State of the U.S. Seniors Housing Market

The health crisis significantly affected the seniors housing sector, causing a disruption in its expansion in demand following a period of elevated new supply that culminated in a ~900 basis point swing in occupancies. At the same time, operating expenses came under pressure as enhanced protocols and a more challenging labor environment squeezed operating margins. The roll-out of a vaccine in the second half of 2021, however, represented an inflection point in the health crisis that has materialized into a durable demand recovery for the sector along with the broader economy. While near-term imbalances remain, we believe the expanding need for seniors’ care in a seniors housing setting will persist relative to other alternatives. Overall, AEW’s perspective on the long-term dynamics driving the sector remain unchanged with the aging demographic profile contributing to a further elevation in seniors related demand for housing over the next decade.

Several dynamics have aligned that we believe present an attractive investment inflection point for a sector with protracted tailwinds.

These include:

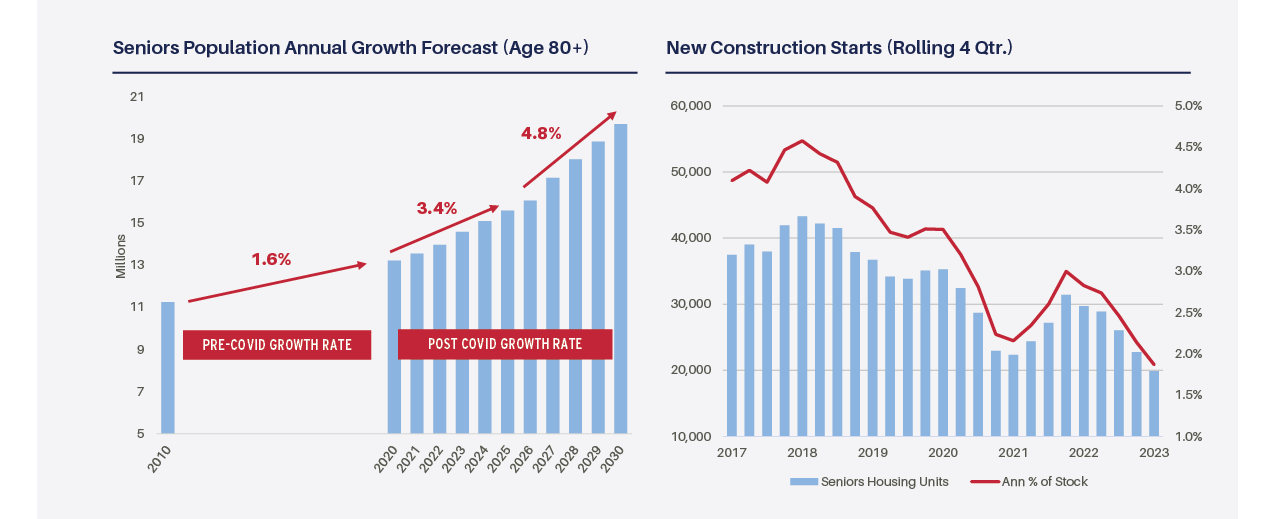

1. Constrained Supply as Demand Accelerates

The pace of new projects breaking ground continues to slow, falling below 2% of total inventory in Q1 2023 as the pipeline of projects under construction unwinds. Significant governors on new construction are currently in place including limited available financing at high rates, wide spreads and a return-on-cost that does not make sense relative to buying existing assets.

The industry has recorded eight consecutive quarters of positive net absorption representing annual demand growth of more than 5% in Q1 20231. In contrast, annual demand averaged 2.5% pre-pandemic2. While pent-up demand likely played a role early in the recovery, persistent growth above pre-pandemic levels has been the new norm likely anchored by demographic trends.

Source: Bureau of Census Current Population Forecasts; NIC Map Data Service. There is no assurance that any prediction, projection or forecast will be realized.

1 Source: NIC Map Vision, LLC. Timeframe reflects Q12021 – Q1 2023

2 Source: NIC MAP Vision, LLC . Five-year annual average Q1 2015-Q1 2020

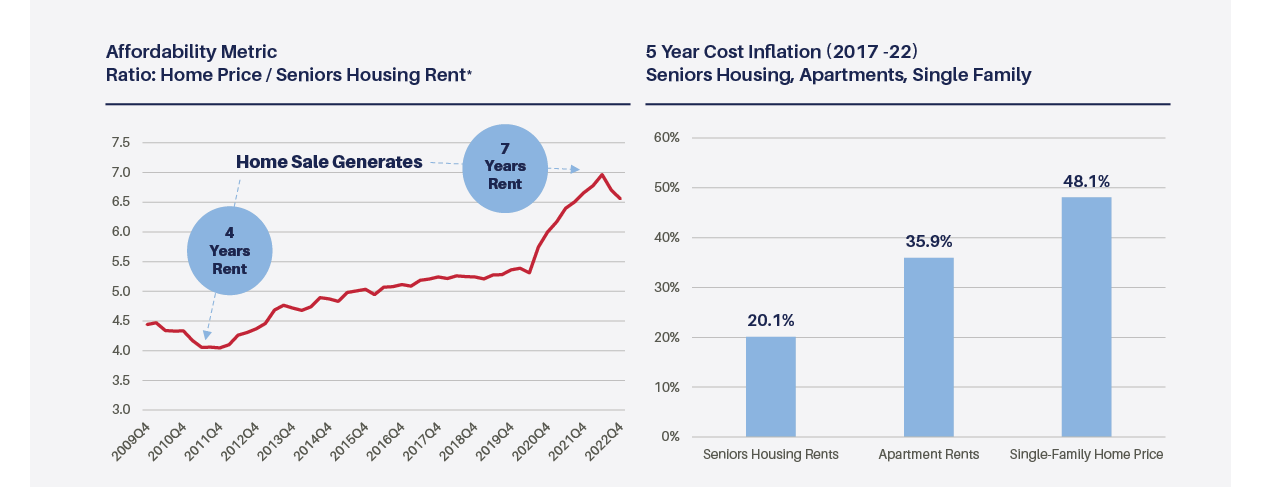

2. Positioned for Growth

The relative affordability of moving to seniors housing has increased, as the costs of seniors housing have fallen behind those of other housing alternatives:

- The average price of selling a home today covers approximately seven years of the average annual rent/care cost of seniors housing versus four years of rent/care payments in 20113.

- Senior housing rents grew 20.1% versus apartment rents which expanded 35.9% and single-family homes which appreciated 48.1% from 2017-20224.

The needs-based sector proved to be more resilient during the last economic recession (GFC) with top-line revenue growth out-performing relative to the other property sectors5.

3 Sources: NIC Map Data Service; National Association of Realtors; AEW Research

*Note: 79.1% of seniors age 75+ own their home - US Census Bureau American Housing Survey

*Note: data reflects the ratio of U.S. median single family home price to annual SH rent of NIC Primary Markets

4 Sources: NIC Map Data Service; Real Page; National Association of Realtors

5 Top line revenue growth defined as change in rent x occupancy calculated as a 4-quarter moving average.

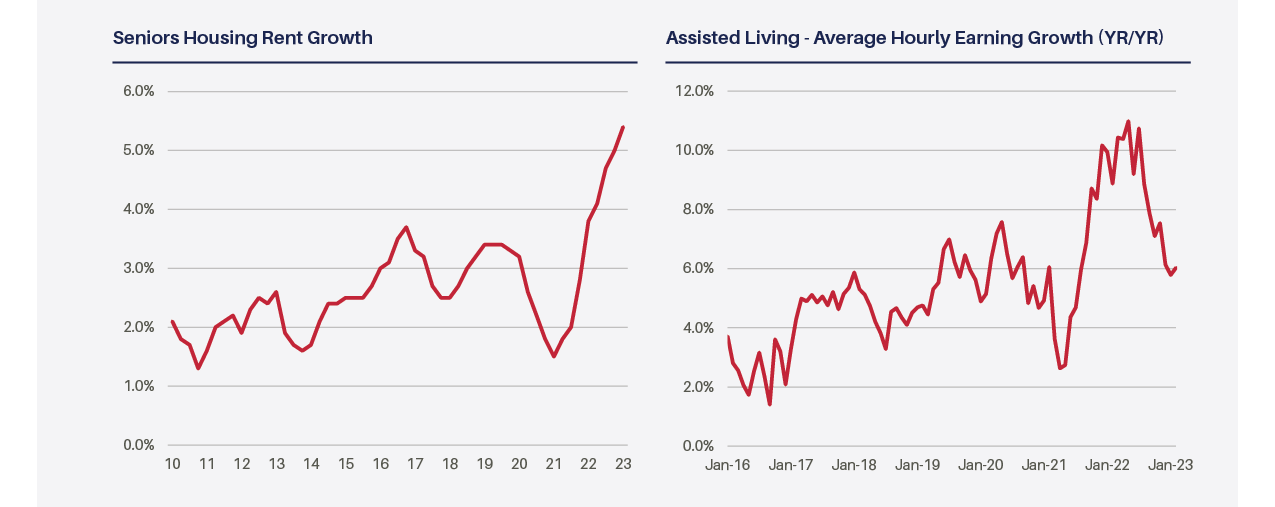

3. Improved Operating Visibility: Underwriting Growth Again

Annual rent growth has accelerated to a historical high of 5.4% in 2023 with seniors housing occupancy at 83.9% having recovered about two-thirds of the share lost relative to pre-pandemic levels6.

Labor availability has improved, and wage pressures have decelerated with assisted living employment levels eclipsing previous peaks. Agency usage as a share of labor expense has fallen by more than half over the past 12 months7.

6 NIC Map Data Service; primary and secondary markets as of Q1 2023.

7 Sources: Bureau of Labor Service, public company disclosures, AEW Research

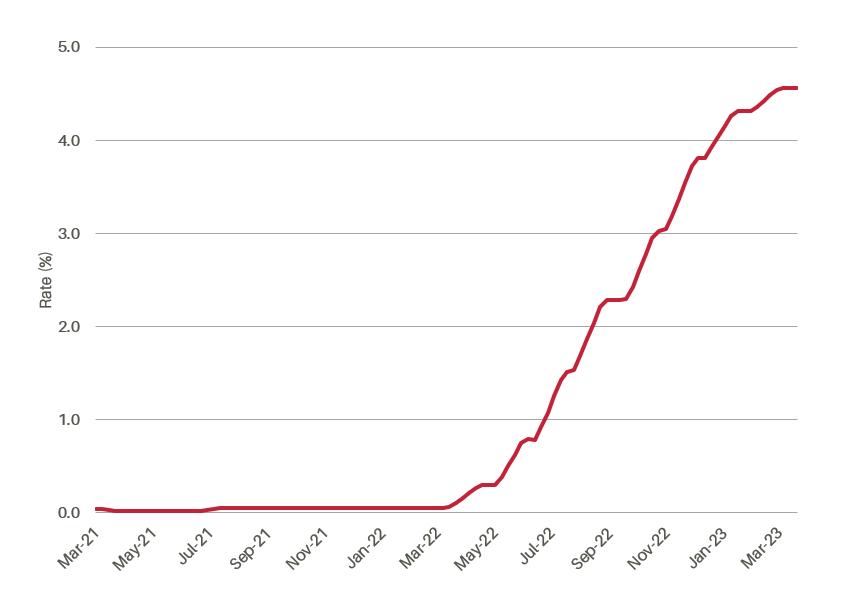

4. Continued Pressure on Owners with Misaligned Capital Structure

The rising cost and more limited availability of debt is presenting greater challenges for leveraged owners especially as liquidity wanes and lending standards tighten.

The FOMC held rates steady in June but maintained its hawkish stance on inflation which AEW believes will keep interest rates elevated over the near-term at a minimum.

A stalled transaction market presents a challenge for leveraged owners and fund managers with existing capital structures geared to a more liquid, lower interest rate environment.

Source: NIC Map Data Service; Primary and Secondary Markets, As of Q1 2023

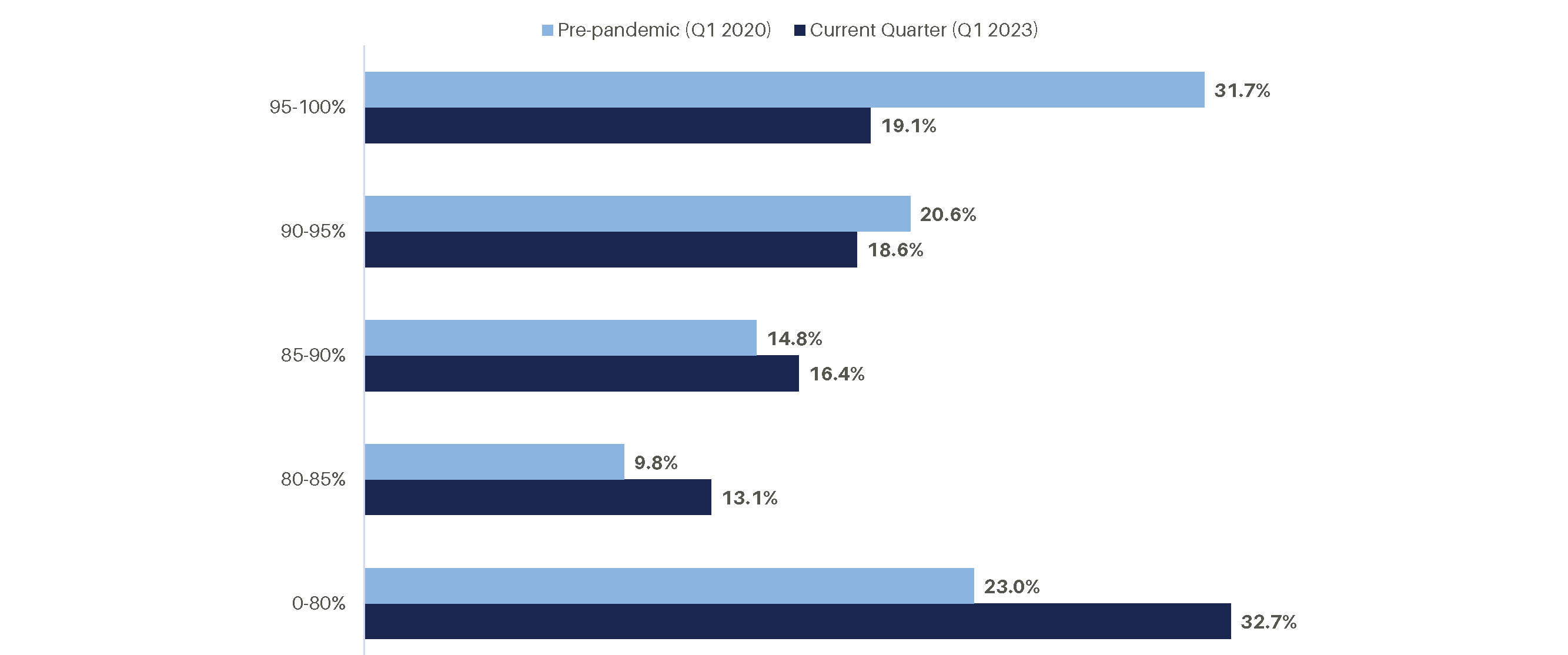

5. Need for Fresh Capital to Extend/Maintain Business Plans

The health crisis has extended the timeframe necessary to implement most pre-pandemic business plans. Operating norms have been reset to a higher expense structure.

The share of properties operating at or above stabilized occupancy levels of 90% remains well below pre-pandemic levels (38% vs 52%) suggesting more properties are operating with negative cash flow that require cash infusions from owners.

8 Source: NIC Map Vision, LLC; Primary Markets

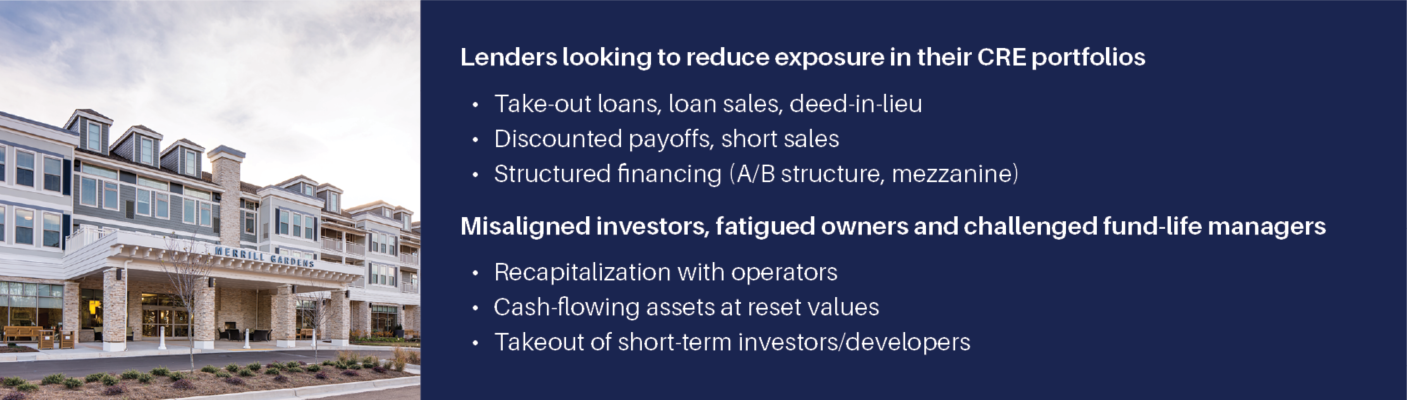

Identifying Opportunities

The current interest rate environment presents a ubiquitous challenge for commercial real estate given the leveraged nature of the asset class and seniors housing is no exception. Prior to the Great Financial Crisis (GFC), interest rates were following a similar tightening policy albeit not at the pace seen most recently. As the crisis unfolded, the Federal Reserve took an aggressive approach to lowering rates and implementing aggressive quantitative easing effectively setting the policy of keeping short-term rates near zero known as ZIRPs (Zero Interest Rate Policy). The ability to borrow at historically low rates for an extended period following the GFC essentially provided a mechanism (limited cost of capital) for lenders and borrowers to wait for a brighter future. Despite the elevated risk of recession facing the U.S. over the next 12+ months, AEW does not anticipate a similar scenario playing out this cycle. The Fed seems to be telepathing a similar sentiment through June 2023 based on the target range for its benchmark rate as expressed by the future expectations of individual policy makers on the FOMC. While certainly not a given, the ability and/or desire to implement a similar policy to the one put in place following the GFC appears more limited.

The implication is that access to capital will remain constrained and the cost of capital will remain elevated adding to the level of distress facing the sector which in turn creates opportunities for capital providers even as operating metrics improve. While AEW has seen the number of seniors housing opportunities increase, we are now observing an emergence of higher quality investment options.

The opportunity set of higher quality investments will likely be sourced from:

These opportunities will vary by region and market although the ultimate success of an asset remains tied to the quality of the operator, asset specific attributes, local competition and trade-area dynamics that determine market depth and the profile of resident demand. Larger markets that are expanding with an above average wealth profile and constraints to supply resulting in above average occupancies and rent growth will likely present better

repriced-core opportunities over the next several years. Representative markets include Boston, Seattle and select California markets. Growth oriented markets with more exposure to recent new supply resulting in lower occupancies albeit with sufficient size, wealth and depth in the adult-child demographic should produce more attractive value-added opportunities. Representative markets for these opportunities include Dallas, Colorado and select southeastern states.

Over the short-to mid-term horizon, AEW anticipates existing assets should provide a more attractive risk adjusted return than building given the relative return-on-cost to develop versus yields on existing assets and aversion construction financing. Secondary and tertiary markets where the potential for new supply has often been the most significant risk, may present additional opportunities as current conditions persist. Historically, AEW has been successful implementing smaller market strategies with the right operator.

Good Tradewinds, Great Tailwinds

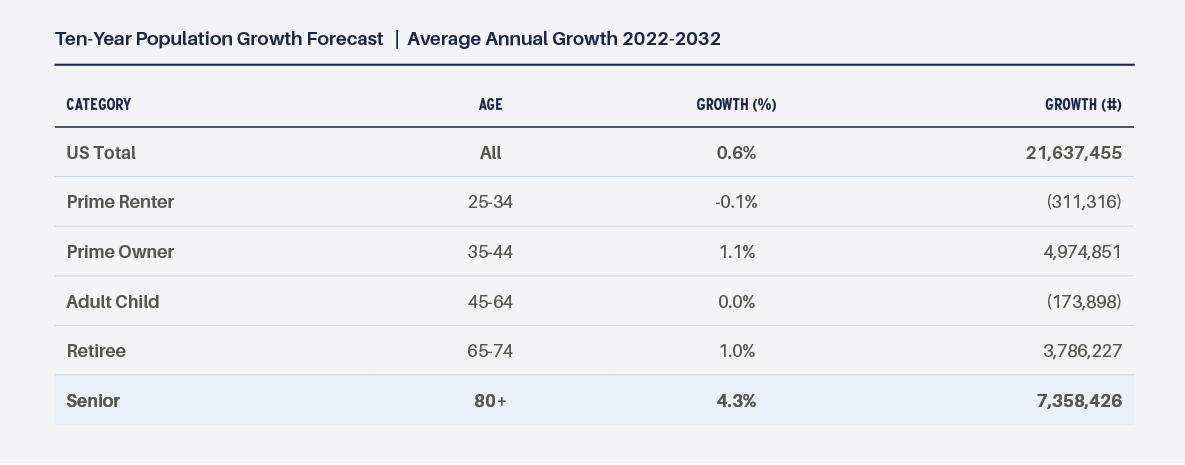

With the front edge of the baby boomers turning 77 in 2023, the much heralded “silver tsunami” is taking shape as a significant factor driving more robust demand for seniors housing. Over the next decade, the 80+ age cohort is expected to grow 4.3% annually adding over 7.3 million people representing more than one third of the nation’s total population growth. Taken alone, this dynamic is considered the primary demand tailwind for seniors housing. However, this driver takes on more depth when considering the broader demographic landscape that underpins both the need and ability for a senior to make a move to seniors housing.

- Seniors are the fastest growing age cohort in both percentage terms and absolute numbers and 79% own a home.

- The primary age group looking to own a home is the second fastest growing age cohort.

- Retirees, the prime renters for active adult/build-for-rent are a close third in terms of growth.

- The number of adult children, the prime caregiver cohort for seniors, is not increasing making seniors housing a logical alternative for seniors needing care.

Summary

As noted, there are multiple dynamics that have aligned to create what we believe will make seniors housing an attractive investment opportunity with protracted tailwinds. The fundamental underpinnings of constrained new supply with persistent and accelerating demand have the industry well-positioned for growth. With improved operating visibility into both top-line and bottom-line revenue growth, we believe we have reached a favorable inflection point in the investment cycle. The health crisis has put a wrench in many business plans creating the need for fresh capital and extending timeframes as the broader capital markets have become less accommodating and the cost of capital has increased. The Federal Reserve appears likely to maintain its hawkish approach to inflation keeping interest rates elevated for longer setting the stage for what we believe will be a higher degree of distress for investment real estate than the previous cycle. The current dynamics point to what may be forming one of the most appealing investment environments in seniors housing for committed long-term investors with deep operating relationships.

Prepared by AEW Research, August 2023

This material is intended for information purposes only and does not constitute investment advice or a recommendation. The information and opinions contained in the material have been compiled or arrived at based upon information obtained from sources believed to be reliable, but we do not guarantee its accuracy, completeness or fairness. Opinions expressed reflect prevailing market conditions and are subject to change. Neither this material, nor any of its contents, may be used for any purpose without the consent and knowledge of AEW. There is no assurance that any prediction, projection or forecast will be realized.