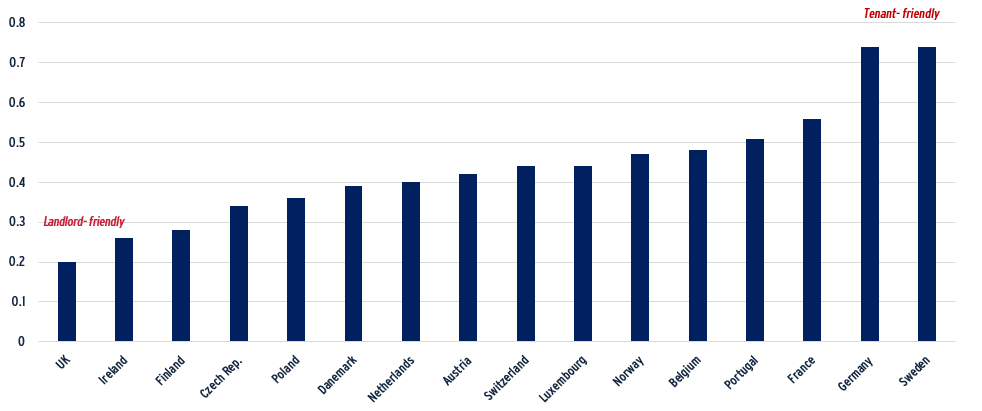

- European residential markets vary widely in terms of rental regulations. The OECD index indicates which markets are the most landlord-friendly – the UK & Ireland– and the most tenant-friendly – Sweden & Germany, which are some of the largest residential investment markets.

- Tenant-friendly countries typically have lower tenant turnover and therefore much more secure and predictable income streams for investors.

- Rental regulation is not a risk per se, as long as initial pricing takes the regulation into account. But affordability concerns across Europe are keeping housing policy high on the political agenda and need to be carefully monitored to anticipate changes.

- In Spain, the government is discussing a law that will allow regional authorities to introduce rental caps on landlords who own 10 or more residential properties. Under regional law, Barcelona has also introduced rent control mechanisms referring to a rental index.

- Since the Bundestag election on September 26th, the Social Democratic Party (SPD) is the prime contender to lead the new federal coalition in Germany. New housing policy could include an extension of the Mietspiegel look-back period and annual rental caps.

- In Sweden, the Prime Minister Stefan Löfven lost a no-confidence vote last June after supporting a reform to allow free market rent for new-built apartments.

- In Ireland, residential rents in Rental Pressure Zones are now capped at inflation (4% annual cap previously).

Rental regulation index

Sources: OECD, AEW Research & Strategy

INSTITUTIONAL INVESTORS IN BEST POSITION TO GREEN THE RESIDENTIAL STOCK

MINIMUM EPCS COULD TRIGGER REDUCTION IN STOCK

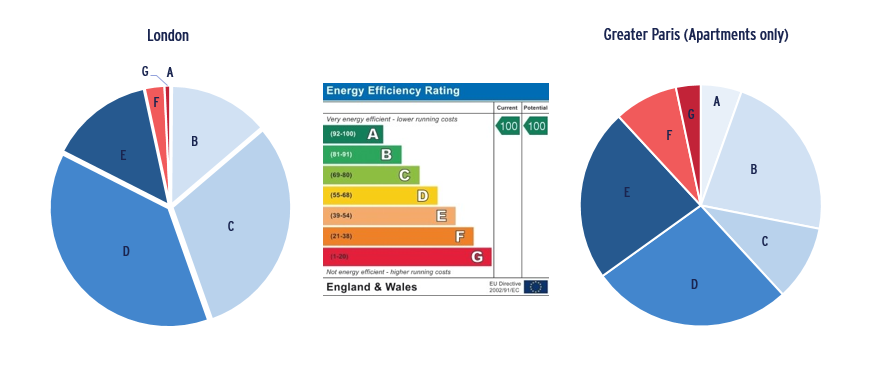

- Energy Performance Certificates (EPCs) provide information on the indicative energy performance of a dwelling, issued when the property is sold or rented. This is one of the tools used by Member States to implement the EU’s Energy Performance of Buildings Directive (EPBD) and the main source of data on the energy efficiency of the European residential stock.

- In the near future, landlords can no longer let or continue to let residential properties if they have an EPC rating below E, unless exempted. In the UK, this Minimum Energy Efficiency Standard has been implemented since April 2020. In France, the deadline is 2025 for properties with an EPC label G and 2028 for properties rated F.

- In London, around 4% of the residential dwellings have an EPC of F or G and therefore cannot be let anymore. In Paris, it is 12% of the apartment stock which will soon be unlettable unless refurbished. Please note that EPC methodologies vary between countries.

- As any measuring tool, Energy Performance Certificates are not perfect. Academic research has clearly pointed out that there is often a disparity between model-based and actual energy use - commonly known as the Energy Performance Gap*.

Energy Performance Certificates - Breakdown of the residential stock by EPC energy rating (%)

Sources: ONS, ADEME, AEW Research & Strategy

* See Cozza et al., 2020; De Wilde, 2014; Gram-Hanssen&Georg,2018; Majcen et al., 2013; Zou et al.,2018

URGE TO DECARBONISE THE RESIDENTIAL STOCK

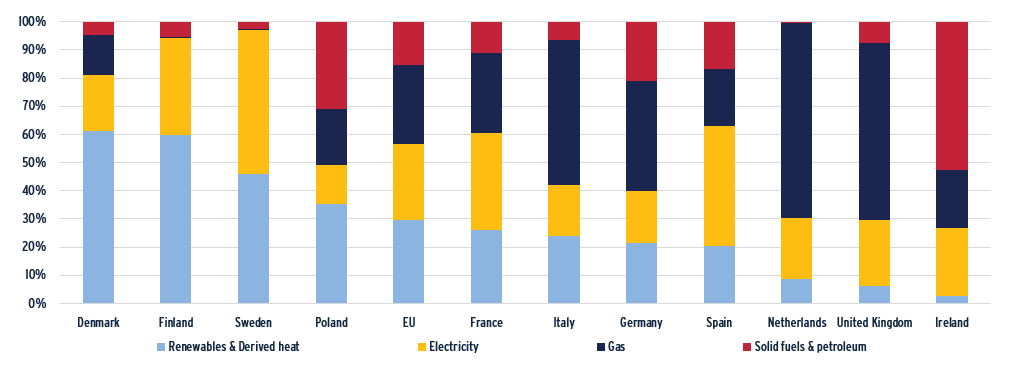

- The residential sector represents around 26% of the EU’s final energy consumption, representing the second largest consuming sector after transport, with the majority of energy (80%) used for space and water heating.

- On average in the EU, 50% of residential dwellings rely on fossil fuels for space and water heating – in particular natural gas.

- The reliance on gas is particularly high in the Netherlands, the UK and Italy. Oil is being phased out but remains significant in Poland but also Ireland. The recent spectacular increases in gas prices highlights the need to improve the energy efficiency of the residential stock, also in light of rising energy poverty levels.

- According to the Odysee-Mure datasets covering all European markets, the pace of energy efficiency improvement has been slowing since 2015. Larger homes, the need for cooling and an increasing amount of appliances have indeed increased the demand for energy. Landlords and tenants need to collaborate to achieve these reductions while maintaining costs at manageable levels.

Final energy consumption in the residential sector by energy source, 2019 (%)

Sources: Eurostat, Odyssee-Mure, AEW Research & Strategy

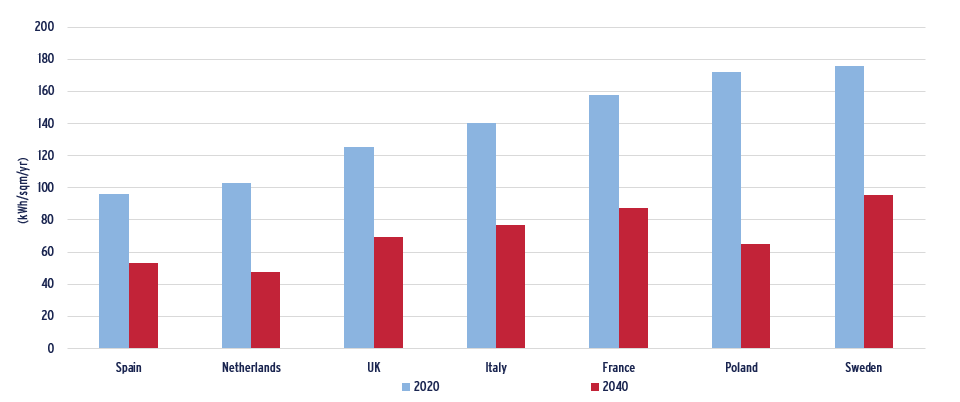

TRANSITION RISKS: STEEP REDUCTION PATHWAYS

- The reduction pathways developed by CRREM (Carbon Risk Real Estate Monitor) highlight the necessary reduction in energy intensity required to respect the Paris Accord to limit global warming to 2°C through to 2100.

- The Netherlands and Poland have the steepest reduction objectives, of 62% and 54% respectively, in comparison to 44% for France, the UK and Spain.

- The energy consumption per sqm is significantly above average in Poland and Sweden but Sweden’s high shares of renewables and district heating mean that carbon intensity is lower and therefore the reduction pathway is less steep than for Poland.

- Please note that these pathways result from a top-down approach of the Paris Accord’s targets. Regulation such as the EPBD require commercial and residential landlords in EU Member States to achieve a 50% energy consumption reduction by 2040, with 2010 as earliest reference year (up to 2019) – with an intermediary 40% reduction objective in 2030.

2020-40 Energy intensity reduction pathways for the residential sector by country (kWh/sqm/yr)

Sources: CRREM, AEW Research & Strategy

INCOME-PRODUCING RESIDENTIAL AS SUBSTITUTE TO BONDS

THE RACE IS ON TO BUILD SCALE

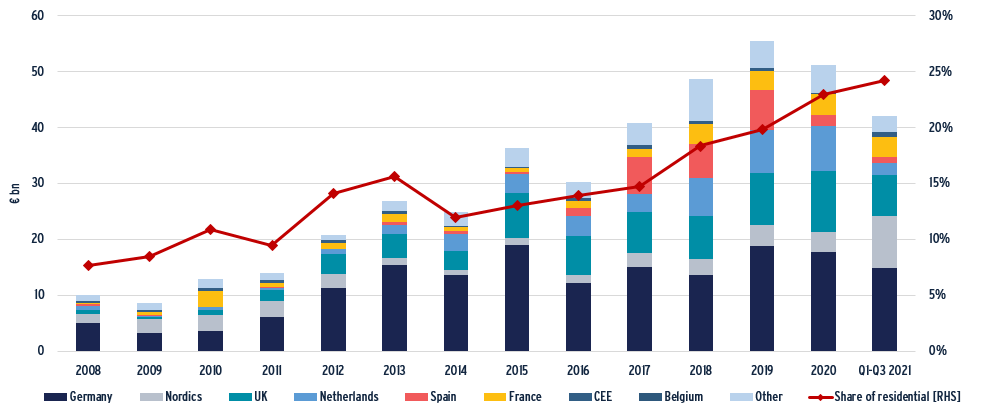

- A record of €42bn was invested in the European residential sector in the first 9 months of 2021 as European residential continues to record a greater share of institutional investors’ commitments.

- Large transactions include the acquisition by Heimstaden of a €9.1bn portfolio of residential assets mostly located in Berlin, Hamburg, Stockholm, Malmö and Copenhagen. Heimstaden, backed by Nordic pension funds, will be the second largest owner of residential assets across Europe after Vonovia following the on-going takeover of its smaller rival Deutsche Wohnen (550,000 apartments worth €80bn). More portfolio consolidation is expected. In France, AXA IM acquired 75% stake in a newly created property company in partnership with In’li, an operator of affordable housing, for €2.2bn to develop 20,000 new affordable dwellings in the Paris region over the next ten years. A large portfolio of 8,000 dwellings is also about to be sold by CDC Habitat.

- In contrast to other property types, institutional investors are facing competition not just among themselves but also from private investors. The high number of house sales today can be explained by the extra household savings during the pandemic. A large share of the institution-owned stock has also been sold apartment by apartment at a premium over the past decades. Acquiring new developments is therefore the favourite route chosen by investors to build a residential portfolio.

Residential investment volumes (€ bn) & share of residential in total volumes invested in real estate (RHS, %)

Sources: RCA, Green Street, AEW Research & Strategy

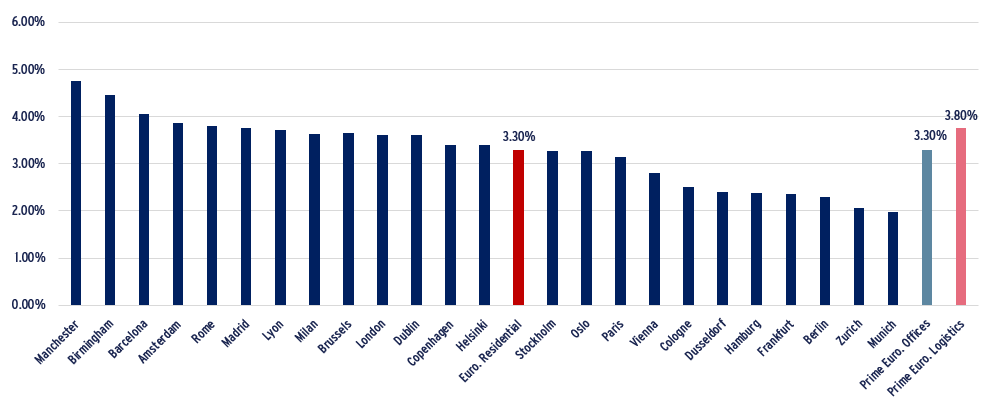

NET RESIDENTIAL YIELDS STAND AT 3.30% ON AVERAGE ACROSS EUROPE

- Net residential initial yields are very low as rental growth has been much weaker than house price growth over the past decade. Residential yields are net of operating expenses, which represents a leakage of around 25% which includes property management fees, basic repairs and maintenance, taxes and utilities.

- Net residential initial yields stand at 3.30% on average across our 24 markets. Net yields are the sharpest in markets which are highly regulated or with strong reversionary potential such as Munich. §Less regulated markets such as the UK and Spain benefit from more attractive yields.

- When comparing with prime offices and logistics, European residential yields appear relatively attractive, especially on a risk-adjusted basis.

Net residential initial yields (%) – Q3 2021

Sources: Green Street, Chatham Financial, Oxford Economics, AEW Research & Strategy

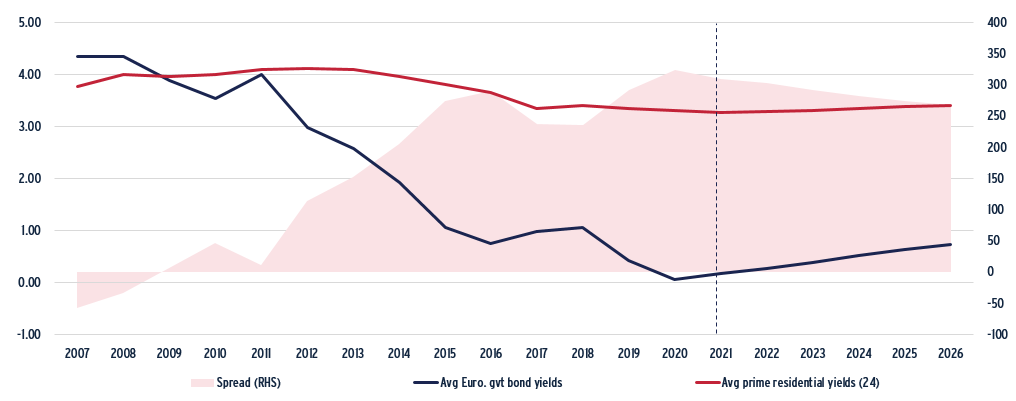

RESIDENTIAL YIELDS TO STABILISE

- Our yield forecasts in our base case scenario are based on the outlook for swap-implied government bond yields, which continue to point at lower-for-longer bond yields with inflation slowing to 1.8% from 2022.

- Net residential yields are expected to stabilise at their current levels, meaning that investors should not expect much further yield compression.

- The yield spread between residential assets and government bonds is currently wide at 310 bps, compared to 160 bps over the past 15 years. In our base case scenario, the risk premium is expected to remain high at 284 bps on average in 2022-2026.

- In a world of (still) very low bond yields, institutional investors see residential as a substitute to bonds, with potential for inflation-linked rental upside and capital growth.

Net residential & government bond yields (%) & risk premium (bps, RHS)

Sources: Green Street, Chatham Financial, Oxford Economics, AEW Research & Strategy

ATTRACTIVE RISK-ADJUSTED RESIDENTIAL RETURNS

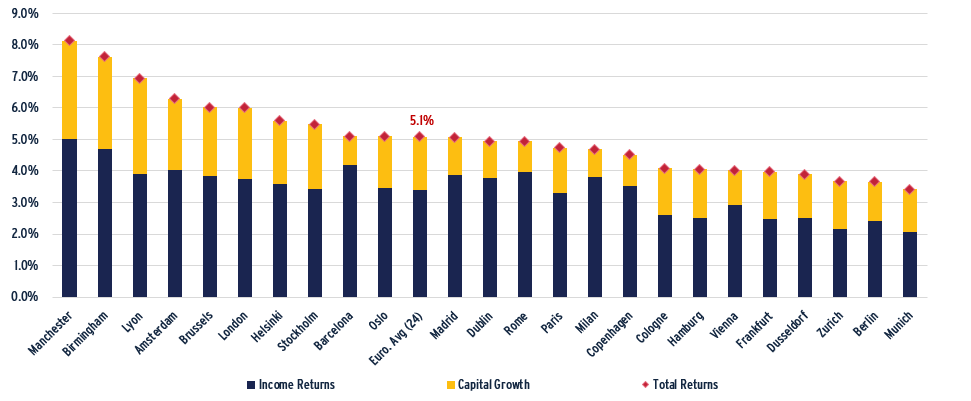

RESIDENTIAL TOTAL RETURNS RANGING FROM 3.4% TO 8.1%

- Prime total returns for the residential sector are expected to be the highest for regional residential markets such as Manchester, Birmingham and Lyon, due to higher net initial yields and stronger rental growth.

- Other outperforming markets include cities where residential markets are less regulated such as Brussels, London and Helsinki.

- Less than 4% per annum total returns are expected in the most regulated markets - the German cities, Zurich and Vienna - where net initial yields are typically very low.

Residential Total Returns Forecasts 2022-2026 (%, p.a.)

Sources: Catella, Green Street, CBRE, AEW Research & Strategy

LESS CAPITAL GROWTH EXPECTED IN THE FUTURE

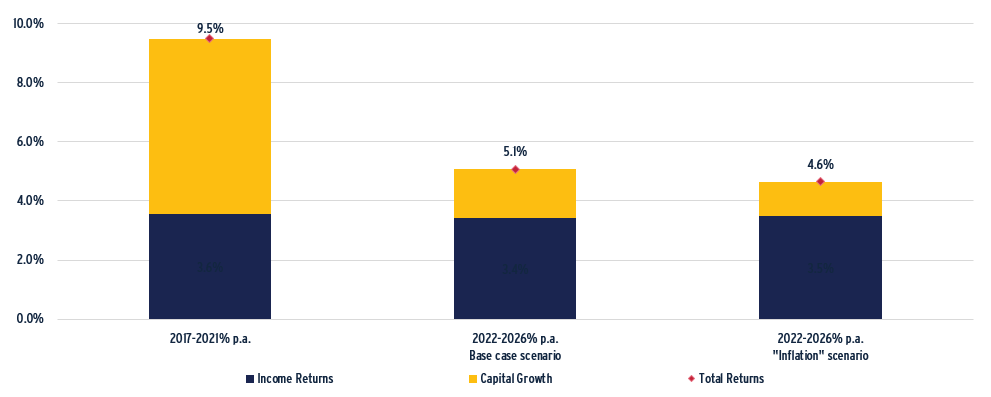

- Over the next five years, prime total returns for the residential sector are forecast to reach 5.1% pa on average in the 24 markets covered, in our base case scenario.

- Residential income returns are forecast at 3.4% p.a. in 2022-26 on average, which is close to the last five years-average (2017-21).

- By contrast, capital growth is forecast at 1.7% p.a, down from 5.9% p.a. in the previous five years. The strong yield compression recorded in the past five years is unlikely to continue in the short-term. With interest rates remaining low in our base case scenario, residential yields are expected to remain stable in 2022-2026.

- Given increasing inflation expectations, we have designed an “inflation” scenario with higher inflation assumed in 2021 and 2022 of 2.4% and 2.6% respectively and a faster government bond yield normalisation. In this scenario, the forecasts for capital growth comes down to 1.2% p.a., bringing average residential total returns down to 4.6% p.a. on average.

Prime European residential total returns p.a. (%) – 24 markets

Sources: Catella, Green Street, AEW Research & Strategy

RESIDENTIAL IN LINE WITH OTHER PROPERTY TYPES

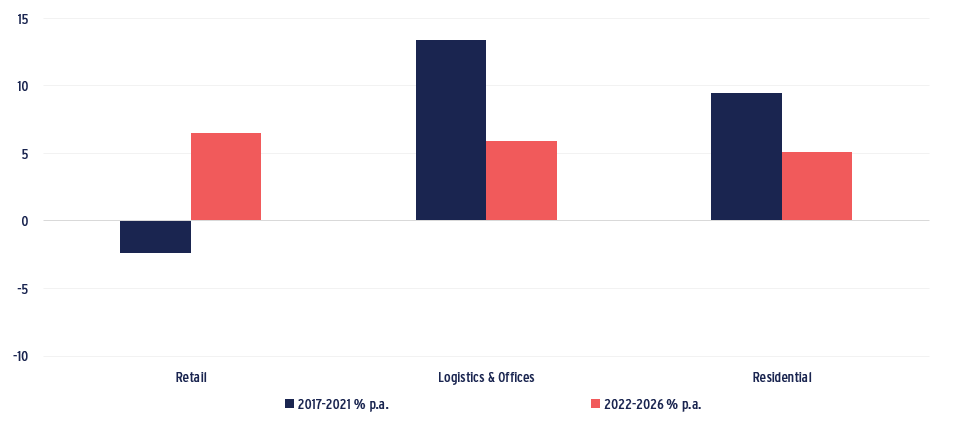

- Prime residential total returns are forecast to reach 5.1% p.a. over the next five years, in comparison to 9.5% p.a. in the past five years.

- European logistics and offices are expected to slightly outperform residential with 5.9% per annum prime total returns expected in 2022-2026.

- Retail is also expected to outperform residential with 6.5% total returns expected per annum as retail capital values have significantly adjusted in 2020 and 2021, with negative total returns recorded over the past five years.

Prime European total returns p.a. (%)

Sources: Catella, Green Street, CBRE, AEW Research & Strategy