EUROPEAN LOGISTICS REACHING A TURNING POINT

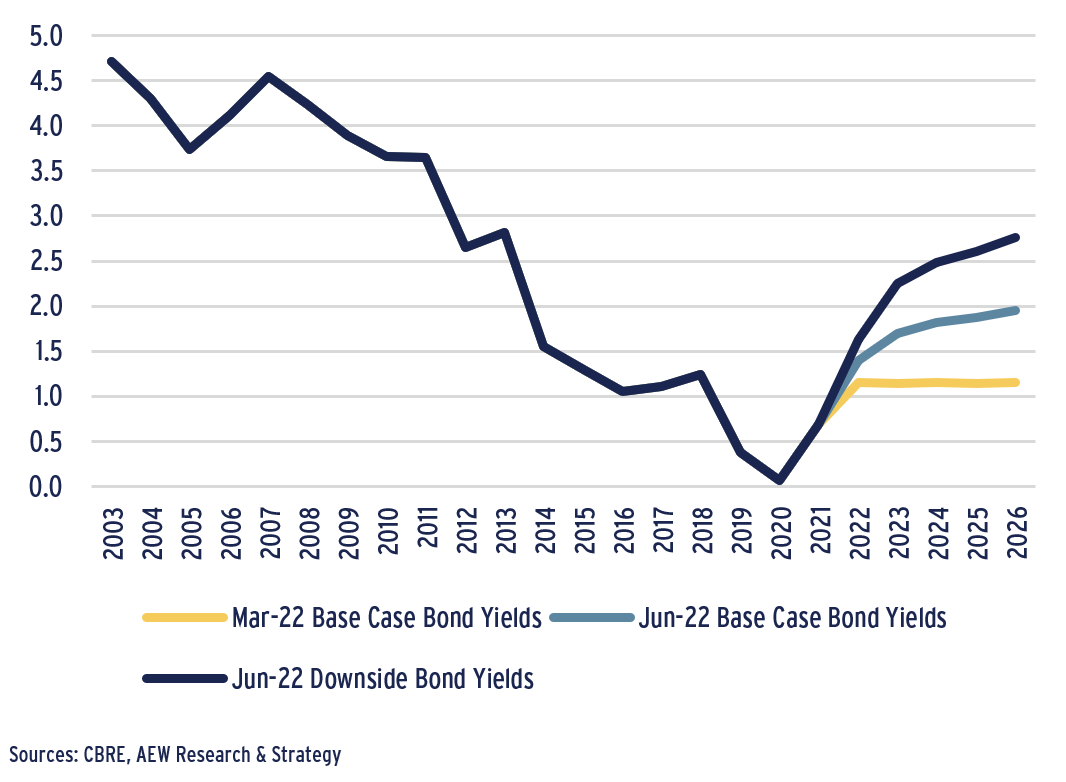

- The ECB has signaled a 25-50 bps rate hike in July and September as on the back of the on-going Ukraine conflict, inflation has continued to move up. Depending on the country, European government bonds have spiked by 100-200 bps over the last three months. These higher bond yields will impact on logistics markets as measured by our new Jun-22 base case and downside scenarios.

- Despite unchanged GDP forecasts, manufacturing and shipping activity across Europe is expected to pick up in the next ten years based on the increasing trend of re- and near-shoring. This will drive demand for logistics space going forward.

- Another key driver of logistics warehouse demand – the share of on-line retail sales – is projected to further increase to 40% in the UK and 25% in Continental Europe over the next ten years regardless of the recent Amazon news or economic outlook.

- As the pandemic exposed supply chain vulnerabilities, many logistics operators have moved from just-in-time to increase their capacity to absorb disruptions, which we can define as just-in-case. This has allowed take-up levels to set new records in 2021.

- High inflation and specifically concrete construction product costs will negatively impact on the profit margin of developers and could trigger a decline or delay in new supply in marginal markets where tenants can not absorb higher rents.

- New development has accelerated to meet the demand. But, future supply might come down as construction costs and site shortages increase. Vacancy rates are expected to stay at a record low 3% level, as demand and supply remain balanced.

- Given the largely unchanged GDP forecasts across Europe between Mar-22 and Jun-22, we keep our forecasts for logistics rents unchanged at an average of 2.3% pa over the next five years.

- As investment activity has also set new record levels and yields have been driven down with strong bidding, we are now expecting a turning point in yield movement. Investors will require higher yields going forward with elevated bond yields.

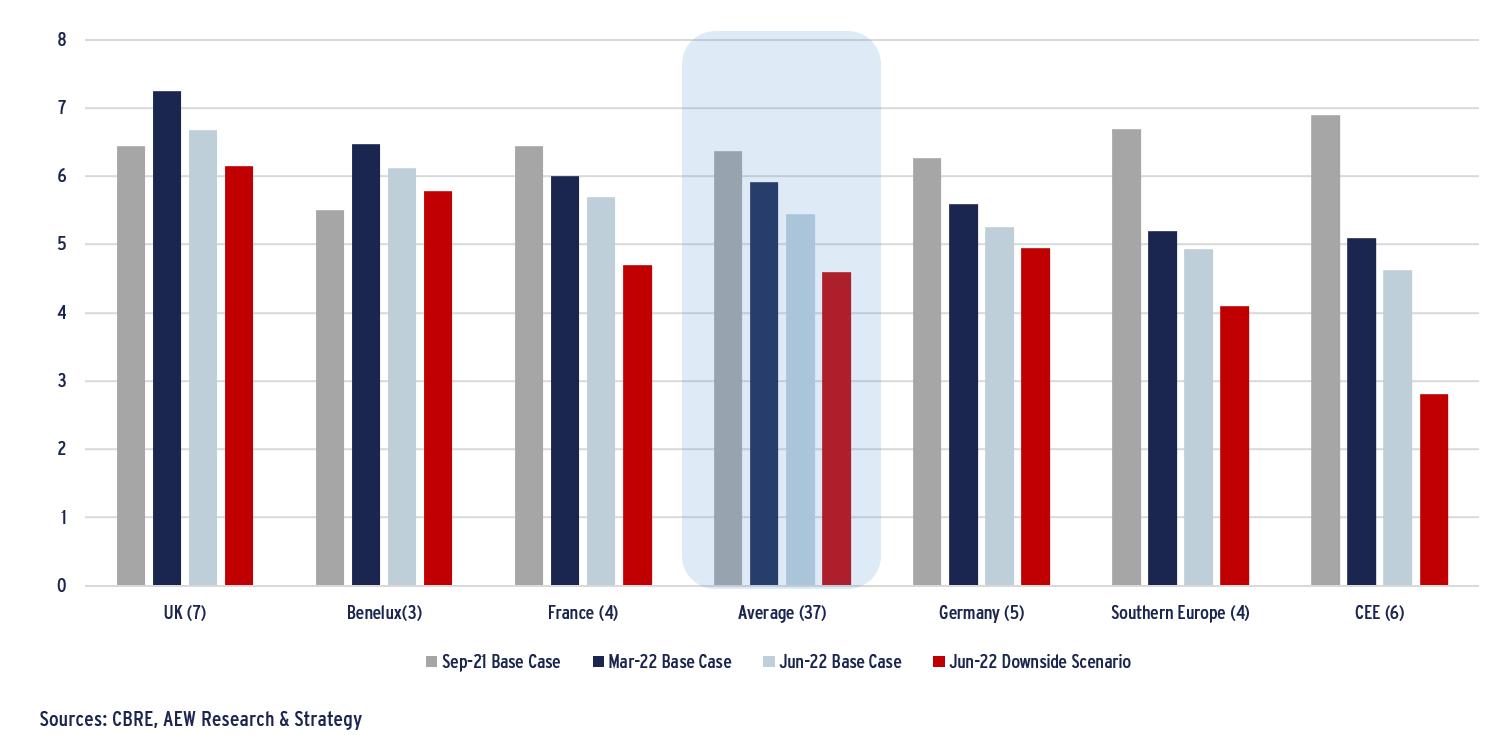

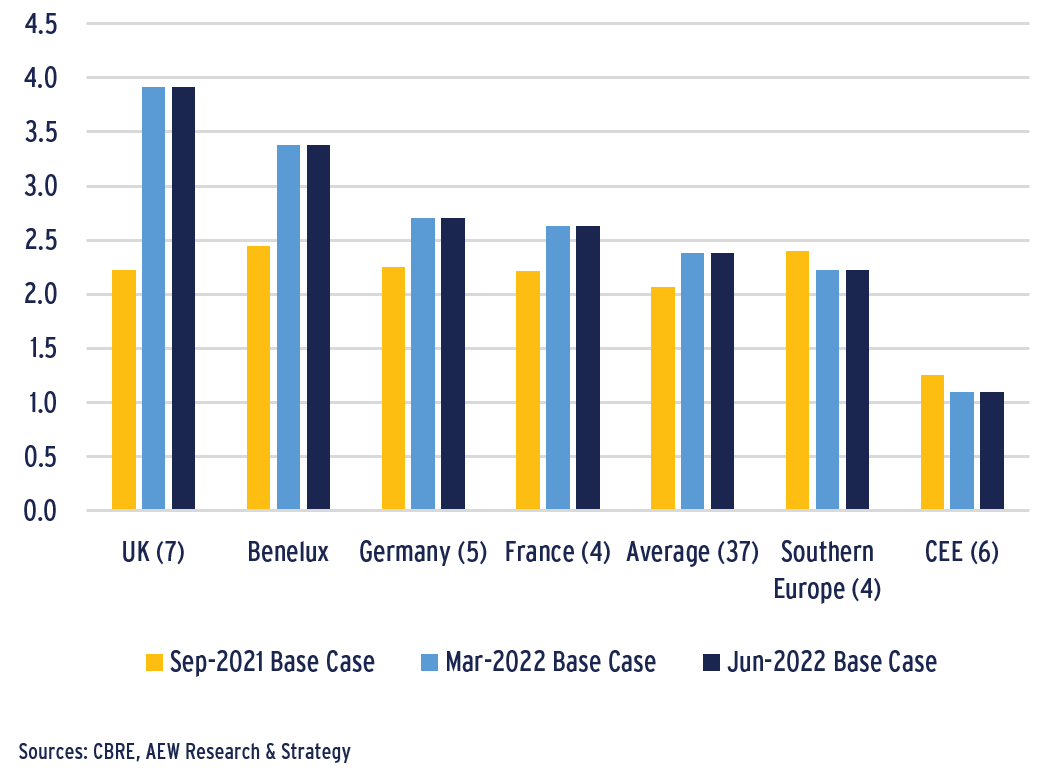

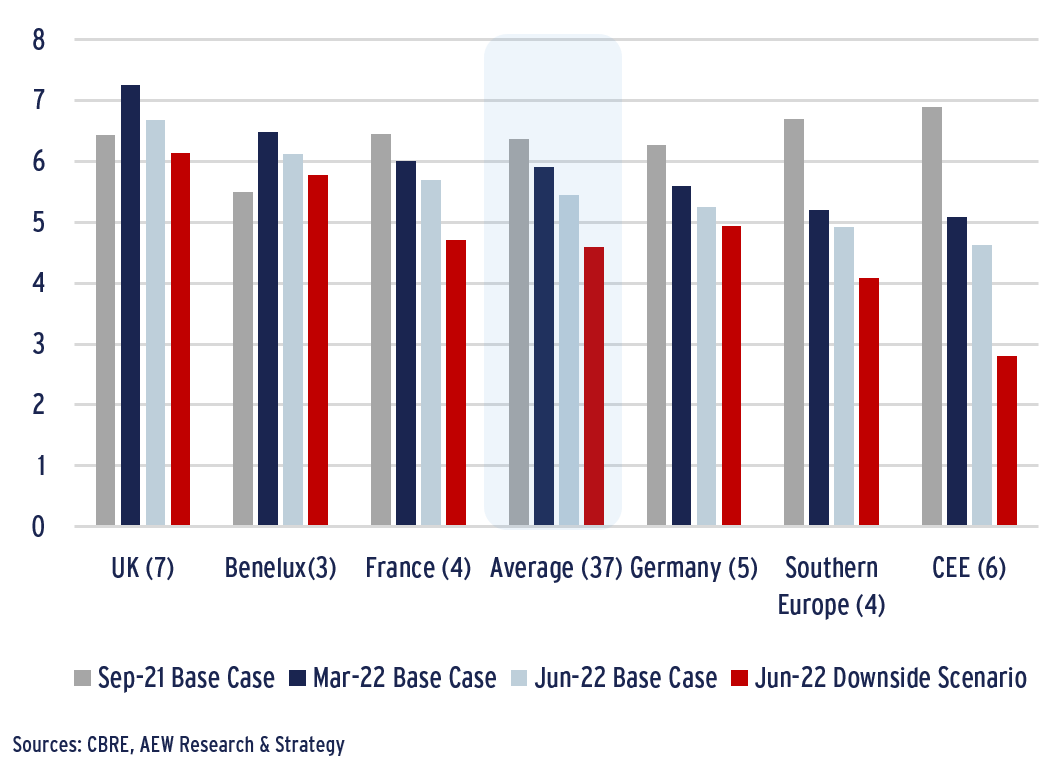

- Total returns for logistics markets across Europe are now estimated at 5.1% pa for the next five years in our Jun-22 base case, down 40 bps from our Mar-22 base case. Based on our Jun-22 downside scenario, total returns are projected at 4.1% pa.

- In our Jun-22 downside scenario, capital growth is projected to turn negative for most non-core CEE and Southern European markets. But, core markets like the UK, Netherlands, Germany and France are projected to maintain positive capital growth.

Logistics Average Annual Prime Total Returns by Country (2022-26 pa, %) – Various Scenarios

MACROECONOMIC FUNDAMENTALS

BOND YIELDS SPIKE AS RATE HIKES BITE

- On the back of the on-going Ukraine conflict, inflation has continued to move up. This has forced the ECB to signal a 25-50 bps hike in July.

- European government bonds have spiked by 100-200 bps over the last three months on the back of rate expectations and actual hikes from the Fed and Bank of England.

- Apart from the impact on investors, rate hikes could further impact consumer sentiment as increasing cost of living has already been hurting them.

- To catch up with this higher than expected actual bond yield widening, we have created an interim Jun-22 downside scenario to assess the impact on logistics.

- In our Jun-22 downside scenario, we project government bond yields across Europe to move up to 2.8% by year-end 2026. Also, we adopt our Mar-22 downside scenario as our Jun-22 base case.

10-year European Government Bond Yields (% pa, Average Across 20 Countries)

MANUFACTURING & SHIPPING TO REGAIN MOMENTUM

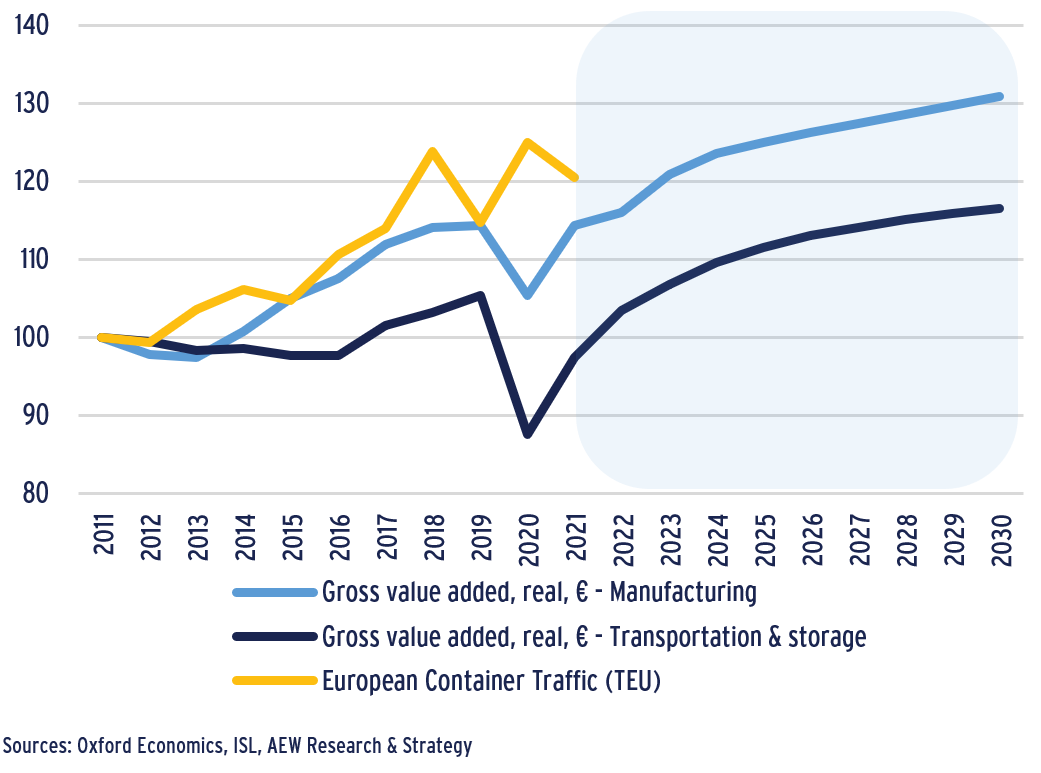

- Long-term macro fundamentals remain marginally positive. However, based on the increasing trend of re- and near-shoring, manufacturing and shipping activity is expected to pick up in the in the next ten years.

- While over the last 10 years there was negative or low growth of GVA in transportation and storage across Europe, the sector is expected to regain momentum in the next 10 years with solid growth.

- Urban densification remains the main driver for the growth of the sector as distribution centres and last mile logistics will continue to develop around major cities.

- Altogether, GVA in manufacturing is also expected to post double-digit growth during the same period, in particular in manufacturing-driven cities, also pushing demand for warehouses next to nearshoring activities.

- The European container traffic, which had already started to slow down on the back of the US-China trade war, slumped in early 2020, delaying the supply of construction materials and pushing prices to soar. Once supply chains have reorganised, we expected trade to catch up with long-term growth.

Container Traffic, Eurozone Gross Value Add in Transportation and Storage, Manufacturing (base 2011 = 100)

ECOMMERCE DRIVES DEMAND FOR LOGISTICS SPACE

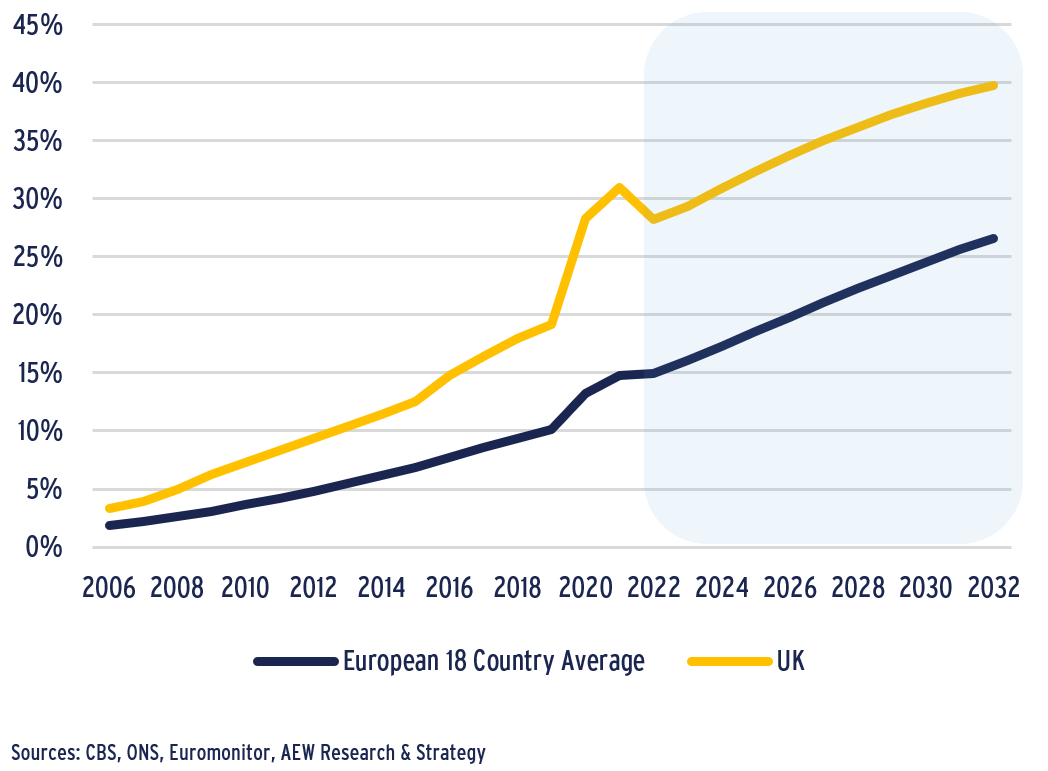

- The share of online sales is expected to double in the next ten years in Europe compared to pre-Covid levels.

- After a rolling series of lockdowns during the pandemic and the lack of open physical retail stores consumers stepped up their online shopping.

- Online-ordered groceries, which accounted for a smaller share of sales compared to non-food products are expected to drive future growth.

- The share of online sales was particularly boosted in the UK, reaching 30% on total sales in 2021 and is projected to reach 40% in the coming decade.

- In the rest of Europe, e-commerce represents a lower share of retail sales and lockdowns impacted sales differently depending on markets but the share of online sales is also expected to increase with online sales reaching 25% of sales by 2032 on average in Europe.

- This trend will support a continued demand for logistics warehouse space in the coming years, regardless of the macro economic situation.

Share of Online Sales as % of Total Retail Sales

INDUSTRIAL DRIVERS

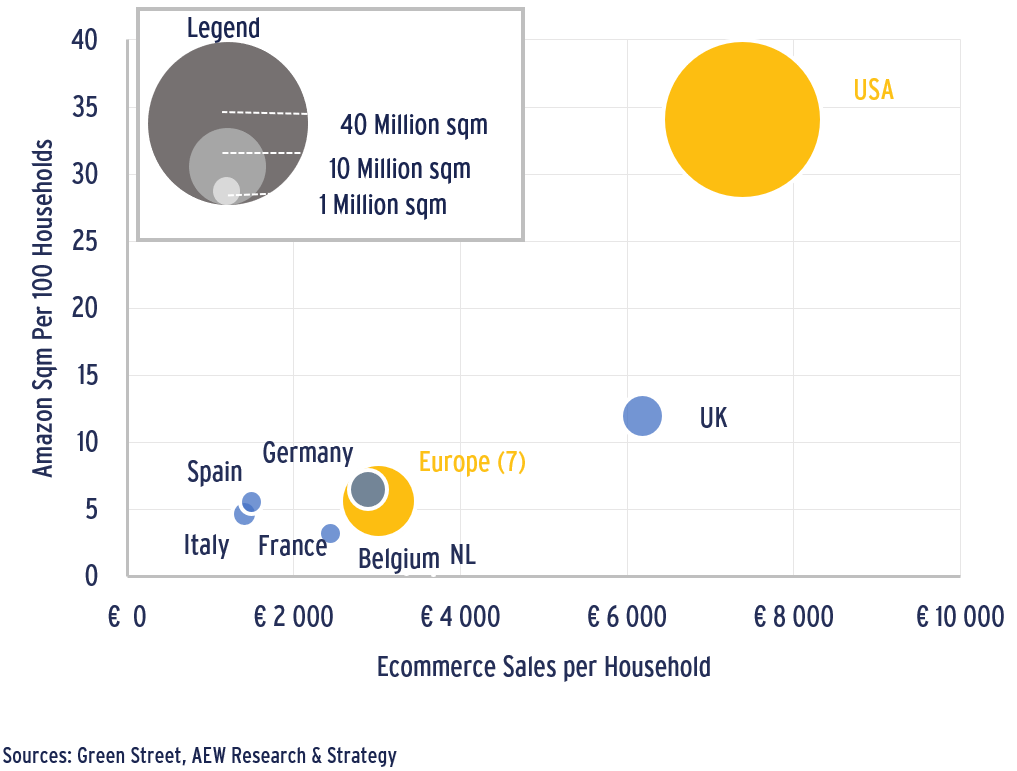

AMAZON PULLBACK HAS LIMITED IMPACT ON EUROPE

- Amazon has invested heavily in its logistics network, tripling it in the last five years in the US and doubling it in Europe, anticipating the growth in online sales share.

- In late April, Amazon had a profit warning stating that due to excess capacity it would be rolling back its expansion plans.

- However, detailed analyses by Green Street shows Amazon’s presence in continental Europe is less than one third the US level. While the giant retailer represents nearly 10% of total warehousing stock in the US and more than 7% in the UK, it makes up for a relatively lower proportion of 3% of the stock on continental Europe.

- As the chart shows both the European average as well as individual countries have lower e-commerce sales and Amazon space than the US.

- While Amazon pulls back, other large food and non food retailers have been increasing their purchase and lease of industrial space, continuing to feed demand for logistics space.

Amazon Country Presence vs E-commerce Sales (2022E)

STOCK MARKET’S OVERREACTION TO AMAZON NEWS

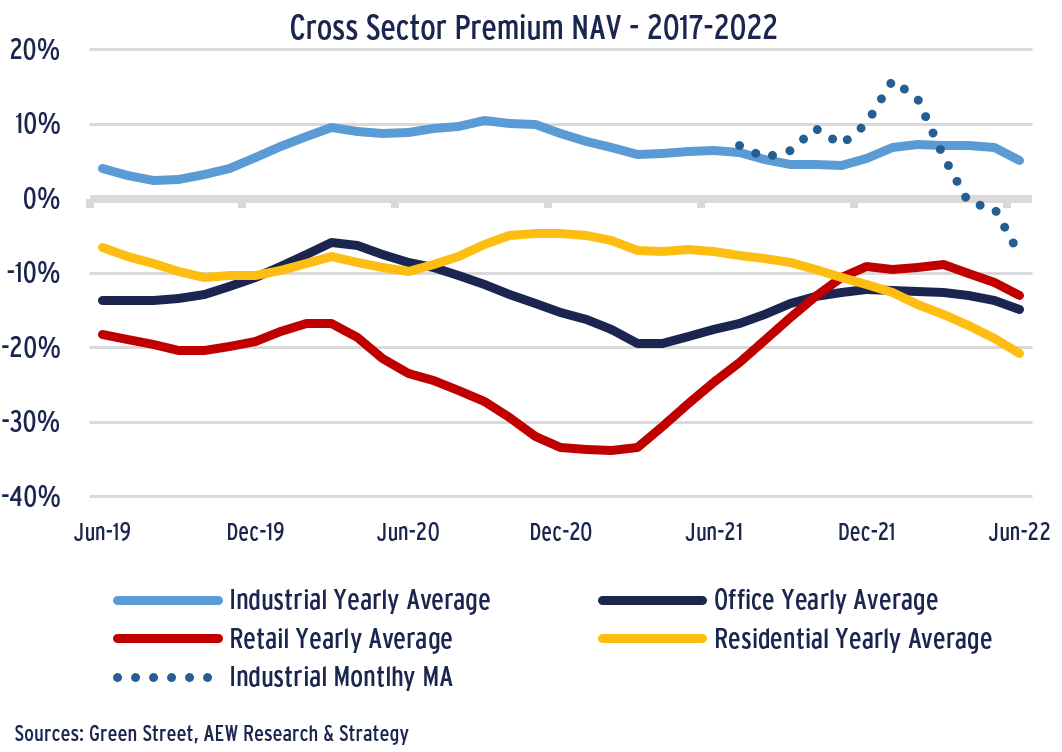

- Over the last three years, industrial REITs have been the favorite sector for investors as it consistently traded above Green Street’s NAV on a 12-month moving average.

- The Amazon profit warning in late April, combined with increasing construction costs and some news Amazon might be looking to sub-let space triggered a REIT share sell-off at discounts to NAV as can be seen on the monthly moving average.

- It seems very likely that REIT investors have over-reacted on the news since the fundamental drivers for logistics remain strong.

- In the medium term, we expect REIT investors to recognize the relative strength of logistics again and trade the sector nearer to the traditional premium.

Premium on NAV

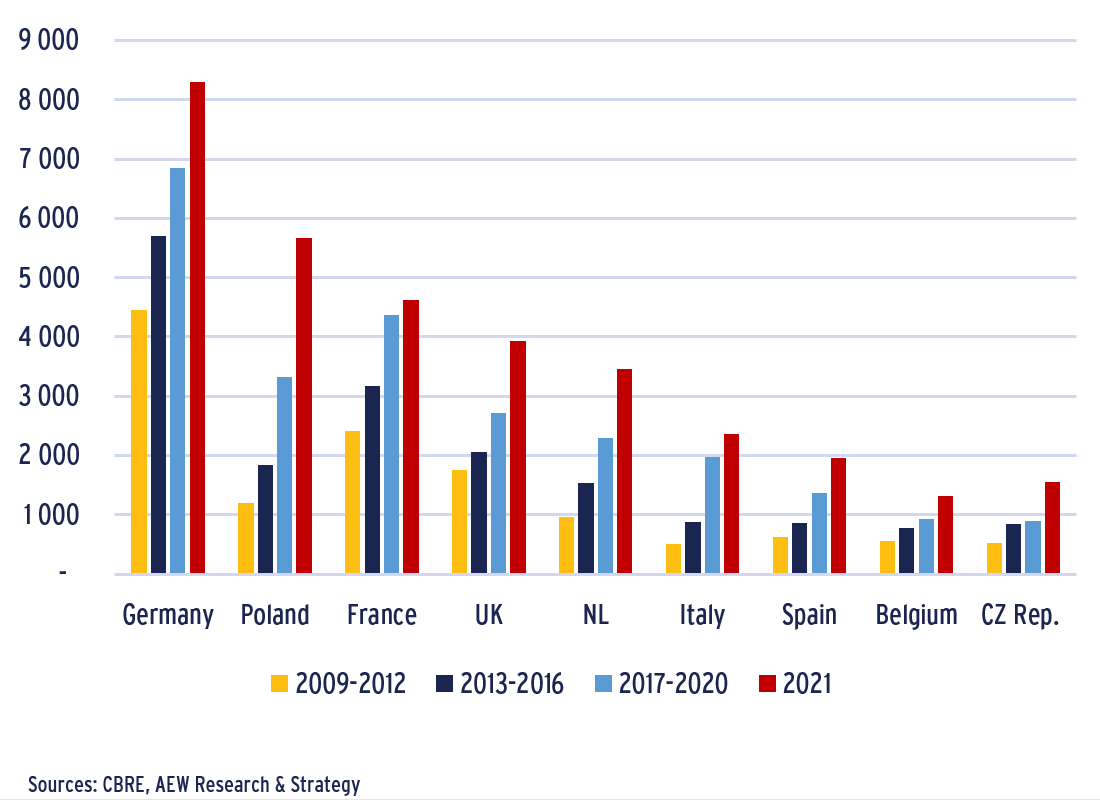

LOGISTICS TAKE-UP POSTS NEW RECORD IN 2021

- As the pandemic exposed the vulnerability of global supply chains and triggered longer delivery times, logistics operators have accelerated the reorganization of their supply chain processes.

- Many providers have moved from just-in-time to increase capacity to absorb future disruptions, which we can define as just-in-case.

- Logistics take-up reached another record in 2021 across Europe as warehousing expansion is viewed as efficient to avoid bottlenecks.

- New standards in terms of technical requirements, such as increase of ceiling height or demand for urban logistics also drove logistics take-up.

- Nearshoring benefitted Germany and Poland in particular, both manufacturing driven and centrally located for European distribution.

- The UK logistics market was driven by the online growth as UK-based e-commerce companies gained larger market shares.

Average Annual Logistics Take-Up by Period (‘000 sqm)

INDUSTRIAL OCCUPIER MARKET

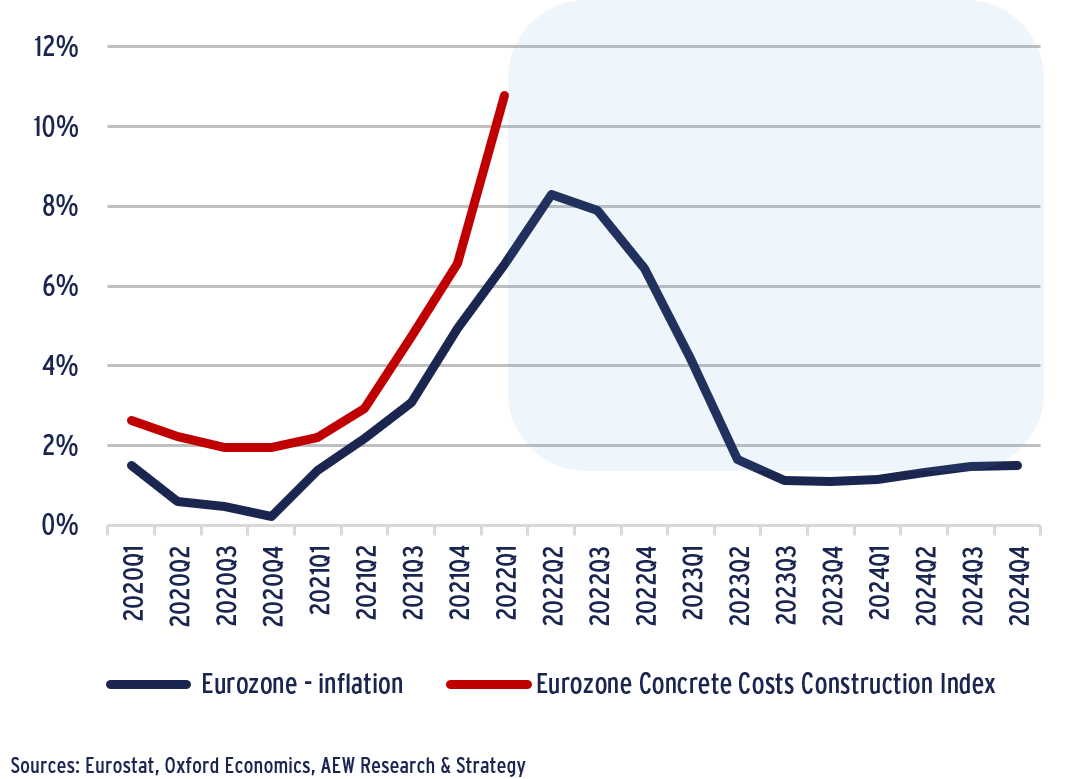

CONSTRUCTION COST INFLATION MIGHT LIMIT SUPPLY

- Global supply bottlenecks in China and the Russian embargo have pushed both general inflation and construction costs up.

- However, inflation is still expected to peak in the second half of 2022 before slowing down in 2023.

- Given this trend and the ongoing disruption in trade, construction costs are likely to continue to increase accordingly.

- The increase in concrete construction product costs has led inflation and will continue to negatively impact on the profit margin of developers.

- Concrete make up about 40-50% of a typical logistics warehouse.

- In markets where developers can not pass on these increased costs in the form of higher rents, we could see supply falling back.

- However, in markets where tenants can absorb them, rents might need to increase to allow developers to maintain their profit margins and deliver badly needed space to the market.

Inflation & Concrete Construction Product Costs (y-o-y; base Q1 2019 = 100)

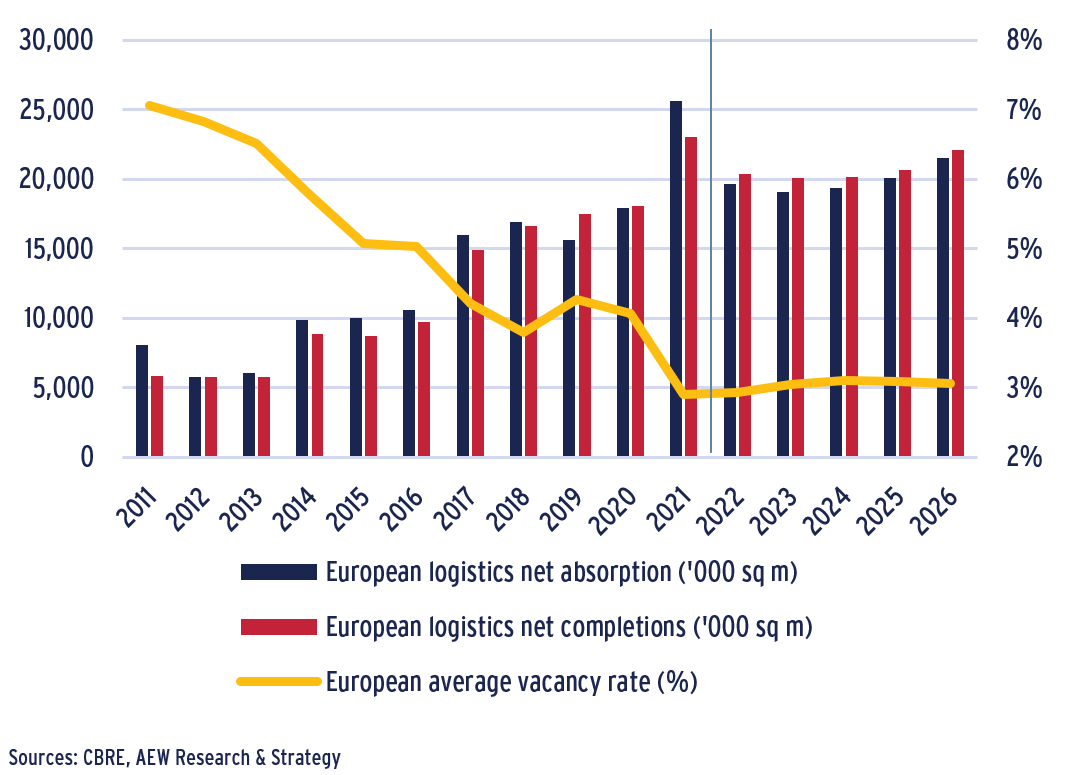

COMPLETIONS KEEP VACANCY NEAR RECORD LOW

- As demand for logistics space continued to increase, the development of new supply has accelerated over the last five years.

- Going forward, we expect a stabilization of both demand and supply at relatively balanced levels.

- There might be some downside to new supply. This is because apart from increasing construction costs, the shortage of land for industrial development is likely to increase as EU policy objectives aim at zero net land take by 2050.

- With green field sites becoming less available, existing stock eligible for conversion or brownfield sites are increasingly considered by developers.

- With established locations experiencing record low vacancy, well connected secondary locations benefit from spill over demand effects triggering an increase in future supply.

- Despite the acceleration of new supply, the average vacancy rate in Europe is expected to remain stable at a record low level of 3% as net absorption is expected to balance the limited level of future completions.

Vacancy rate, Net absorption and Net completions (‘000 SQM)

SOLID RENTAL GROWTH AS VACANCY RATE REMAINS LOW

- With record low unemployment and accumulated household savings, consensus is not yet expecting a recession in Europe.

- Given the largely unchanged GDP forecasts across Europe between Mar-22 and Jun-22, we keep our forecasts for logistics rents unchanged.

- This is supported by the strong underlying drivers of rebounding manufacturing and shipping and increasing e-commerce penetration.

- With new supply of space only exceeding net absorption by a small margin, we expect vacancy rates to stay near record lows.

- The stiff competition for land for industrial development is likely to worsen going forward, driving logistics rents up.

- High inflation and increasing interest rates might impact on GDP growth going forward.

- As the GDP growth expectations will change and might vary across Europe, we will revisit our rental growth projections in more detail in Sep-22.

Annual Prime Logistics Rental Growth for Base Case (2022-26, pa %)

INDUSTRIAL INVESTMENT MARKET

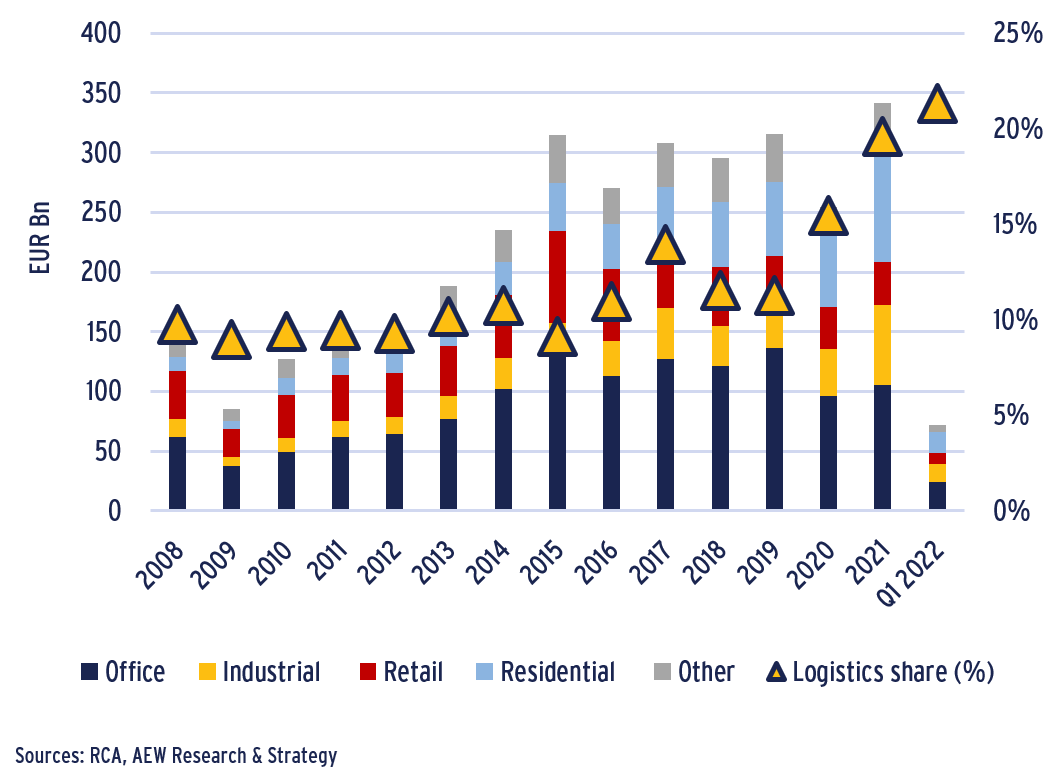

INDUSTRIAL SETS INVESTMENT VOLUME & YIELD RECORDS

- Industrial investment volumes over the last 12 months including Q1 2022 are double their pre-Covid average and Q1 2022 posted a new record high for any first quarter.

- As investors’ appetite has been growing for the sector, industrial forward acquisitions, including speculative schemes, are increasing, totaling EUR 7bn in 2021.

- This is nearly twice the amount recorded in 2018, and already at EUR 3bn for Q1 2022 alone. By contrast forward acquisitions in office reached only EUR 2bn in the same quarter.

- Other segments of the logistics investment market, such as last mile urban logistics, cold storage logistics and light industrial have also seen strong growth.

- With investors demand increasing, core logistics assets hit record low prime yields in Q1 2022.

European Investment Volumes (€ bn)

INVESTORS REQUIRE HIGHER FUTURE LOGISTICS YIELDS

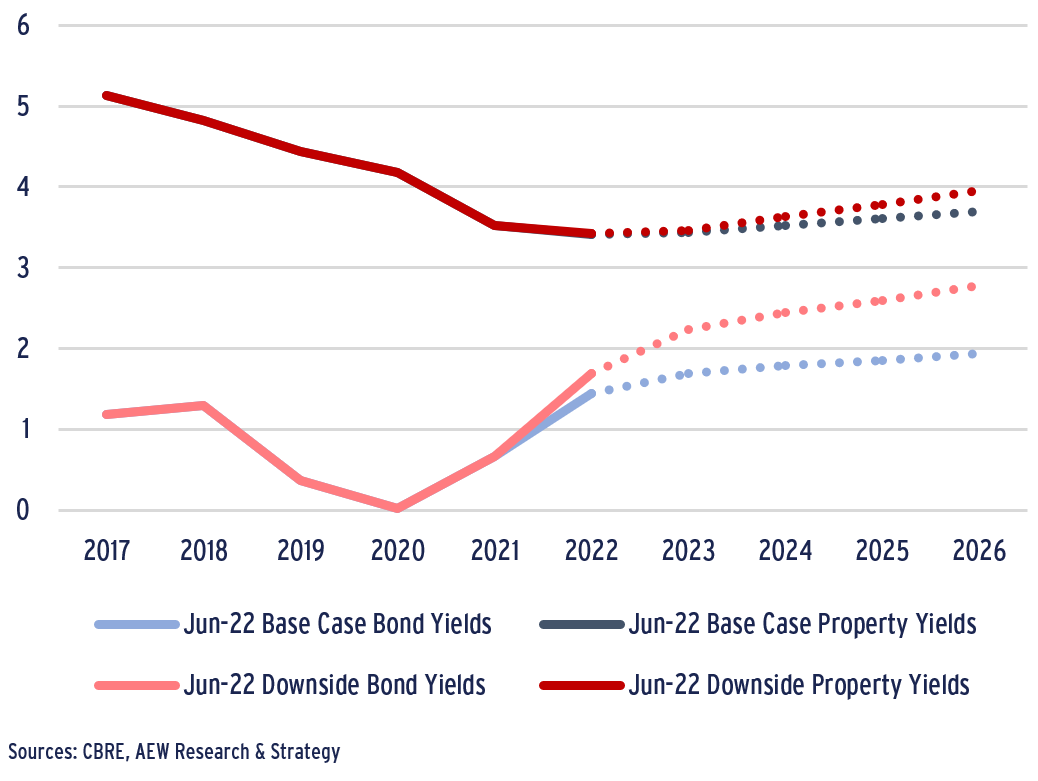

- Despite the strong momentum in both the occupier and investment markets over the last 5-10 years, we do expect prime logistics yields to widen from their current record lows. This would represent a turning point for the market.

- In our June 2022 base case, we expect a 20 bps widening over the next five years. This is in contrast with our downside scenario which shows a 50 bps widening.

- This is based on our assumption that investors will accept a floor to the excess spread of logistics yields over bond property yields of 25% of the 10-year historical average for each market.

- The precise timing of both bond and property yields widening might vary considerably by country. But inter-period movements have limited impact on our return projections over the five year period.

- This is not only based on the depth of the investment market, but also dependent on the occupier market and its exposure to global supply chains and the Ukraine conflict.

European Prime Logistics Yields vs Governement Bond Yields (%)

RESILIENCE IN CORE LOGISTICS MARKETS IN DOWNSIDE

- Total returns for logistics markets across Europe are estimated at 5.1% pa for the next five years in our Jun-22 base case. This is down 40 bps from our Mar-22 base case.

- Based on our Jun-22 downside scenario, total returns are projected at 4.1% pa as capital growth will turn negative for most non-core markets. This is due to the higher yields and their impact on capital growth over the five year forecast period.

- Core markets such as the Netherlands, Germany and France are projected to maintain positive capital growth, even in our Jun-22 downside scenario.

Logistics Annual Prime Total Returns by Country (2022-26 %)

This material is intended for information purposes only and does not constitute investment advice or a recommendation. The information and opinions contained in the material have been compiled or arrived at based upon information obtained from sources believed to be reliable, but we do not guarantee its accuracy, completeness or fairness. Opinions expressed reflect prevailing market conditions and are subject to change. Neither this material, nor any of its contents, may be used for any purpose without the consent and knowledge of AEW.