DESPITE HIGHER INFLATION, EXCESS YIELD SPREAD FOR RESIDENTIAL TO REMAIN ATTRACTIVE

- The recent increase in inflation is impacting residential real estate in a number of different ways:

- Households’ ability to pay higher residential rents in the short-term is reduced, as long as wage growth remains moderate.

- Construction costs are going up, which might limit an already tight supply pipeline in already low vacancy markets.

- New rules on embodied carbon limits for new residential developments are likely to increase construction costs further.

- Higher energy and commodities prices translate into increasing capex, which will negatively impact net operating income.

- Despite these inflation impacts, the existing imbalance between supply and demand is likely to continue and perhaps worsen. Based on this, our latest forecast for 2022-26 residential rental growth comes in at 2.6% p.a., still above inflation (2.4% p.a.)

- Residential investments will be impacted by the outlook for bond and property yields. In our stagflation scenario, the ECB is likely to keep interest rates rises more limited (lower-for-longer) than the BoE and Fed. This is also based on the lower wage driven inflation in Europe.

- As a result, our residential yields are forecasted to show limited increases from current levels in the next five years, growth in capital values remains but is lower than in the previous five years.

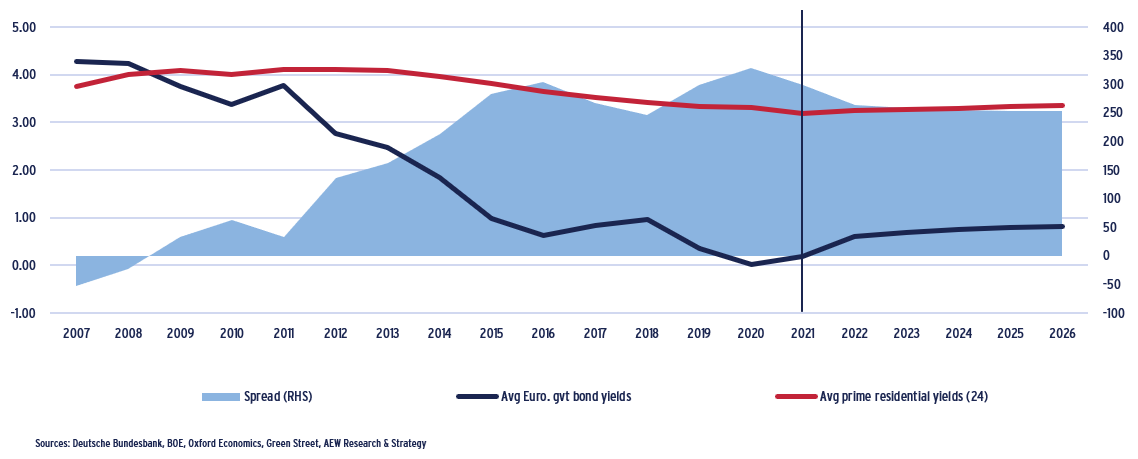

- On the income side, the spread between residential yields and government bond yields is expected to remain attractive at 260 bps on average in 2022-2026.

- In our base case stagflation scenario, we anticipate European residential total returns to reach 5.0% p.a. on average over the next five years. Expected returns will be based on modest capital growth and robust income returns.

- With residential seen as a substitute to bonds by many investors, we expect demand to remain strong, with invested residential volumes reaching record high levels in 2021 in Europe.

- Student and senior housing growth has been solid, offering the benefits of a single, long and triple-net commercial lease to investors.

- A closer look at the largest market in Europe confirms that the Paris residential market has survived the Covid pandemic with limited negative impact on prices and a recovery in rents.

Net residential & government bond yields (%) & risk premium (bps, RHS) - Europe

RISING INFLATION TO LIMIT SUPPLY AND RENTAL GROWTH

DISPOSABLE INCOME TO BE HIT BY HIGHER INFLATION

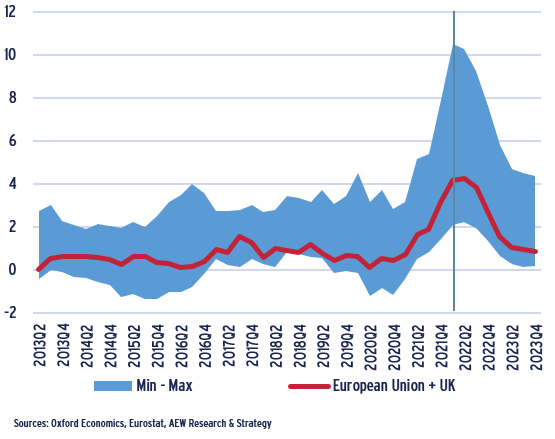

- EU and UK inflation increased significantly at the end of 2021 and at the start of 2022, with Eurozone consumer price inflation reaching 5.8% in February.

- The Ukrainian conflict will lead to a further increase of energy and other commoditiy prices, including food.

- The latest Covid lockdowns in China could also exacerbate supply problems. As a result, inflation in the EU27 + UK is now expected to peak at 4.2% in Q1 2022 before slowing to 1.5% from Q1 2023.

- However, in this uncertain geopolitical environment, inflation forecasts are likely to be revised substantially upward in the coming months.

- In Europe’s private-rented sector, households already dedicate 24% of their income to their rent on average (excluding social tenants).

- Higher inflation will reduce households’ purchasing power. Passing on some of this inflation to tenants might therefore become difficult, especially in markets with rent regulations and absolute rental caps in place.

CPI Inflation (%) – 19 countries

ECB TO KEEP RATES LOW AS INFLATION LESS WAGE-LINKED

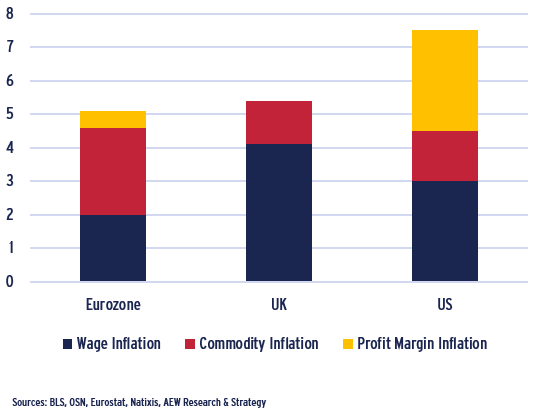

- The breakdown of inflation in Eurozone, the UK, and the US highlights that there are very different dynamics at stake.

- In the Eurozone, more than half of inflation is currently driven by energy and commodity inflation, while the wage growth component dominates in the UK and in the US. In the latter, inflation is also driven by companies’ profit margins.

- This should be a solid argument to allow the ECB to keep interest rates on hold for longer or limit the size and number of increases. Increasing policy rates also will likely not have a significant impact on Eurozone inflation, which is more supply-led and less demand-led, in contrast to the UK and the US.

- The slowing rental growth expected as a result of the war in the Ukraine via lower disposable incomes is therefore expected to be offset by lower for longer property yields, supporting residential capital values going forward.

Breakdown of inflation – January 2022

SUPPLY EXPECTED TO REMAIN LOW AS PERMITS LAG

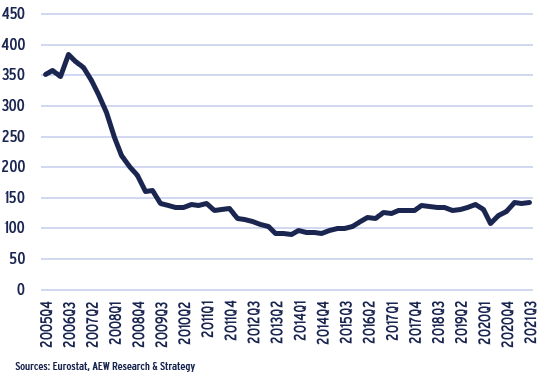

- As a consequence of the Covid-19 crisis, the number of residential building permits filed in the EU27 + UK dropped in the first half of 2020. There was a rebound from Q4 2020, with the number of permits issued now close to their pre-crisis level overall in Europe.

- However, there are wide differences between countries. Sweden, Poland, Czech Republic, Portugal and Finland have experienced a strong rebound in permits since the end of 2019.

- In contrast, the number of residential building permits filed are still significantly down in Austria, Denmark, Ireland, Germany, Belgium and France.

- The most supply constrained cities might become even tighter than before.

- Finally, with construction costs increasing significantly, building permits might not even translate into new residential developments. Developers profitability might be impacted to such an extent, especially if rents cannot increase further as tenants’ purchasing power is insufficient.

EU27 + UK - Residential building permits index

INCREASING CAPEX TO IMPACT NET OPERATING INCOME

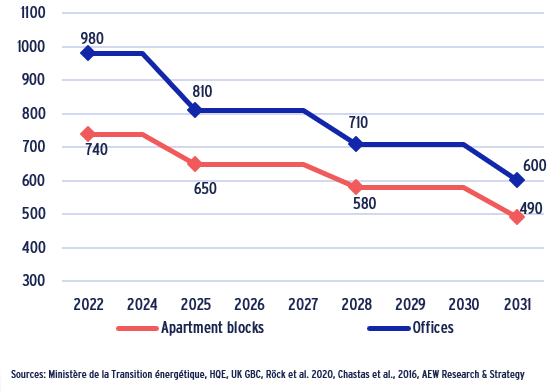

NEW EMBODIED CARBON RULES MIGHT INCREASE COSTS

- Focusing on operational carbon only is insufficient to substantially lower carbon emissions. This is because the embodied carbon emissions arising from manufacturing, transporting and processing building materials typically represent around 20-25% of total CO² emissions in a standard building’s life cycle but between 60% and 90% for highly energy-efficient buildings.

- New stricter regulations are being put in place to address this. The Netherlands, France and Denmark currently have the strictest building regulation in place with CO² limits for new buildings. Finland and Sweden should follow, while in Germany and in the UK these limits only apply to public buildings sofar.

- In France, the building regulation for new construction “RE2020” implemented from 2022 is for the first time taking into account the life-cycle carbon emissions, with maximum levels for embodied carbon emissions to be gradually reduced by respectively 34% and 39% by 2031 as shown in the chart.

- This means that developers will have to do a life cycle assessment for every new building, which might increase construction costs.

Embodied carbon limits in France for new-built residential and offices (kg CO² eq/sqm/yr)

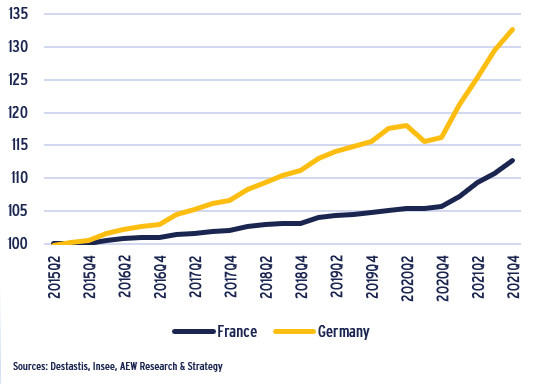

RISING CAPEX LOWER NET OPERATING INCOME

- Net operating income will be reduced by the increasing capex as the cost of energy and other inputs for construction materials such as metals increase.

- Residential capex have increased by 14% and 7% year-on-year in Germany and France respectively in Q4 2021.

- Rising construction costs also mean higher replacement costs. This will support capital value growth of existing assets. Some new developments could be delayed or cancelled if there is too much uncertainty around prices or procurement of key materials.

- On a positive note, these trends are likely to fast track the development of the circular economy and encourage recycling of construction materials.

Residential Capex – 100 = 2015

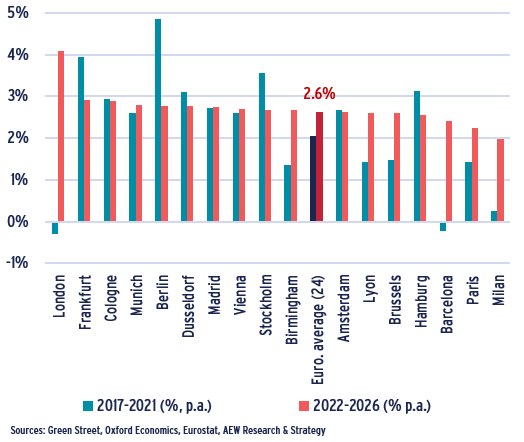

2022-26 RENTAL GROWTH EXPECTED AT 2.6% PER ANNUM

- At 2.6% p.a. on average, residential rental growth expected between 2022 and 2026 is expected to be above inflation (2.4% p.a.) as the imbalance between demand and supply continues.

- This 2.6% compares favourable against the 2.1% p.a. average rental growth over the past five years across our 24 market coverage.

- London, the German cities, Madrid, Vienna and Stockholm are expecting to outperform the European average.

- London residential rental values are bouncing back after experiencing rental declines during the lockdowns.

- In contrast, Helsinki, Milan, Paris and Barcelona are forecast to underperform the European average.

Residential rental growth (p.a) (%) -2017-2021 vs 2022-2026

STRONG INVESTOR DEMAND TO CONTINUE FOR DEFENSIVE SECTOR

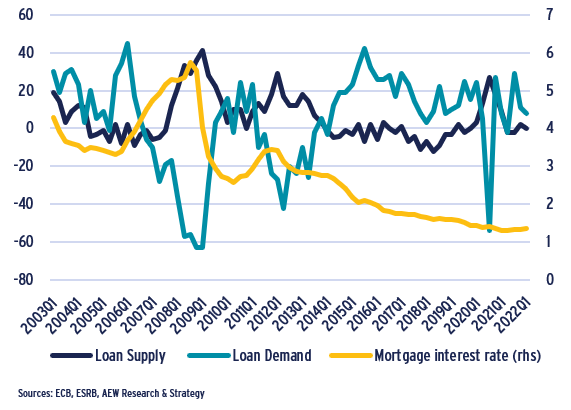

MORTGAGE RATES REMAIN SUPPORTIVE FOR NOW

- According to the ECB lending survey, loan demand for house purchase dropped significantly during the lockdowns, but recovered in 2021.

- Loan supply for house purchase remains in line with historic average although a number of central banks have announced tighter controls.

- In Germany, ultra-low borrowing costs have fuelled a strong increase in house prices of 12% in Q3 2021. As a result, BaFin recently raised the countercyclical capital buffer from 0% to 0.75% by Feb 2023. A supplemental 2% capital buffer will be introduced for residential mortgages.

- In France, the Banque de France has capped the maximum loan duration to 25 years and the debt-service-to-income ratio at 35% (for at least 80% of banks’ loan production).

- Nevertheless, mortgage interest rates remain very attractive at 1.35% in Q1 2022, supporting house prices going forward.

European banks sentiment survey : Loan demand & supply for house purchase (LHS, %) and mortgage interest rates (RHS, %)

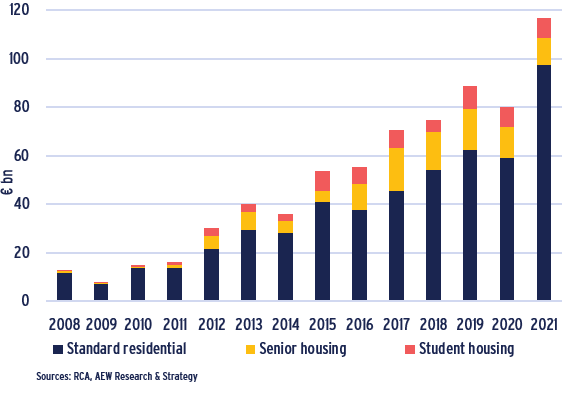

RECORD HIGH RESIDENTIAL VOLUMES IN EUROPE

- In 2021, the European residential sector reached an all-time high with €97bn invested. Residential now account for 35% of the total European investment market, an increase from 23% in 2020.

- At €27.6bn, the acquisition of Deutsche Wohnen by Vonovia was the largest deal in the European residential market. This exceptional transaction pushed the German transaction volume to a new record.

- With €52bn invested in 2021, Germany is the largest residential investment market, followed by the Nordics (€18bn) and the UK (€10.3bn).

- In France the residential sector is small in comparison to the size of the overall investment market at but institutional investors interest for residential asset is growing. 2022 volumes will be driven by the acquisition by French insurer CNP of 85% of the Lamartine fund (which is classified as article 9 under SFDR) from CDC Habitat for €2.4bn and representing 7,600 residential units.

Residential investment volumes (€ bn) by country and share of residential (%) in total investment volumes (%, RHS)

OPERATIONAL RESIDENTIAL: THE BENEFITS OF A COMMERCIAL LEASE

- Commercial residential – residential assets supported by a commercial lease to an operator – combine the benefits of a single, long, triple-net commercial lease with the defensiveness of the residential sector.

- On the back of an ageing population, investors’ interest in the senior housing market has been increasing. Since 2015, volumes invested in senior housing have more than doubled and reached €11.4bn in 2021.

- Volumes invested in student housing have also been increasing, driven initially by the UK market. The sector is now recovering from the pandemic which saw a drop in the number of international students studying in Europe.

- Investment activity appeared resilient with €8bn invested in the student housing sector in 2021. The joint venture between Unite and the Singapore sovereign wealth fund GIC reached £1.68bn after new acquisitions in London in 2021 and the partnership has been extended to 2032.

European investment residential volumes (€ bn) by subsector

ROBUST INCOME RETURNS CONFIRM BOND-LIKE STATUS

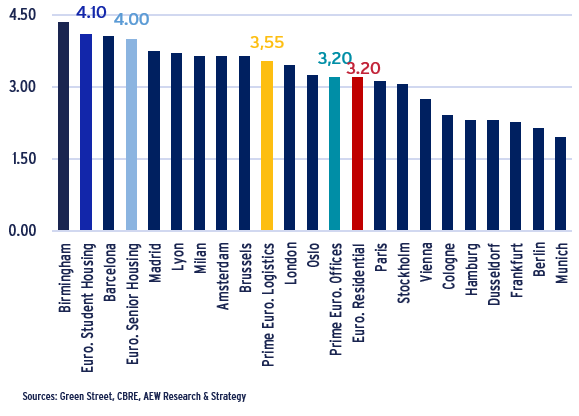

NET RESIDENTIAL YIELDS STAND AT 3.20%

- Net residential initial yields stand at 3.20% on average across our 24 markets as at Q4 2021, 10 bps lower than last quarter.

- Residential yields are net of operating expenses, which represents a leakage of around 25% which includes property management fees, basic repairs and maintenance, taxes and utilities.

- Net yields are the sharpest in markets which are highly regulated or with strong reversionary potential such as the German markets.

- Less regulated markets such as the UK and Spain benefit from more attractive yields.

- When comparing with prime offices (3.20%) and logistics (3.55%), European residential yields continue to appear attractive given the low associated risk.

Net residential initial yields (%) by market – Q4 2021

EXCESS SPREAD FOR RESIDENTIAL TO STAY ATTRACTIVE

- The yield forecasts are based on our stagflation scenario which combines a period of high inflation in the short-term and weaker GDP growth than expected before the start of the war in the Ukraine. This scenario might be adopted as our new base case and assumes a slowing down of the post-Covid economic recovery but stops short of assuming a recession.

- In this uncertain context, the ECB is expected to slow the normalisation of its monetary policy. Our forecasts for government bond yields based on the forward yield curve indicate that government bond yields are forecast to increase by 40 bps in 2022 and to increase by a further 20 bps by 2026.

- Net residential yields are therefore expected to increase by just 16 bps over the next five years on average for the 24 European markets covered.

- The yield spread between residential assets and government bonds is currently at 300 bps. This compares to an average of 170 bps over the past 15 years.

- In our base case stagflation scenario, the excess spread over bond yields is expected to remain high at 260 bps on average in 2022-2026. This is still well above the long term historical average.

Net residential & government bond yields (%) & risk premium (bps, RHS) - Europe

MODEST CAPITAL GROWTH EXPECTED GOING FORWARD

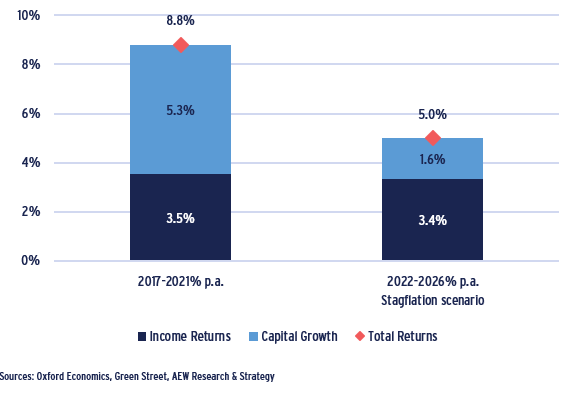

- Over the next five years, prime total returns for the residential sector are forecast to reach 5.0% p.a. on average in the 24 markets covered, in our stagflation scenario.

- Residential income returns are forecast at 3.4% p.a. in 2022-26 on average, which is close to the last five years’-average (2017-21).

- In contrast, capital growth is forecast at 1.6% p.a., down from 5.3% p.a. in the previous five years. The strong yield compression recorded in the past five years is indeed unlikely to continue in the next five years.

- Nevertheless, with interest rates expected to remain low for some time in our base case stagflation scenario, residential yields are expected to increase very modestly over the next five years.

Prime European residential total returns (%, p.a.)

PARIS RESIDENTIAL MARKET SURVIVED THE PANDEMIC

INNER PARIS PRICES MORE RESILIENT THAN EXPECTED

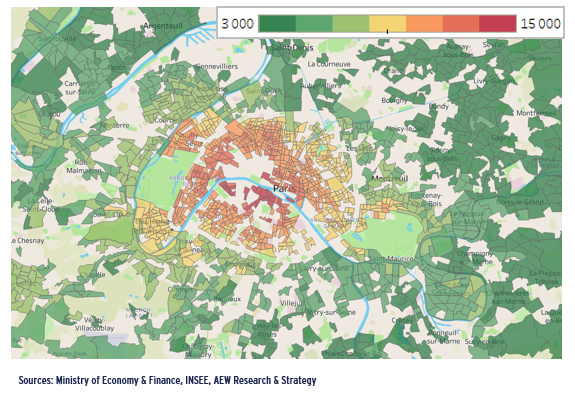

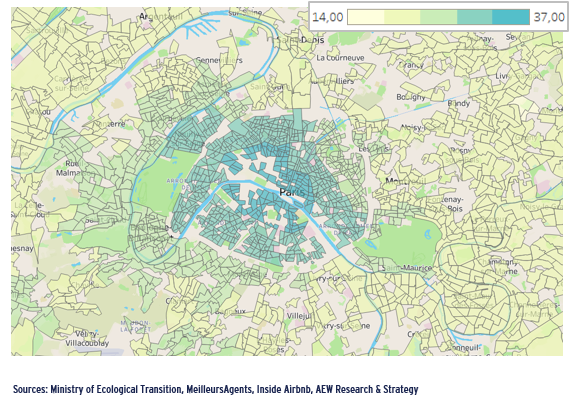

- This heat map on residential prices is based on 334,100 individual apartment transaction data recorded between 2019 and H1 2021. An average residential price per sqm is calculated for 1,660 local areas of the Paris region.

- In the Paris region, apartment prices increased by 0.7% year-on-year in Q4 2021. But while in Inner Paris, apartment prices decreased by 1.5%, in the Inner Rim, the first ring of suburbs, apartment prices increased by 2.2% and in the Outer Rim (the second ring of suburbs) apartment prices increased by 3.8%.

- While this polarisation can be attributed to the Covid pandemic, the impact on apartment prices in central Paris has been much more limited than initially expected despite high prices in Inner Paris.

Average prices in 1,660 local areas of the Paris region based on 334,100 transactions recorded in 2019-H1 2021 - €/sqm

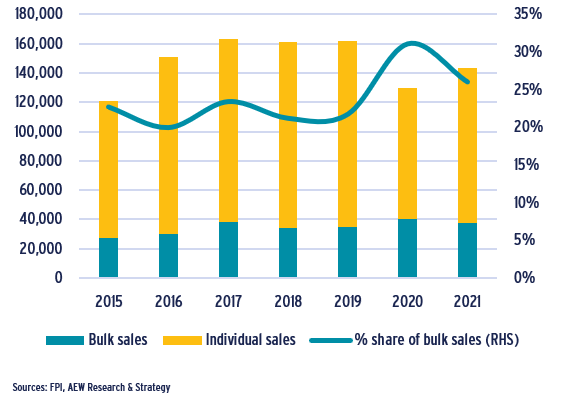

INSTITUTIONAL MARKET SHARE MAY INCREASE

- Developers sell new residential units to institutional investors, typically in “bulk”, or sell unit by unit to owner-occupiers or private investors.

- In France, bulk sales represented 26% of total sales of residential units in 2021, slightly higher than the pre-Covid average which has been stable over time at 22%. Bulk sales peaked in 2020 at 31% of total sales as a result of the lockdown which made sales to private investors more difficult.

- The increasing appetite of institutional investors make the competition harder for potential buyers of residential buildings. As a result, the discount between bulk sales and individual sales has been shrinking.

- Nevertheless, developers willing to de-risk their balance sheet are likely to favour quicker bulk sales over individual sales.

New-build dwellings sold by developers in France– bulk sales vs individual sales

RENTAL GROWTH MORE THAN DOUBLED IN 2021 IN PARIS

- Prime residential rents in Paris currently stand at €29.20/sqm/month as at Q4 2021. In 2020, prime residential rental growth slowed to 1.3% as a result of the Covid lockdown, but increased by more than 3% in 2021 when employees and students returned to the city.

- Local market rental levels range from €14/sqm/month to a maximum of €37/sqm/month in some areas of central Paris.

- Rental growth has been concentrated in the inner ring of suburbs with good or improving public transport accessibility, more than in Inner Paris where a rental cap has been reintroduced since July 2019. A similar rental cap also applies to a few other municipalities in northern Paris.

- Paris is one of the largest markets for Airbnb globally. Following the introduction by the Paris municipality of a compulsory registration of all short-term rentals, the number of short-term rentals listed on the platform has decreased by around 20% in July 2021, representing around 11,500 entire flats. The Covid impact was however very limited before this regulation was introduced. This has eased some of the pressure on the rental market but the market remains very tight.

Average residential rents in the Paris region including service charge

€/sqm/month for a typical 49-sqm apartment or 92 sqm house

This material is intended for information purposes only and does not constitute investment advice or a recommendation. The information and opinions contained in the material have been compiled or arrived at based upon information obtained from sources believed to be reliable, but we do not guarantee its accuracy, completeness or fairness. Opinions expressed reflect prevailing market conditions and are subject to change. Neither this material, nor any of its contents, may be used for any purpose without the consent and knowledge of AEW.