A Great Time to Look Ahead

MIXED ECONOMIC SIGNALS AND INTEREST RATE OUTLOOK

- Volatility was defining feature of markets in H1 2023, and macroeconomic expectations have shifted since the start of the year.

- Investors went into Q2 on high alert for a recession across multiple markets, but easing downward pressures indicate an increasing likelihood of a soft landing, not just in the U.S., but also across Asia Pacific markets.

- Asia Pacific presents a varied monetary policy landscape, with possible further rate hikes in Australia, standstills in Singapore and South Korea, and easing in China. Japan is expected to maintain accommodative policy with some gradual tightening.

- AEW Research believes that the Asia Pacific region is slightly ahead in terms of economic reset and recovery. Asian central banks (outside of Hong Kong) don't typically mirror the Fed, suggesting some markets may see easing before the U.S. However base rates are likely to settle higher than their ten-year historical average.

INVESTMENT ACTIVITY DECLINES FURTHER IN Q2, H2 WILL BE MIXED ACROSS MARKETS

- Investment markets have been stagnant for eight months, but this inactivity has not surpassed the 12-month pause seen during the Global Financial Crisis before capital started moving again. Total transaction volumes for the year to end Q2 2023 amounted to $43.8 billion, which is approximately 43% lower compared to the same period last year and 13% lower than the volumes recorded in the same period in 2020. (These figures may change slightly as more data becomes available.)

- While there is variation in these numbers, most markets slid lower. Compared to the same period last year, Australia saw the steepest decline at 65%, followed by China at 53%. However, Japan's deal volumes remained relatively stable in local currency, and specifically Singapore's industrial market was up around 62% versus the same period last year, logging nearly 30 enbloc trades in H1 2023.

- Positively, Asia Pacific's deal volumes for 2023 have, so far, outperformed the U.S. and Europe, which experienced a roughly 60% decline compared to the same period last year.

- There is more certainty today on where interest rates will settle. Valuers are beginning to adjust downwards, even in the absence of concrete evidence, which may lead to increased trading activity in the second half of the year. While re-pricing expectations have become more bearish since the beginning of the year, this presents a solid opportunity to acquire assets at discounted prices.

- According to Preqin, the post-GFC vintage funds in the region have been highly successful, averaging returns of 16% IRR and 1.6EM.

LOOK FOR GOOD VALUE AND GROWTH

- Some markets have already moved into downward pricing corrections while others appear to be on the cusp. We anticipate buying opportunities at good value across several markets, however underlying income growth or ability for managers to add alpha (through adaptive reuse, implementing low carbon strategies etc.) will be key to establishing healthy returns.

- New economy sectors with favorable lease structures will likely remain in the spotlight alongside multifamily and industrial assets in some key markets. There is also likely to be increased interest in re-priced office properties.

- Beyond 2024, return in income growth and potential for cap rate compression is supporting a better total return outlook, averaging 7% p.a. over 2024 to 2027. Based on AEW's research, the most positive outlook for this period will be in logistics and offices.

ASIA PACIFIC INVESTMENT VOLUMES

2019 TO JUNE 2023

Source: AEW Research, JLL, PMA, Real Capital Analytics, as of end June 2023

Note: Investment volumes measure income producing investments across AEW’s target markets. There is no assurance that any prediction, projection or forecast will be realized.

ASIA PACIFIC TOTAL RETURN

2021 TO 2027F

Source: AEW Research, JLL, PMA, Real Capital Analytics, as of end June 2023

Note: Investment volumes measure income producing investments across AEW’s target markets. There is no assurance that any prediction, projection or forecast will be realized.

Varied Economic Tailwinds and Headwinds

GLOBAL GROWTH SLOWDOWN, MIXED OUTLOOK IN ASIA PACIFIC

- Economic resilience in the U.S. and Europe has led to a slight upward revision in growth forecasts. While the West's 2023 growth forecasts have increased, it could curb growth from 2024 onwards if policy rates remain high.

- Asia Pacific’s outlook is diverse:

- Higher interest rates in Singapore, South Korea, and Hong Kong are tempering inflation and moderating 2023’s growth.

- In Australia, high overseas migration rates and a still strong labor market have kept inflation levels high, although the recent Q2 2023 print of 6% indicated a slowdown from the previous quarter.

- China is facing declining domestic demand and credit growth, which has contributed to growing deflationary concerns, spurring calls for more fiscal support.

- Conversely, Japan's H1 economic performance exceeded predictions, with rising corporate profits and increasing wage inflation.

- Aside from the differences by country, we expect an economic recovery in Asia Pacific to emerge faster than the other regions, with growth improving over the forecast period.

CONSUMER SENTIMENT SHIFTING LOWER IN 2023

- Business and consumer sentiment surveys have started to go their separate ways across several markets. At the same time, other key indicators such as bankruptcy filings, PMI indicators and retail sales have started to paint a bleaker picture of the economic environment in the near-term.

- Employers globally are also dialing back their hiring plans; however, talent shortages remain high in Australia and Hong Kong.

UNEVEN HIKING CYCLES AND MORE LOCAL CURRENCY WEAKNESS

- Most central banks in the region are done, or near the end of their hiking cycles.

- In Japan, the BoJ unexpectedly allowed 10-year JGBs to rise to 1.0% in late July. However, this is not seen as a move away from monetary easing. Most now anticipate the next policy change in Q2 2024, rather than any further action in 2023.

- China has been easing its monetary policy in the face of slowing growth and even implemented several rounds of stimulus measures to boost domestic growth. To-date, these have been viewed as inadequate.

- As most Asian banks are unlikely to mirror the Fed, interest rate differentials will likely sustain USD strength. We see the recent USD weakness as short-lived, suggesting local currencies' depreciation against the USD (as seen in Q1), is likely to continue.

ASIA PACIFIC GDP GROWTH REVISIONS

2023 TO 2025

Source: Oxford Economics, Bloomberg & AEW Research, as of 26 July 2023

Anticipation Mounts for the Pricing Reset

Office

CAUTION AND COST-EFFECTIVENESS PREVAIL, SOME BRIGHT SPOTS

Leasing sentiment is cautious, with effective rents in most markets falling between 0.5% and 3% q-o-q. Lease incentives are generous and expected to continue for the next 12 months. Prime grade assets are performing better than secondary counterparts, and in Greater China, new construction of prime assets outside the CBD continue to support the trend of relocation/decentralization to more affordable markets. Seoul, Brisbane and Perth have the most favorable occupier fundamentals today. In Seoul vacancy rates are at their lowest in more than a decade while in Perth and Brisbane tenant demand is surging from investment in traditional and renewable resources.

INVESTMENT VOLUMES HOLD UP BETTER IN ASIA PACIFIC (VS OTHER REGIONS), REPRICING EXPECTATONS TURN MORE BEARISH

Investment interest in the sector is out of favor, but year-to-date liquidity in Asia Pacific is holding up better than Europe and U.S. However, the forecasted repricing in the sector for Asia Pacific has turned more bearish, given recent reported deal evidence and the expectation of prolonged higher interest rates. We believe the repricing will be strongest in Australia and China (down 20 to 30%) where there is more refinancing and liquidity stress, while a larger proportion of cash-rich owners in Hong Kong and Singapore could prevent significant declines in asset values. Meanwhile, even though overall deal activity in Seoul decreased substantially, it is the most actively traded office market globally (year-to-date) with no evidence of pricing reductions yet.

Logistics

RENT GROWTH FORECASTS UPGRADED AGAIN IN AUSTRALIA AND SINGAPORE

Prime facilities across Australia’s eastern seaboard markets and Singapore have close to zero vacancy, keeping occupier markets extremely landlord favorable. Both saw rent growth expectations upgraded again for the year ahead. Meanwhile oversupply concerns are greatest in North Asian markets. In Greater Seoul, the oversupply issue is concentrated in Incheon, particularly with cold-chain facilities. AEW has learned that some landlords are contemplating converting cold to dry space or are offering higher incentives (in the range of three to five months) to attract tenants and fill vacancies.

WHILE SOME MARKETS WILL REPRICE, OTHERS REMAIN STABLE

Yield movements have been divergent in the last 12 months. Compression in Japan (~15 bps), flat in Singapore and expansion in Australia and Greater Seoul (~70 to 150 bps). Despite the increase in yields for Australia, the pricing for short Weighted Average Lease Expiry (WALE) assets remains somewhat elevated due to strong income growth potential. Meanwhile in Greater Seoul, the investment markets had its slowest six months as occupier markets and financing terms remain challenging.

Retail

ALTHOUGH CONSUMER SENTIMENT WANES IN SOME MARKETS, INVESTMENT ACTIVITY HOLDS

Retail leasing markets in Singapore and Hong Kong have improved over H1, while in Australia the outlook is mixed across the subcategories. In the near-term, we expect tourism-orientated retail to lead in Singapore and Hong Kong while in Australia, malls with smaller discretionary components should do better.

After some large deals in Q1, investment markets turned quiet in Q2, with mostly smaller deals transacting. Higher debt costs and weakened consumer outlook have also kept institutional investors at bay. In Australia, 17 of the 28 deals closed in the quarter were priced below AUD 50m. In Singapore shophouses by private investors made up the bulk of transactions while in Hong Kong the majority of deals were strata with only one enbloc deal – West9Zone Kids traded at a 5.0% entry yield.

Multifamily/ Build-to-Rent

STRONG MIGRATION AND IMMIGRATION SUPPORT DEMAND, ROBUST CROSS-BORDER APPETITE

In Japan, migration patterns have already returned to pre-pandemic levels, supporting multifamily demand in the major cities. Meanwhile in Australia, extremely strong overseas net migration, low vacancy rates and housing unaffordability is exacerbating pent-up demand conditions. Both markets are exhibiting strong occupier fundamentals today.

Investment activity in the sector should stay healthy, especially by foreign capital. Today, Japan offers the widest yield spreads globally, while in Australia, recent positive changes in tax conditions for foreign investors and proof of concept (with some successfully operating properties) will likely incentivize further investment.

Office

AUSTRALIA: UNEVEN RECOVERY, REPRICING IS IMMINENT

- Occupier demand is improving but remains far below historical trends. Brisbane and Perth were least impacted by work from home (WFH) practices and have better leasing conditions today.

- Demand is gravitating to fitted suites in better quality stock at the expense of secondary assets which have larger vacancy pockets and is likely to lag the prime rent recovery.

- Transaction markets in H1 were quieter than initially expected. Bid-ask spreads remain wide, which is drawing out the yield softening cycle as valuers wait for more evidence. Markets with more private capital (like Perth and Brisbane) could move faster.

SINGAPORE: MARKET REMAINS QUIET, POTENTIAL REBOUND IN 2024

- Both leasing and investment markets remain quiet. Vacancy rates increased as anticipated in 2023 due to new construction in the CBD, but this is expected to be temporary. Beyond 2023, there is potential for a decent recovery as economic growth resumes a steady track. During 2024 and 2025, existing leases should revert 20% higher than in-place rents.

- In the absence of institutional investors, HNWI individuals, family offices and buyers from mainland China have been active in the strata-titled office market (with unit prices ranging from SGD40 to 80m)

HONG KONG: MARKETS STAY TENANT FAVORABLE, BUYERS UNENGAGED

- Rental growth forecasts have been revised down to reflect weaker than expected demand from mainland China. At the same time, the large supply due to be delivered on Hong Kong Island in 2023 will likely add vacancy and downward pressure on rents.

- The market has stayed unengaged on deals. Mainland buyers have instead been active in the strata-titled market, where they often avoid taking on debt and pay in full cash.

- CHINA: WEAK LEASING AND INVESTMENT MARKETS

- Large supply and high vacancy will continue to place downward pressure on rents. The market generally lacks any positive tailwinds, but there are some submarkets like Qiantan, and Liujiazui in Pudong, Shanghai and East Second Ring Rd in Beijing that are doing slightly better.

- Few transactions have occurred in H1 2023 but offshore refinancing stress has risen and we expect more dispositions in H2 2023, potentially at substantial discounts.

SOUTH KOREA: POSITIVE OCCUPIER MARKET CONDITIONS SUPPORTS PRICING

- The leasing market remains in a solid position and limited supply in the next three years in the three core markets can support rental growth. Loss-to-lease is circa 20 to 30% over the next two years, presenting strong income growth potential.

- South Korea’s office market has defied expectations of downward price pressure. Riding on the strength of the occupier market, recent transactions have reflected pricing that breaks new records. AEW understands more deals are due to transact in H2 2023 and end-users are likely to be active buyers.

JAPAN: SUPPLY RISKS CONTROLLED WITH MODERATE TENANT DEMAND

- In Tokyo, Grade A demand has improved since the start of the year, which has helped support a marginal decline in vacancy rates. Supply peaks in 2023 and 2025 however will keep vacancy above the long-term historical average till 2027 at least. Under these conditions, we believe rental growth is unlikely.

- Investment volumes in Tokyo have come down, but ostensibly held up better than other markets. We expect investors to continue to be selective on assets, Grade B could have more activity as tenants are sticky and supply is lower.

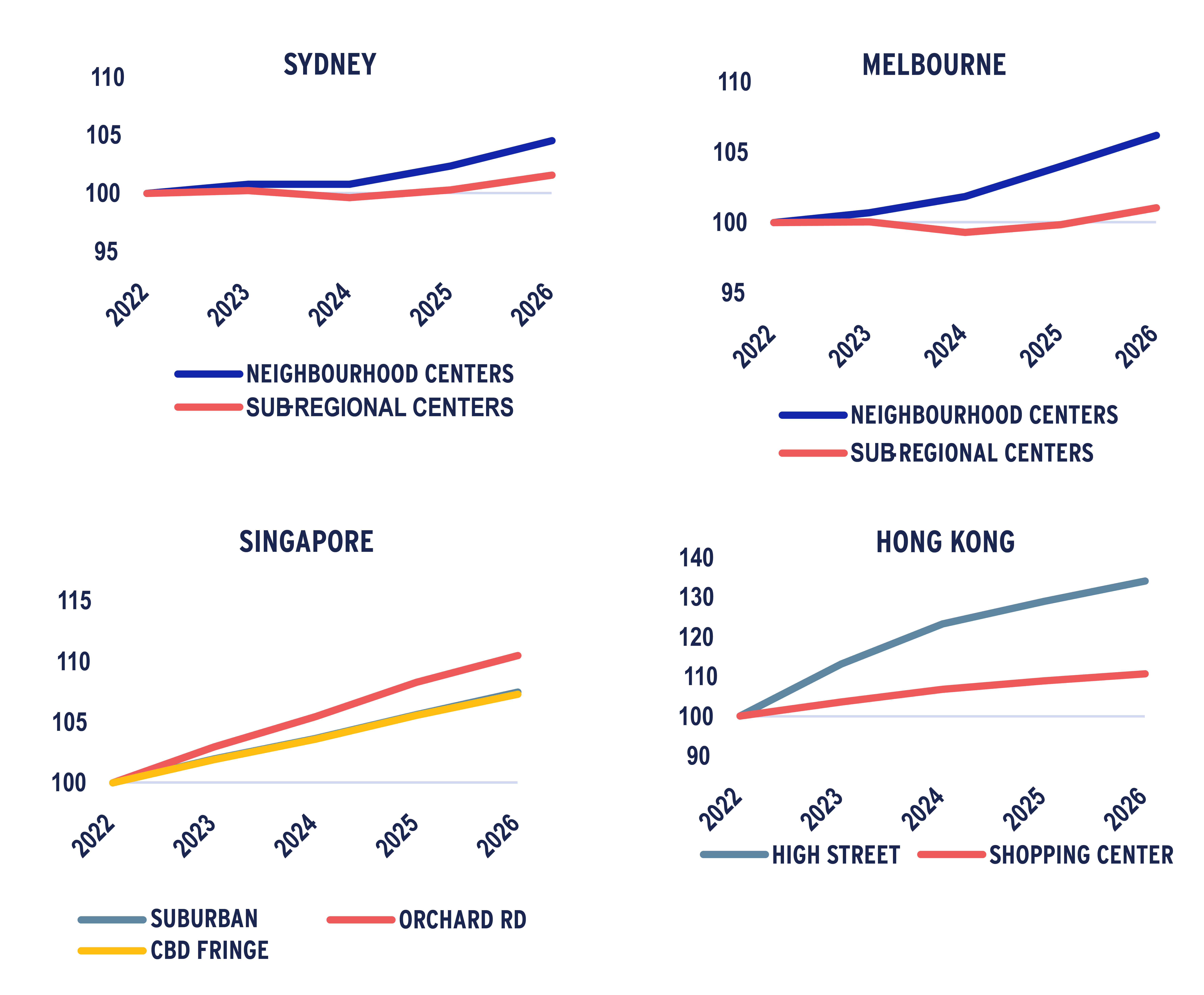

OFFICE RENT INDEX

2022=100

Source: AEW Research, JLL, Q2 2023

Logistics

AUSTRALIA: NEAR-TERM RENT GROWTH UPGRADED, YIELD EXPANSION PLAYING OUT

- Rent growth for H1 2023 has exceeded prior forecasts and consensus growth has been upgraded for the year to 15% to 20% across the eastern seaboard markets.

- While demand has slowed, the market remains structurally undersupplied and extremely attractive for asset owners.

- Investment activity improved q-o-q but still lacks depth on account of higher interest rates. Some portfolios up for sale in H2 could add to investment volumes. Yields have increased by 150 bps since peak cycle but in terms of capital values, generally only long WALE assets have seen value declines, ranging from 10 to 12%.

SINGAPORE: FAVORABLE OCCUPIER CONDITIONS, MORE INVESTORS TARGET THE SECTOR

- Demand for prime facilities remains strong, leading to full occupancy levels and limited options for 3PLs looking to expand. The need for just-in-case inventory continues to drive demand, and with limited supply expected in the coming years, annual rental growth has been revised upward to 14% in 2023, with projections of 3% to 5% growth in 2024 and 2025.

- The sector continues to be actively traded driven by attractive yield spreads (to cost of debt) and the favorable rental outlook. Rent reversions over the 2023 to 2024 period range from 10 to 15% for prime facilities. The sector is expected to see some yield compression (especially for facilities with land tenures above 20 years).

HONG KONG: VACANCY REMAINS LOW

- Warehouse rents were flat over the quarter while leasing sentiment declined due to weakness in re-export trade. Beyond 2024 however, there could be several avenues for growth, including demand from cosmetics and pharmaceutical trades as well as the expansion of the electric vehicle market.

- There were only three enbloc deals transacted since Jan 2023 (of value USD 50M and above), with no cross-border buyers. New-economy conversion plays (to data centers, cold-storage, or self-storage) remain interesting, but interest rates would probably need to fall by 50 to 100 bps to reignite interest.

SOUTH KOREA: ON-GOING SUPPLY DELAYS, MARKETS RE-PRICE

- Demand was positive, but there has been a notable decrease in leasing activity, especially from the e-commerce groups. Large new completions have also caused vacancy spikes, especially in the Western region. Cold remains strongly oversupplied with a vacancy of 42% in contrast to dry which is just 10%.

- Prior construction delays are advancing faster than expected which means supply risk for the next 12 months is increasing. Still some markets with limited new construction continue to exhibit low vacancies and face rent increases.

- Debt costs have lowered in the last six months, but investment activity remains limited. Transaction yields held a wide range, but in general have expanded by 70 to 120 bps since peak pricing in 2022.

JAPAN: MORE FAVORABLE CONDITIONS IN INNER-CITY SUBMARKETS

- Both Greater Tokyo and Greater Osaka are going through a supply cycle, with new construction expected to peak over 2023 and 2024. As supply is concentrated in the outer lying regions, the inner-city submarkets should remain landlord favorable.

- Investment activity in the last six months has been relatively upbeat and increased y-o-y. We expect further yield compression in the sector for 2023.

LOGISTICS RENT INDEX

2022=100

Source: JLL, as of Q2 2023

Retail

AUSTRALIA: RETAIL SALES STRONG UP TO Q4, POSITIVE YIELD SPREADS

- Inflation and rising interest rates have had their intended impact on consumer spending. Retail sales have declined further 1.4 y-o-y in Q2 2023, while consumer confidence surveys indicate cautionary spending in the near term.

- Vacancy rates across all retail subcategories today remain higher than historical average. In Q2 2023, regional malls had the lowest vacancy while CBD retail was close to 16%, the highest it has ever been.

- Rents for non-defensive assets are likely to come under pressure this year. In general, landlords remained focused on managing vacancy risk and can be very flexible on lease terms. AEW understands leases are taking longer to conclude with incentives in some cases going up to 40%.

- Various capital sources are showing interest in the sector, but private domestics remain the most dominant purchasers. Yields are expected to soften between 15 to 50 bps over the next 12 months with assets with larger discretionary components on the large end.

SINGAPORE: RENTS RECOVERY CONTINUES IN 2023

- Improving tourist numbers and healthy domestic spending are contributing to a better near-term outlook for the retail sector. For tourists, despite a shortfall from mainland China year-to-date, there are y-o-y increases in both arrivals and spending from other countries like South Korea, Japan and Philippines.

- Leasing activity in Q2 was up, and led by F&B, beauty, luxury and medical services. Both prime and suburban-located malls benefited, and vacancy rates have declined consistently since June 2022. Vacancy rates for suburban malls today are the lowest since 2014.

- With the limited supply and better leasing conditions, retail rents should continue to recover throughout the year. However, weak economic growth will likely limit the upside.

- The capital markets remain subdued, with most transactions this year involving shophouses purchased by private investors. It is anticipated that activity will decline further in H2 following a recent amendment that now requires foreign buyers to pay a 60% stamp duty on a broader range of properties (which includes non-strata residential and commercial zoned developments)

HONG KONG: TOURISM-LED RECOVERY TO FORM

- After years of weakness, Hong Kong is experiencing a revival in retail leasing. Retail sales were up 16% y-o-y in May 2023 and this helped support leasing activity while vacancies further declined. Rents increased fastest in high-street shops, by 6.0% q-o-q, but remain about 20% below pre-COVID levels.

- Like Q1, demand was led by beauty/pharmaceutical chains, F&B and mass fashion, but there has been a notable increase in luxury retailers re-engaging with landlords.

- Domestic, non-institutional investors continue to comprise the bulk of capital interested in the sector, especially for high-street shops. Investment sentiment from this group of buyers will likely remain healthy in 2023, especially as good bargain buys are available in the market.

RETAIL RENT INDEX

2022 =100

Source: JLL, as of Q2 2023

Multifamily

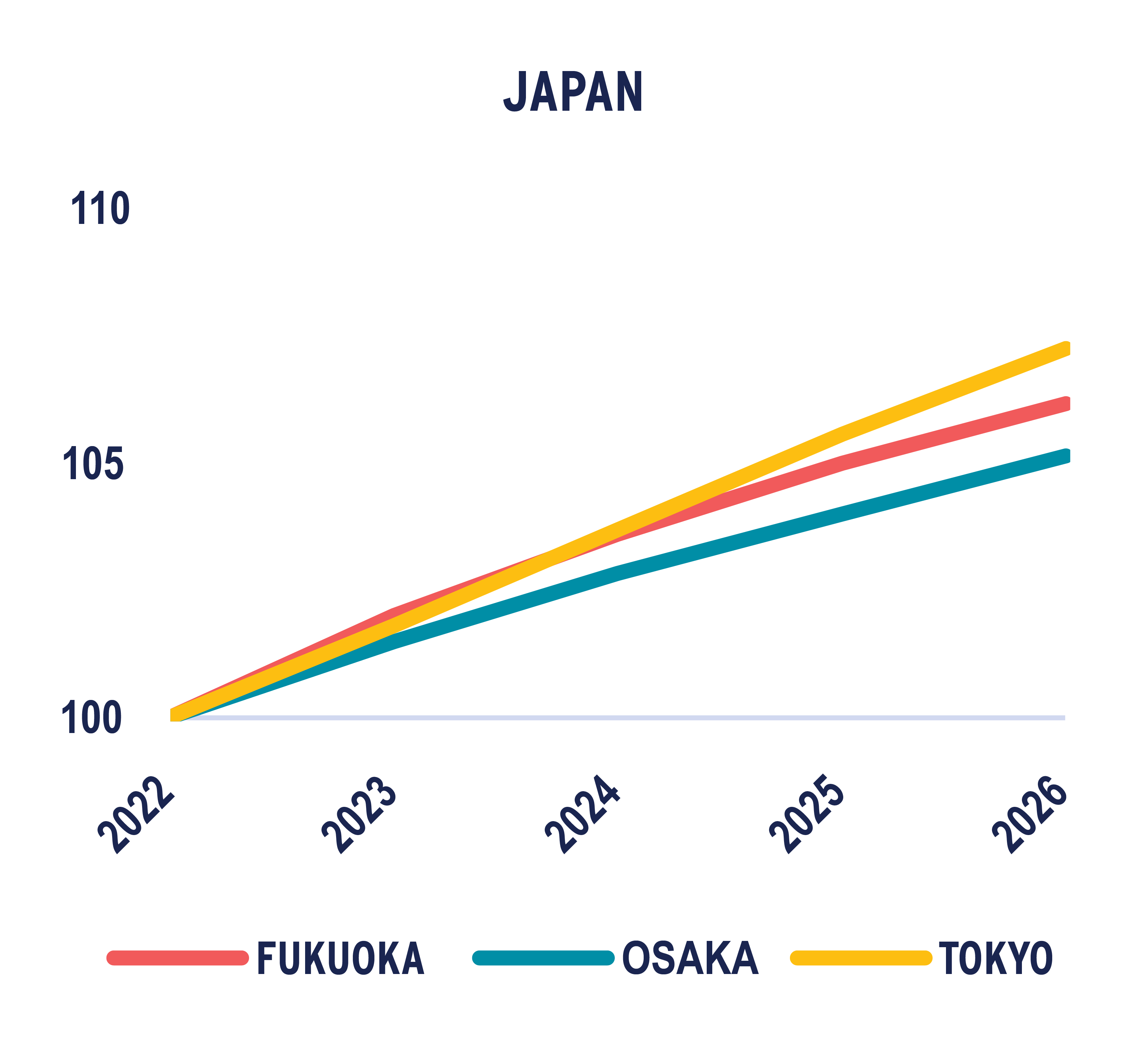

JAPAN: RETURN TO PRE-PANDEMIC CONDITIONS

- Net migration trends continue to recover and leasing conditions, especially in inner city areas have improved substantially from one year ago.

- In Tokyo, occupancy rates are up, and several developers have pivoted to larger-sized units given their popularity and the faster-paced rental growth during the pandemic years. The inner-east and Central 5 wards are favored due to stronger population growth.

- Across the regional cities like Osaka, Fukuoka and Nagoya, the major REITs have also reported occupancy increases from the start of the year.

- For 2023, rents are expected to increase the most in Tokyo and Fukuoka (due to stronger population growth), between 2 to 3%, while Osaka and Nagoya see smaller increases of 1 to 2%.

- Investment interest in the sector remains healthy as yields over debt costs still offer favorable spreads. Some of the larger investors during 2019 and 2022 are now net sellers. Yields compressed by about 10 bps y-o-y in 2022 and should hold flat or compress mildly in the range of 5 to 10 bps in 2023.

AUSTRALIA: POSITIVE FUNDAMENTALS, FOREIGN PARTICIPATION TO GROW

- Factors contributing to pent-up demand conditions in Australia’s rental housing market include– strong overseas migration (the bulk of which are students), chronic undersupply, and purchasing unaffordability.

- Rents have increased sharply across all capital cities, strongest in Sydney and Melbourne, up between 18 to 23% y-o-y in June 2023.

- With several successfully operating BTR facilities in the country, we believe the proof of concept will give confidence to further investment. AEW understands that the rental premium for BTR (compared to BTS) is about 15 to 20% and is expected to remain constant for some time.

- Further with the withholding tax rate for BTR investment through foreign MIT vehicles reduced from 30% to 15% (effective of July 2024), participation is expected to grow.

MULTIFAMILY RENT INDEX

2022 =100

Source: PMA, as of Q1 2023

For more information, please contact:

GLYN NELSON

Managing Director, Head of Research and Strategy, Asia Pacific

glyn.nelson@aew.com

+65.6303.9016

HANNA SAFDAR

Assistant Director, Research and Strategy, Asia Pacific

hanna.safdar@aew.com

+65.6303.9014

JAY STRUZZIERY, CFA®

Head of Investor Relations

jay.struzziery@aew.com

+1.617.261.9326

This material is intended for information purposes only and does not constitute investment advice or a recommendation. The information and opinions contained in the material have been compiled or arrived at based upon information obtained from sources believed to be reliable, but we do not guarantee its accuracy, completeness or fairness. Opinions expressed reflect prevailing market conditions and are subject to change. Neither this material, nor any of its contents, may be used for any purpose without the consent and knowledge of AEW. There is no assurance that any prediction, projection or forecast will be realized.