U.S Economic and Property Market Outlook

The Return of Return Capital Has a Cost (Again)

Throughout 2022, and over the past 90 days in particular, the Federal Reserve has aggressively moved to tighten financial market conditions across the U.S. economy. So far, this tightening has been achieved primarily through a rapid increase in the Fed’s overnight lending rate, moving from an effective rate of zero at the beginning of the year to more than 3% as of the end of October. More significantly, the Fed’s Open Market Committee (FOMC) has clearly indicated it intends to further increase short-term interest rates at future meetings until observed inflation and, more importantly, inflation expectations, revert towards levels more consistent with longer-term monetary policy goals (i.e., +/- 2%). Currently, FOMC forward guidance suggests short rates will peak next year somewhere between 4.5% and 5%.

FIGURE 1

FOMC FORWARD GUIDANCE FOR FED FUNDS BORROWING RATE

Source: Federal Reserve, as of September 2022

There is no assurance that any prediction, projection or forecast will be realized.

As the Federal Reserve has pulled forward the pace at which overnight interest rates will rise, the forward curve for the benchmark 10-year Treasury yield has also shifted, rising from March’s expected 2027 rate of 2.5% to nearly 4.5% today. This change in expected future interest rates has, in turn, filtered into a variety of borrowing costs across the economy. For example, the average 30-year single-family mortgage rate increased from less than 3% in mid-2021 to approximately 7% today, dramatically raising the cost of home purchases and, consequently, lowering the pace of home sales (new and existing) from a pre-COVID peak of 7.3 million to approximately 5.3 million today1.

FIGURE 2

10-YEAR TREASURY YIELD FORWARD CURVE

Source: Federal Reserve, as of October 31, 2022

There is no assurance that any prediction, projection or forecast will be realized.

As interest rate-sensitive sectors of the economy slow, the likelihood of broader economic contraction has increased. For example, the year-over-year change in the leading economic indicators, a reliable signal of past periods of recession, turned negative during the third quarter. Absent a significant change in monetary policy, we expect the U.S. economy to be in some form of recession during 2023. The depth and duration of an economic contraction next year will, of course, be shaped in large part by any additional financial condition tightening by the Federal Reserve over the remainder of this year and throughout 2023; tightening will itself be shaped largely by the degree to which inflation (and inflation expectations) moderate. Currently, we do not anticipate any significant change in Fed policy through at least the end of 2023 and likely well into 2024.

FIGURE 3

FEDERAL FUNDS RATE AND PRIOR RECESSIONS

Source: The Conference Board, NBER, as of September 2022

U.S. Commercial Property

As with the single-family housing market, the rapid tightening of financial conditions broadly, and the rise in borrowing costs specifically, has had an immediate impact on the liquidity of the U.S. commercial property market. Transaction volumes slowed significantly during the third quarter as bid-ask spreads widened and third-party financing became difficult, if not impossible, to source. While the first half of 2022 saw total transaction volumes well ahead of 2021 and 2019 (pre-COVID), it seems likely that 2022 will finish with levels comparable to 2019 if not lower, particularly in specific property sectors. Certainly, we do not expect there to be a repeat of the transaction surge in the fourth quarter of last year.

FIGURE 4

TOTAL COMMERCIAL PROPERTY TRANSACTION VOLUME BY YEAR

Source: NCREIF

While not yet reflected in reported data, there are signs that property investor sentiment and capital pacing is slowing and that the market has entered a new period of price discovery for this cycle. Anecdotally, most major money center banks have recently slowed or stopped new lending activity, largely in response to external capital reserve requirements or internal allocation issues. In some cases, lender capital pacing during the first half of 2022 has already exceeded all of 2021 and there is little business case pressure to continue. Indeed, this is affirmed by the first half aggregate property transaction volume data highlighted in Figures 4 and 5, with total volume during the first six months of this year well ahead of the pacing of 2021 and 2019 (pre-COVID). More significantly, when viewed on a trailing four quarter basis, U.S. total property transaction volume is nearing an all-time peak of $1 trillion, far in excess of prior peaks in 2007 and 2019.

FIGURE 4

TOTAL COMMERCIAL PROPERTY TRANSACTION VOLUME BY YEAR

Source: RCA, as of September 2022

Even in specific cases where lenders are offering financing, higher borrowing costs relative to current property income (NOI) yields are no longer accretive to current income yield. Figure 5 illustrates the average NCREIF Property Index (NPI) appraisal cap rate as well as that cap rate leveraged 50% with fixed-rate and floating-rate debt at the prevailing borrowing cost. As illustrated, leveraged property yields are now sharply lower than unleveraged yields rendering most financing impractical. There are, of course, times when investors will employ negatively accretive near-term leverage if they are able to underwrite higher eventual property NOI and/or falling future borrowing costs. Given today’s heightened uncertainty regarding future Fed rate increases as well growing uncertainty over the broader economic outlook, few investors today are willing to do so.

FIGURE 5

IMPACT OF LEVERAGE ON PROPERTY YIELDS (%)

Source: American Council of Life Insurers (ACLI), NCREIF, as of Q3 2022

The combination of lender pullback and higher borrowing costs is quickly eroding the availability and the yield accretion of financial leverage, effectively pushing highly leveraged investors to the transaction market sidelines. As shown in Figure 6, the cost of most fixed-rate borrowing is already well above the average NPI property yield (cap rate), which stood at 3.8% as of the second quarter, and most floating-rate leverage is quickly moving in the same direction.

Property Yields Expected To Rise

Over the past 25 years, the average spread between property cap rates and the 10-year Treasury yield has been approximately 250 basis points, ranging from a high of nearly 400 basis points in the periods right after the early 2000s Tech crash and the 2008-2009 Financial Crisis to a low of near zero during the run up to the Financial Crisis. Today, the average NPI appraisal cap rate is well below 4% and the 10-year Treasury yield hovers slightly above 4%. Clearly property yields will rise. This can happen through property income growing faster than valuation increases, property valuation declines, or some combination of both.

FIGURE 6

NPI AVERAGE CAP RATE SPREAD TO 10-YEAR TREASURY YIELD

Source: NCREIF, as of Q3 2022; 10-Year Treasury, as of October 28, 2022

Potential Valuation Impacts Resulting from Higher Yield Environment

Potential future property valuation changes will likely reflect both changes in underlying cap rates as well as expected growth in the property income that is being capitalized. Tables 1 and 2 below provide a framework for thinking about these changes in the context of the NPI. As of 2022 Q3, the average appraisal cap rate, defined as net operating income (NOI) divided by current value, was approximately 3.7%, ranging from slightly less than 3% for the average industrial property to nearly 5% for the average retail property.

Table 1 illustrates the impact of different increases to the cap rate given different expectations for future NOI growth assuming a starting average cap rate of 4%, slightly above where the NPI stands today. Similarly, Table 2 illustrates a hypothetical 100-basis-point increase in cap rate given different cap rate starting points as well as expectations of future NOI growth. In both cases, these tables are simple “one period” solutions where both cap rates and NOI change over the same future period (e.g., one year, two years, etc.).

TABLE 1

VALUE IMPACT WHEN STARTING AT 4% AVERAGE APPRAISAL CAP RATE

Source: AEW Research, as of Q3 2022

TABLE 2

VALUE IMPACT OF 100-BASIS-POINT INCREASE IN CAP RATE

Source: AEW Research, as of Q3 2022

Currently, there is significant variation across property sectors in terms of current average appraisal cap rate and trailing four-quarter growth in NOI (see Figure 7). Property sectors with stronger recent NOI growth such as industrial and apartment generally have much lower valuation cap rates while weaker growth property sectors such as office and retail generally have higher current valuation cap rates.

FIGURE 7

CURRENT AVERAGE NPI APPRAISAL CAP RATE AND TRAILING FOUR-QUARTER NOI GROWTH

Source: NCREIF, as of Q3 2022

Conclusion

The remainder of 2022 and 2023 will be a period of great uncertainty regarding the economy and the true cost of capital. The catalyst of unacceptably high inflation has forced the Federal Reserve and other central banks to end the prolonged period of near-zero interest rates and massive monetization of government debt through central bank balance sheets (quantitative easing) that has characterized the post-Financial Crisis period. In the long run, we believe the return to an environment where safe assets have yield will prove ultimately beneficial to investors everywhere as capital markets work best to allocate scarce resources when there is a known and defensible cost to their capital. The entire investment industry can further benefit from greater information efficiency and there will likely be a significant widening in investor outcome between less skilled and greater skilled investors. In the short-term, however, the price of risk assets must adjust to the new reality. In most cases, publicly traded risk assets have already re-priced or are largely through the process. Also in most cases, private market risk assets, including commercial property, have largely not re-priced yet and this process will likely play out through the remainder of 2022 and throughout 2023. We believe, the timing and degree of this re-pricing will be shaped, as always, by additional future changes to monetary policy, the resulting impact to the broader economic environment, and the property sector/market specific vagaries of the various individual assets.

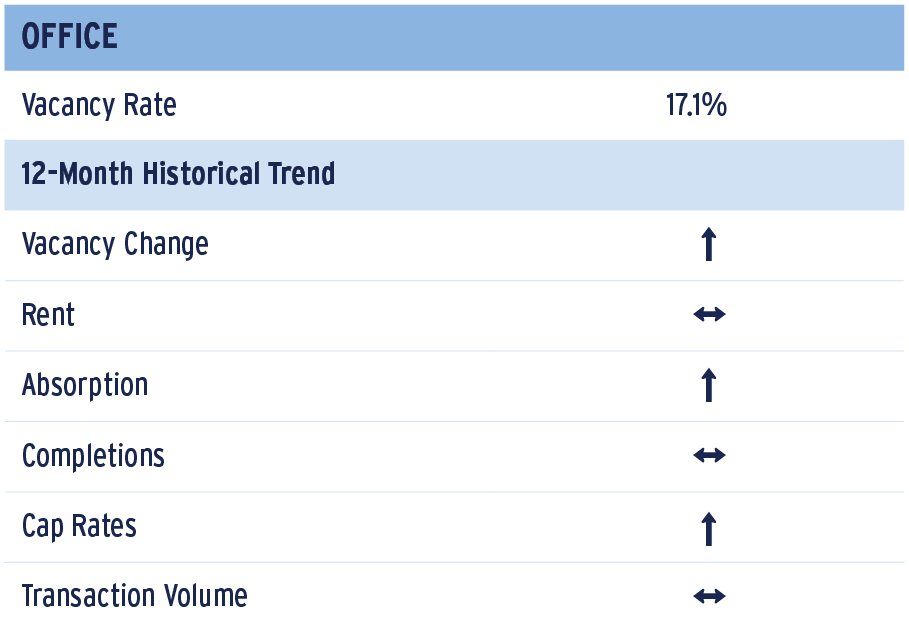

Office

The office sector has moved to a higher level of uncertainty among CRE investors regarding future values. The capital markets have clearly shifted with rising interest rates driving borrowing costs higher and constraining liquidity, not to mention the added concerns of a potential recession. While not isolated to the office sector, these pressures are compounded by the challenging demand dynamics associated with working remotely. Acceptance of the hybrid work model has become more entrenched in employee and employer expectations, which has structural implications for future demand as companies reevaluate the type, location, configuration and aggregate need for space. Health concerns do not appear to be the driving factor with most surveys suggesting a flexible work schedule, commuting, collaboration, socializing and other dynamics are of higher importance. While other metrics such as airline travel, restaurant reservations, entertainment venue attendance, etc. have returned to near pre-pandemic levels, office usage has not despite employment levels for office-using jobs sitting ~3% above 2019 levels. As a result, the market continues to struggle with subdued leasing volumes, consolidations and elevated availabilities.

Office vacancies climbed 30 bps to 17.1% for the quarter according to CBRE-EA, continuing the pattern of rising rates albeit at a slower pace than 2021. The issues remain more pronounced across downtown urban cores where vacancies stand at 17.4% or 50 basis points above suburban rates. New supply has been a factor in pushing rates higher, but not to the degree of previous cycles with current dynamics more indicative of shifting demand as tenants grapple with assessing future space needs.

OFFICE MARKET FUNDAMENTALS

Source: CBRE-EA, as of Q3 2022

In aggregate, net absorption turned positive in 2022 although the third quarter was a struggle at only 340,000 square feet according to CBRE-EA. This parallels much of what is being seen in the leasing market, which improved significantly heading into the year, but lost steam this Fall with velocity dipping to 73% of pre-COVID levels. Brokers are reporting fewer tenants in the market looking for new space with added pressures coming from the sublease market; San Francisco and Seattle being the most notable outliers. All told, sublease space now accounts for 2.2% of the 17.1% total office vacancy rate and continues to trend higher. Office tenants continue to take a measured approach to adjusting their space needs partially given existing lease commitments. That said, the number of companies announcing space consolidations or altering expansion plans has increased. Recent surveys suggest that employer and employee expectations for remote work are falling more in line with each other, perhaps adding clarity to determining future space needs. For those that have announced changes, the dynamics appear to be more skewed to reducing or reconfiguring space at renewal or upgrading to better space with a move.

OFFICE NET ABSORPTION TREND BY ASSET QUALITY* (ALL ASSETS 50K SQUARE FEET AND LARGER)

Source: Costar; assets 50,000 and larger as of 10/21/22

Note: Gateway markets include Atlanta, Boston, Dallas, Chicago, Los Angeles, South FL (Miami), New York City, San Francisco, Seattle and Washington DC *Premium Class reflects assets with a 5-star rating, Non-Premium Institutional reflects assets with a 3- or 4-star rating

Not atypical for a downturn, flight to quality among office tenants has been a notable theme this cycle. AEW Research took a closer look at the gateway markets using CoStar data and found a more pronounced flight to quality this cycle, especially across the larger gateway markets. Premium office buildings in the top ten gateway markets have maintained positive net absorption throughout the pandemic, while the balance of the institutional assets have lost ground. This has remained the case in 2022 with premium office buildings absorbing more than 9 msf of space while non-premium institutional assets experienced a decline of nearly 15 msf2.

Overall, AEW Research reaffirms its belief that many companies will embrace a more fully integrated hybrid work model that will translate into a reduction in aggregate demand; however, it will take time to fully play out as firms assess the impact of the shifting work model on productivity, profitability and the ability to retain talent. We are seeing this translate into a skewed demand for quality space and location premiums which begs the question of how this will affect commodity space that dominates the market. Office rents and values will likely be under significant pressure for the next several years.

Source: CBRE-EA, NCREIF and RCA , as of Q3 2022

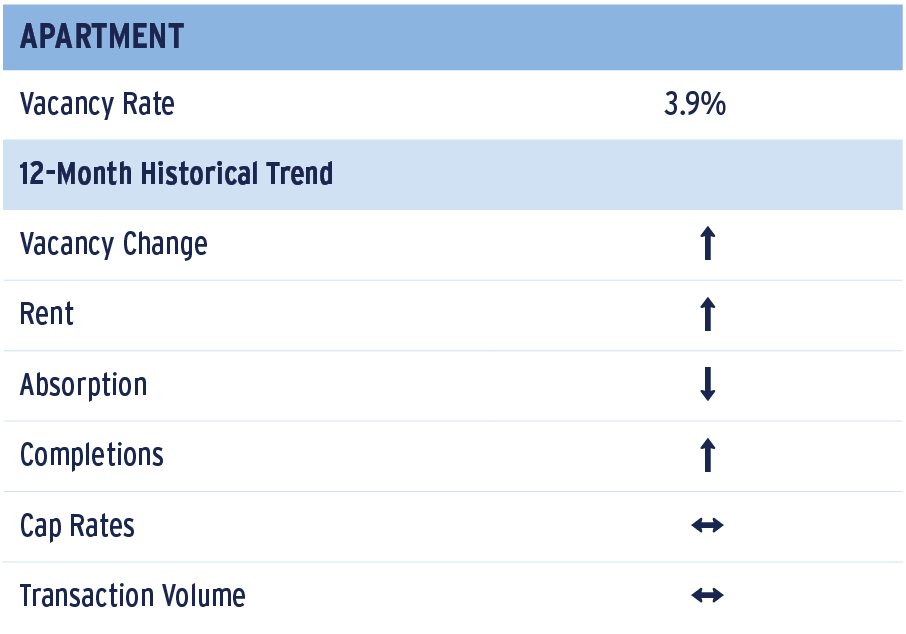

Apartment

The apartment sector is showing signs of slowing, with vacancies edging up to 3.9% in 2022 Q3, an 80-basis-point (bps) increase from the previous quarter and 90 bps from a year ago. This marks the second consecutive quarterly uptick in vacancies. While two quarters do not make a trend, heading into a weakening economic environment, it does bear watching. Moreover, it is important to note that the market remains exceptionally tight. Indeed, vacancies at 3.9% remain well below the long-term historical average of 5.0%.

On the demand side, according to Apartments.com, search activity has remained healthy over the course of year; however, searches are not converting to absorption. Indeed, per data from CBRE-EA, nearly 56,000 units were returned to the market in 2022 Q3; combined over the previous two quarters nearly 97,000 units have been returned to the market. Meanwhile, a record of roughly 92,000 units were delivered in the quarter and nearly 168,000 units have been added over the previous two quarters. It is unclear if this reversal in performance for the sector is due to seasonality, a result of diminished affordability, a return to normal after the sharp post-COVID recovery, or simply due to today’s economic uncertainty.

APARTMENT MARKET FUNDAMENTALS HAVE SOFTENED FOR TWO QUARTERS

BUT FUNDAMENTALS ARE HISTORICALLY TIGHT

Source: CBRE-EA, as of Q3 2022

By city, 21 markets reported a year-to-date (YTD) increase in vacancies that was more than two times the 90-bps increase seen nationally. Corpus Christi (8.0%, +350 bps); Phoenix (5.7%, +310); West Palm Beach (5.3%, +310); Las Vegas (5.5%, 300); and Honolulu (5.3%, 290) reported the largest increases in vacancy. Meanwhile, only four markets – New York (2.1%, -100); Madison, WI (1.3%, -70); San Francisco (4.3%, -40); and Omaha (2.5%, -30) – reported a decline in vacancy. Other major markets, including those in the Midwest, also performed better, with San Jose; Newark; Indianapolis; St Louis; Kansas City; Boston; Chicago; Washington DC; Oakland; and Los Angeles holding up better than growth markets like Atlanta, Southeast and Central Florida, Charlotte, Raleigh, Riverside, Austin and Dallas, to name a few.

The uptick in vacancies in Corpus Christi; Phoenix; West Palm Beach; Las Vegas; and Honolulu was the result of both new supply and soft demand. Las Vegas; Corpus Christi; Honolulu; and West Palm Beach were among the top ten weakest markets for demand, along with Tucson; Norfolk; Memphis; Fort Lauderdale; Albuquerque; and Sacramento, which all reported a negative YTD absorption between 1.5% and 2.4% of inventory. Meanwhile, markets with the largest increase in supply as a share of inventory included Colorado Springs; Austin; Richmond; Charlotte; Greenville; Madison; Orlando; Jacksonville; Salt Lake City; and Minneapolis; YTD supply as a share of inventory was greater than 3.0% in all the aforementioned markets.

Going forward, there are roughly 727,000 units underway with delivery expected between now and 2024. Markets with double-digit construction underway as a share of inventory include Austin (15.8%); Salt Lake City (13.9%); Nashville (12.7%); Colorado Springs (11.6%); and Orlando (10.0%). Still, based on demand trends there are very few markets that look oversupplied. The supply/demand ratios for all but a handful of markets are less than 1.25 – this compares supply as a share of inventory and average annual demand performance over the previous five years. The bulk of the supply will likely be delivered over the next two years and so we have assumed two years’ worth of demand. Based on these assumptions, markets with the highest supply/demand ratio include Salt Lake City (2.59); Colorado Springs (1.88); Sacramento (1.71); Albuquerque (1.71); Austin (1.71); and Nashville (1.53).

The risk, however, is that the U.S. tips into recession and demand is weaker than expected near-term. Over the medium-term, however, supply should slow quickly, with fewer projects being contemplated today due to rising construction costs, a lack of construction debt and greater economic uncertainty. Thus, after the pipeline underway is completed, we expect a more moderate delivery pace, which should allow for a relatively quick recovery should demand fall short of expectations. Long-term, we believe multifamily fundamentals should remain healthy, supported by continued demand and a broad undersupply in housing that has persisted since the Great Financial Crisis.

Source: CBRE-EA, NCREIF and RCA, as of Q3 2022

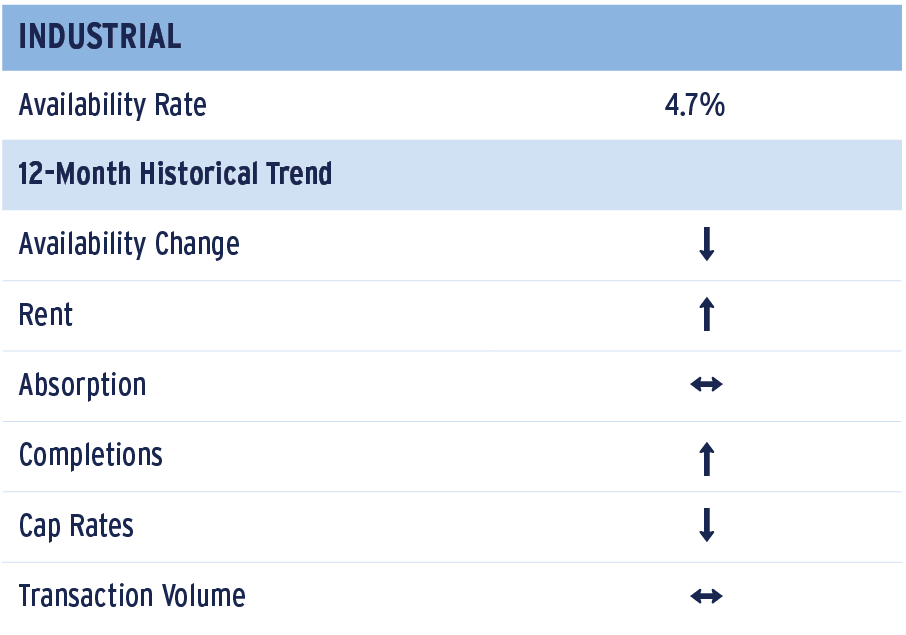

Industrial

As of the third quarter of 2022, the industrial sector is starting to show signs of cooling off, a departure from its recent boom. Over the last few years, the rise in e-commerce has supported high levels of demand for industrial space and declining availability. After eight consecutive quarters of tightening, the U.S. industrial sector has seen an increase of 10 basis points (bps) in the national availability rate. As of 2022 Q3, it now stands at 4.7%. This is still 270 bps below the pandemic peak of 7.4% and 450 bps below the sector’s historical average of 9.5% (per CBRE-EA, tracked since 1989 Q1). While seeing a slight increase in availability this quarter, the industrial sector is still performing better than nearly any other time in history; the previous quarter was the sector’s record tightest availability at 4.6%, making this quarter the second tightest. The outlook for the U.S. industrial sector is still favorable but increases in supply and slowing demand could indicate potential headwinds.

In the third quarter of 2022, demand moderated with net absorption of 81.1 million square feet (msf), a slowdown from a quarterly average of 124.4 msf over the last two years. Moreover, in each of the last seven quarters, net absorption has totaled more than 100.0 msf. While net absorption in the quarter was 35% lower than the previous two years, Q3 demand was 60% higher than the historical quarterly average of 49.9 msf. As national demand took a dip, completions rose. This quarter, completions totaled 101.2 msf, the highest level of new supply seen in over two decades, since 104.6 msf were completed in 2000 Q4. Over the last two years, quarterly deliveries averaged 77.3 msf; completions this quarter are up 31% from that average. Additionally, this is the first quarter since 2020 Q2, the peak of the pandemic, where new supply has outpaced demand.

U.S. INDUSTRIAL FUNDAMENTALS

Source: CBRE, as of Q3 2022

The national trends were reflected in the performance across most markets. Of the 69 markets tracked by CBRE-EA, 51 reported an increase in availability this quarter. However, 50 markets reported a decrease in availability year to date, revealing that this increase has not undone the overall improvements seen so far in 2022. Of the set of markets that reported a decrease in availability this year, the average improvement was roughly 110 bps.

INDUSTRIAL LOSS TO LEASE

(INDEX 2017Q4 = 100)

Source: CBRE-EA. Aggregate percentages are the loss-to-lease after adjusting for 2.5% annual contractual rent bumps, as of Q3 2022

This quarter, 36 markets reported that new supply outpaced demand. Nonetheless, many markets still reported levels of demand that surpassed completions. In the 33 markets that reported demand outpacing supply, the gap between demand and supply averaged 865,000 sf. The largest gap was in Minneapolis, where net absorption exceeded completions by 7.2 msf. This was followed by Stockton (3.4 msf), Fort Worth (2.3 msf) and Kansas City (2.1 msf). Some of the top-performing markets in terms of year-to-date availability improvements include Nashville (-220 bps), Minneapolis (-210 bps), Tucson (-210 bps), Charleston (-190 bps) and Cincinnati (-180 bps). The markets with particularly tight availability rates include Albuquerque (1.2%), Charleston (1.9%), Salt Lake City (1.9%), Las Vegas (2.0%) and Savannah (2.0%).

Per CoStar, leasing in the third quarter slowed even as a record 148 msf of new projects were delivered, a large share of which was built on speculation. This comes at a time that Amazon, the industrial sector’s largest tenant, is reducing its extensive footprint. After rapidly scaling up during the unprecedented rise in e-commerce during the COVID-19 pandemic, this dominant online retailer announced it will be tapering off its leasing and development of industrial space. As of October 2022, Amazon has withdrawn or delayed development of 50 msf of space, having an outsized impact on the slowing leasing in the sector.

As mentioned in the previous quarterly outlook, AEW Research has expected moderation in the sector due to the aforementioned challenges. However, even as the sector is decelerating, industrial fundamentals still remain solid. The availability rate, while slightly up this quarter, is still lower than every quarter except 2022 Q2. Additionally, rents have been driven higher yet. In the third quarter of 2022, the CBRE-EA asking rent reached a new record high of $9.54, up 12.1% year-over-year.

Industrial rent growth is likely to moderate in the near term as new supply and more restrained demand due to heightened economic uncertainty yield slightly higher availability rates in most markets. Despite this, significant “loss to lease” remains imbedded in most markets suggesting continued outsized property income growth (NOI) as existing leases roll over. This should dampen any near-term increases in investors’ required property yields (cap rates).

Source: CBRE-EA, NCREIF and RCA, as of Q3 2022

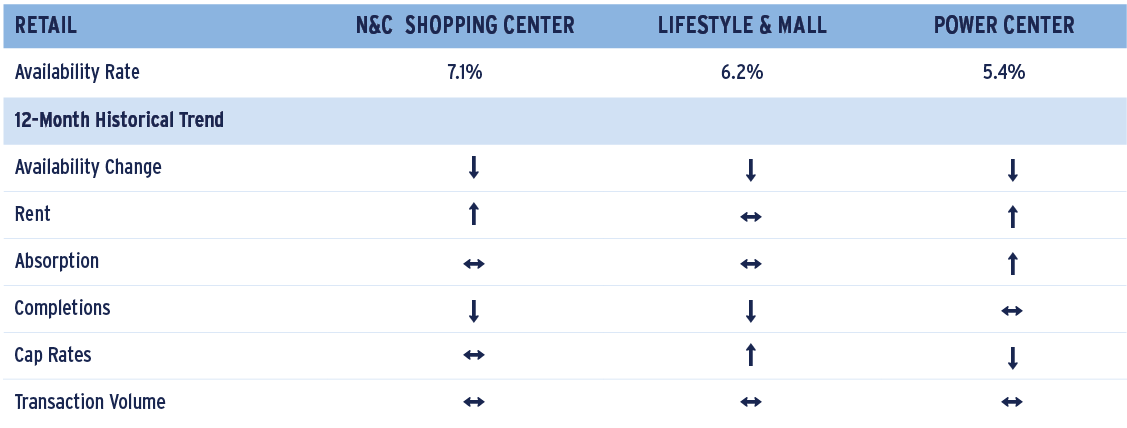

Retail

As of the third quarter of 2022, the retail sector is performing relatively well, as low levels of new supply and solid net absorption have tightened availability rates for total retail. Per CBRE-EA, 2022 Q3 total retail availability stood at 5.0%, down 10 basis points (bps) from the prior quarter and down 90 bps year-over-year (YOY). This is a new record low for availability for the sector, which now stands 250 bps below the historical average availability of 7.5% (tracked since 2005 Q1). This quarter, net absorption stood at 14.3 msf; this is below the short-term average of the prior four quarters (28.4 msf) and the long-term historical average (19.0 msf). Even so, net absorption outpaced the negligible levels of new supply, which stood at 6.3 msf this quarter. Over the last three years, quarterly supply has averaged just 8.5 msf; this is down significantly from the prior three years’ average of 14.8 msf. Rising construction costs, resulting from labor shortages and inflation of raw materials’ prices, have contributed to this dearth of new supply as well as weaker post-GFC demand as the retail sector struggled under the weight of retailer bankruptcies. With record-low availability, rents are also climbing with the gross asking rent ($20.16/sf), net asking rent ($20.69 /sf), and EA asking rent ($22.55/sf) each reaching new highs.

The neighborhood, community, and strip center (NCSC) subtype showed favorable performance this quarter. As of 2022 Q3, availability was 7.1%, down 20 bps on the quarter and 120 bps on the year. As seen with total retail, this is the tightest availability rate in the subtype’s history. This quarter, just 1.4 msf were delivered, a significant reduction relative to the 3.9 msf average quarterly completions seen over the last decade. Net absorption stood at 6.4 msf, outpacing completions by a wide margin. Of the 64 markets tracked by CBRE-EA, the year-to-date (YTD) availability rate decreased in 58 markets; this subset reported an average improvement of 100 bps. Some of the largest improvements in availability this quarter were seen in Albuquerque (-340 bps); Austin (-160 bps); Philadelphia (-160 bps); and San Antonio (-160 bps).

RETAIL SECTOR FUNDAMENTALS

Source: CBRE-EA, as of Q3 2022

The power center subtype is also reporting improving fundamentals. The third-quarter availability rate of 5.4% is down 20 bps on the quarter and 130 bps on the year. This is the lowest availability rate for the subtype in over five years and is 90 bps below the historical average of 6.5%. This quarter, 1.7 msf of net absorption outpaced completions of 169,000 sf. Availability improvements were widespread, with 54 markets reporting a decrease in availability YTD, with this subset reporting an average improvement of 130 bps. Improvements of 100 bps or more YTD were seen in 28 markets. The largest improvements were in Honolulu (-440 bps); West Palm Beach (-400 bps); San Francisco (-390 bps); and Jacksonville (-350 bps).

CONSUMER CONFIDENCE

Source: The Conference Board, as of Q3 2022

The lifestyle & mall (L&M) subtype held steady this quarter. The third-quarter availability rate stood at 6.2%, on par with the prior quarter and down 30 bps YOY. Just 23,000 sf were absorbed this quarter, less than the 480,000 sf of new supply. Rents have not yet fully recovered to pre-pandemic levels, as the EA asking rent of $34.02/sf is still 1.0% below its 2019 Q1 peak of $34.35/sf. When looking at L&M fundamentals by market, performance varied significantly. Jacksonville has the highest availability rate in the nation at 19.8%, up 520 bps YTD. Of the 64 tracked markets, 41 reported decreases in availability this year, with this improving subset reporting an average decrease of 200 bps. This was driven by outsize shifts in a few markets. The availability rate in Albuquerque has improved by 15.2 percentage points YTD and now stands at 1.2% availability, while Cincinnati reported an improvement of 12.7 percentage points YTD and now stands at 7.0% availability. Other markets with significant decreases YTD include Tulsa (-520 bps); Birmingham (-510 bps); Tucson (-370 bps); and Phoenix (-370 bps).

Retail sales, a driver of retail demand, were flat in September 2022. Weaker vehicle and fuel sales contributed to this performance. Meanwhile, core sales, excluding autos and gas, rose 0.3% in the month. September’s core sales gains were driven by strong department store, restaurant, online, apparel and drug store sales. While core growth outpaced expectations in the month, sales have slipped slightly over the last three months and several headwinds to sales are still present. Supply constraints continue to limit purchases of some goods while consumer confidence has softened, and inflation-adjusted income has been falling. So far, consumers are showing a willingness to spend some of their excess savings, but we will continue to watch the consumer in response to rising interest rates and greater economic uncertainty.

Source: CBRE-EA, NCREIF and RCA, as of Q3 2022

1 Seasonally adjusted at annual rates. Data through September 2022. Source: Commerce Department.

2Premium office buildings defined as 5-star assets over 50,000 sf and non-premium defined as 3- or 4-star assets over 50,000 based on CoStar data.

This material is intended for information purposes only and does not constitute investment advice or a recommendation. The information and opinions contained in the material have been compiled or arrived at based upon information obtained from sources believed to be reliable, but we do not guarantee its accuracy, completeness or fairness. Opinions expressed reflect prevailing market conditions and are subject to change. Neither this material, nor any of its contents, may be used for any purpose without the consent and knowledge of AEW.