- Macroeconomic drivers for retailers have become more supportive, as Eurozone 2026–30 real retail sales are projected to grow by 1.5% p.a.. Even if consumer confidence remains below pre-COVID levels, it has improved from 2023 lows and remained stable during recent challenging geopolitical uncertainties.

- In-store retail sales are forecast to grow by a modest 0.4% p.a. over the next five years, an improvement from the zero growth in 2016–2020. E-commerce penetration is still projected to reach 19% of Eurozone retail sales by 2030, but the pace at which it negatively impacts in-store sales is expected to slow down.

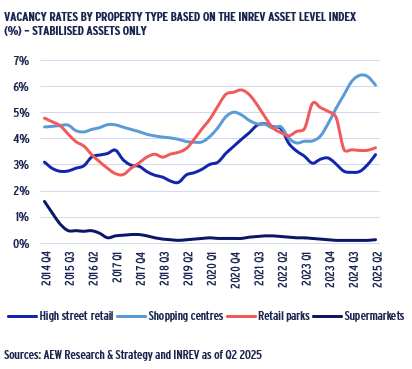

- Retail vacancy rates have moderated in varying degrees across sub-sectors from their 2020–21 COVID-related highs, with shopping centre vacancy at 6%, high street retail at 4%, and retail parks at 4% for Q2 2025.

- As a result, 2026–30 rental growth across retail sub-sectors is projected to be positive, with shopping centres, high street retail, and retail parks are expected to have increases of 1.2%, 1.6%, and 2.7% p.a., respectively.

- Transaction volumes for European retail came in at €31bn in 2025 still well below their €78bn peak in 2015. Concerns about e-commerce and interest rates drove a significant repricing. However, a recovery is now emerging as the share of retail within total transaction volumes has recovered to 16% in 2025 from a low of 10% in 2021.

- Retail transaction volumes can be expected to increase further as manager sentiment for retail has improved in Q4 2025. Over the last 3 years, retail has shown the biggest sentiment improvement among all four core sectors.

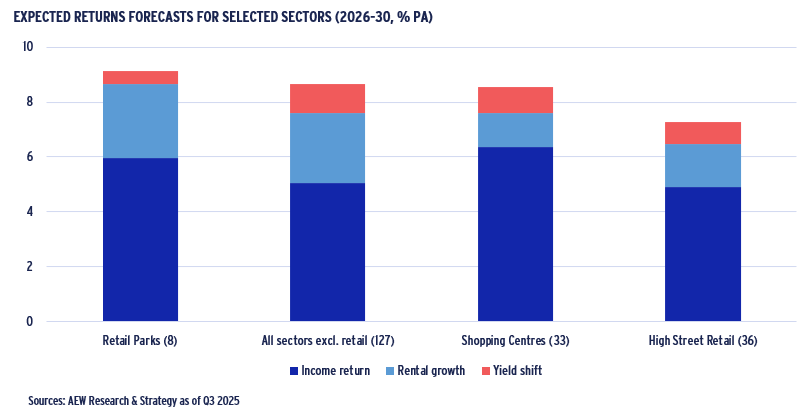

- In terms of projected 2026–30 returns, retail park returns are 9.2% p.a., exceeding our projected 8.7% p.a. for non-retail sectors, while shopping centres and high street retail trails behind at 8.6% and 7.3% p.a., respectively. Projected retail capital returns are more moderate than for non-retail, emphasising their focus on current income.

- Finally, our relative value framework shows that Spanish shopping centres rank top with the highest risk-adjusted return across all country‑sector segments. German and Italian shopping centres also feature in the top five, followed by Spanish high street retail in sixth position. Retail parks are not yet part of this framework.

SUPPORTIVE MACROECONOMIC DRIVERS

CONSUMER CONFIDENCE SIGNALS RECOVERY IN RETAIL SALES

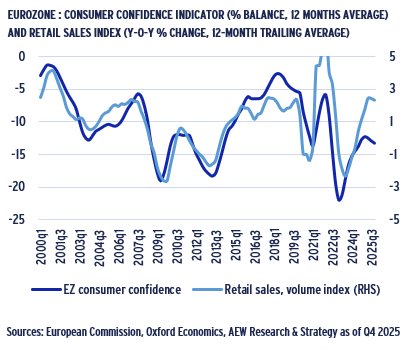

- Drops and spikes in consumer confidence often precede movements in retail sales, and the Eurozone series are highly correlated as shown in the chart.

- European consumer confidence has been predominantly negative since 2000, indicating persistent consumer pessimism over the period.

- Regardless of this sentiment, retail sales growth was generally positive over the last 25 years.

- Some exceptional shocks such as GFC, sovereign debt crisis, global pandemic and recent inflation-driven crisis did show a negative impact on retails sales.

- With positive albeit modest GDP growth in our base case, unemployment is expected to stay low which should facilitate improvement in future consumer confidence.

FOOD & HOSPITALITY BANKRUPTCIES AHEAD OF OTHER RETAILERS

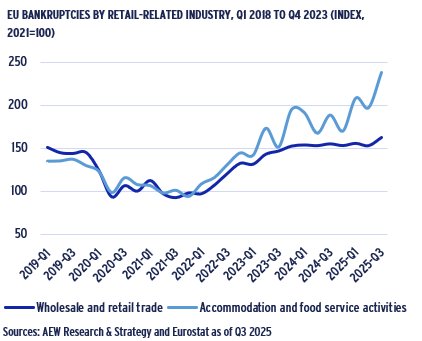

- Investors should be concerned about the credit strength of tenants. Bankruptcies for retail-related businesses has continued to trend up in the last year.

- Retail and wholesale bankruptcies might be skewed towards wholesale rather than retail, but limited data does not allow confirmation of this.

- Covid-era government supports shown their positive impact in 2020-22. As they were withdrawn, bankruptcies returned to 2015 levels.

- However, accommodation and food service businesses have shown higher level of bankruptcies in the post-Covid period. More worrying, they are still increasing

- Again, the combination of accommodation (hotels etc.) and restaurants does not allow for retail specific bankruptcies, as they are not part of pure retail assets.

STORE-BASED SALES POSTIVE BUT TRAILING OVERALL RETAIL SALES

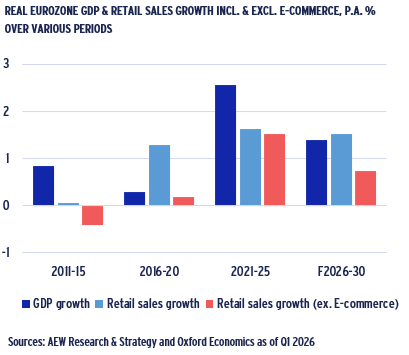

- Over the next five years, eurozone real GDP is projected to grow at 1.4% p.a. and real retail sales by 1.5% p.a., exceeding most pre-Covid periods.

- However, the strong 1.5% p.a. rebound for in-store sales (excluding e-commerce) in the 2021–25 post-Covid period is projected to fade to 0.7% p.a. for 2026–30.

- Projected 2026–30 growth is still better than the pre-Covid periods of 2011–15 and 2016–20.

- Weak 0.2% p.a. in-store retail sales in the 2016–20 period were driven by Covid lockdowns and the more rapid increase in e-commerce penetration in that period.

- Overall and in-store sales in the 2011–15 period were negatively affected by the GFC-related recession.

- Going forward, some downside risks remain from global geopolitical uncertainties such as wars and trade tariffs.

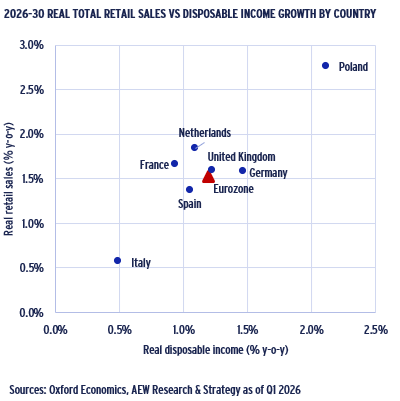

PROJECTED RETAIL SALES AHEAD OF DISPOSABLE INCOME GROWTH

- 2026–30 real retail sales are expected to grow at 1.5% p.a. and 1.6% p.a. in the Eurozone and in the UK, respectively.

- These increases might be unsustainable as they are well above the projected growth in real disposable income of 1.2% p.a. for both the Eurozone and the UK.

- These projections implicitly assume that households prioritise retail spending over big expenditures like homes or cars, using their savings or taking on new debt.

- Higher rates and tighter lending terms might be affecting borrowing for homes and cars more than credit provision for regular consumer spending.

- The wealth effect of increasing house prices and stock prices could have been a driver for some consumers.

- Again, France stands out with the widest gap between its strong 1.7% p.a. projected real retail sales and modest 0.9% p.a. real disposable income growth.

- However, Italy, with very low income and retail sales growth, and Poland, with the highest income and sales growth, present the more extreme outliers.

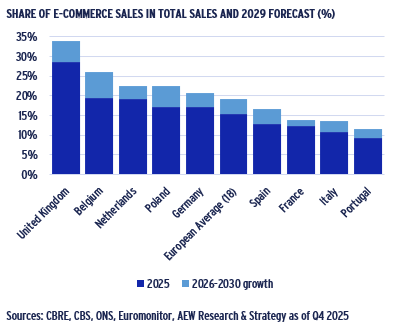

SHARE OF E-COMMERCE TO RISE TO NEAR 20% BY 2030

- Physical store sales have been impacted by the ongoing growth of e-commerce over the past decade. As of 2025, e-commerce sales account for 15% of total retail sales.

- Looking forward, this growth trend is expected to persist, with the average share of e-commerce retail across 18 European countries projected to rise to 19% by 2030.

- This marks a return to the slower pre-COVID trend of rising e-commerce penetration, following the record levels achieved during the 2020–21 COVID restrictions.

- As the share of e-commerce continues to grow, it remains uncertain when it will stabilise and at what level.

- The United Kingdom is still expected to see a further increase, with e-commerce projected to account for about one third of retail sales by 2030.

- Across countries, Belgium and Poland are projected to experience the biggest increases in e-commerce, while Spain, France, and Italy likely to remain below the average.

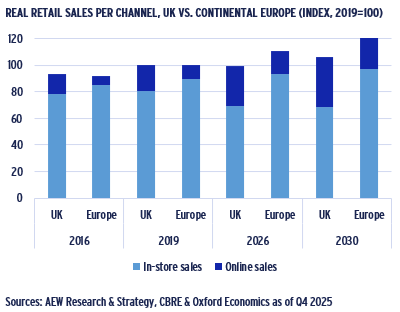

EUROZONE IN-STORE SALES PROJECTED TO RECOVER, BUT NOT IN UK

- Overall retail sales growth in Europe are led mostly by e-commerce, as can be clearly seen from the chart.

- Online sales are expected to grow by 6% p.a. in the UK and 8% p.a. in the rest of Europe for the 2026–30 period.

- The UK has experienced a big drop in in-store sales during the pandemic. Neither by 2026 or 2030, UK in-stores sales are expected to recover to 2019 levels.

- However, the situation is different in the rest of Europe, where e-commerce penetration has been less prevalent.

- European in-store sales are projected to be 4% higher in 2026 than the pre-pandemic level of 2019.

- Furthermore, in-store sales in the rest of Europe are expected to grow annually at 1.0% for the 2026–30 period.

- Despite lower sales growth projections for physical stores, many legacy retail operators need them to execute their omni-channel strategies.

RETAIL OCCUPIER MARKET

VACANCY TRENDS DIVERGE WITH SHOPPING CENTRES STABILISING

- Vacancy rates across different retail sub-sectors show some diverging trends based on the latest INREV asset-level data.

- These data reflect a concentration of high-quality assets in a small number of countries and are not fully representative of European retail markets.

- Shopping Centre (SC) vacancy stood at 6.1% in Q2 2025, down from a record high of 6.5% in Q3 2024, but remains elevated despite this recent stabilisation.

- National retailers rationalise their footprint and retaining space only in the most profitable centres is the key driver.

- On the other hand, vacancy rates for both retail park (RP) at 3.7% and high street retail (HSR) at 3.6% in Q2 2025 have both trended down over the last 2–3 years.

- Finally, supermarket vacancy remains near 0% given that they are predominantly sale-leasebacks.

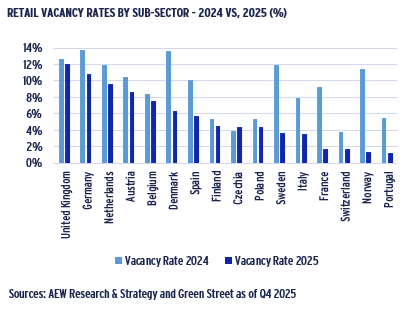

SHOPPING CENTRE VACANCY RATES NORMALISE

- In 2025, vacancy rates across European markets ranged from 1% to 12% based on the latest Green Street data.

- By comparison, in 2024 vacancy rates ranged from 4% to 13, with an average decline from 9% to 5% by 2025.

- The biggest drops were recorded in Denmark, France, and Norway, as shopping centre vacancy rates decreased across the board.

- The UK, Germany, and the Netherlands still show relatively high vacancy levels at 12%, 11%, and 10%, respectively.

- Decreasing vacancy rates suggest a recovery in total demand and more stable investment volumes.

- These data reflect an average quality of assets and are deemed more representative for European retail markets.

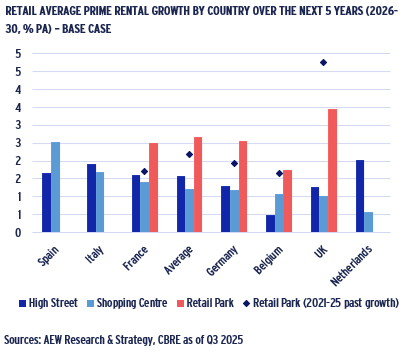

RETAIL PARK RENTAL GROWTH AHEAD OF OTHER SUB-SECTORS

- Across the three main European retail sub-sectors, 2026–30 prime rental growth is projected to average 1.2%, 1.6%, and 2.7% p.a. for SC, HSR, and RP, respectively.

- This stronger projected rental growth for RP is in line with actual 2.2% p.a. growth recorded in 2021-25.

- RP coverage focuses on eight countries at the national level and is not yet available everywhere.

- RP rental growth is forecast to exceed both HSR and SC rental growth in most countries.

- There is no consistent trend for SC and HSR rental growth, with five of the seven largest markets showing higher HSR than SC rental growth.

- Across available sub-sectors, prime Spanish SC markets are projected to outperform most other European countries.

- Finally, the historical bifurcation between prime and secondary retail across sub-sectors is expected to remain for some time, impacting rental growth.

RETAIL INVESTMENT MARKET

SHOPPING CENTRES LEAD REBOUND IN RETAIL SHARE OF DEAL VOLUME

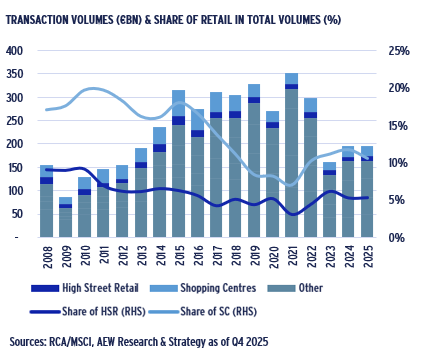

- In 2025, the share of retail in total European transaction volumes increased to 5% for HSR and 11% for SC, or 16% in aggregate.

- This was a partial reversal of retail’s gradually decreasing share from 30% in 2010 to 10% in 2021 and was driven by a decline in volumes for other core sectors.

- This, in turn, was triggered by investors’ concerns about the growing impact of e-commerce on demand for traditional retailers, particularly shopping centre space.

- The 2010–21 decline in investment volumes also coincided with a decline in retail capital values.

- The low point was 2021, when retail accounted for only 10% of total volumes, with 3% in HSR and 7% in SC — even as overall 2021 volumes set a new record.

- However painful the adjustment in capital values and yields has been for investors and lenders alike, at current pricing sufficient capital is mobilised to push volumes up.

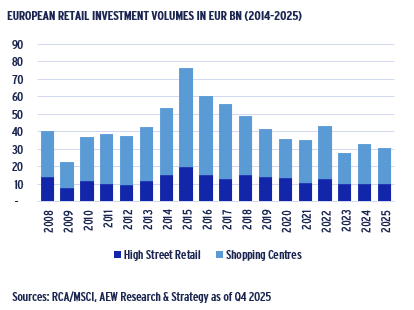

2025 RETAIL VOLUMES IN LINE WITH 5-YEAR AVERAGES

- Despite increasing share in total volumes, 2025 European shopping center volumes of €21bn were slightly below their 5-year historical average of €23bn.

- 2025 high street retail transactions are reported at €10bn, also just below their 5-year average of €11bn.

- However, it is not unlikely that 2025 volumes will increase further as more data is added to Q4 2025 totals, as usually there is a lag in deal completions and reporting deadlines.

- It is clear from the historical data that the retail sector went through a long term downcycle which started in 2016, well before recent interest rate hikes and the pandemic.

- As the advance of e-commerce created oversupply in many retail markets, it triggered capital value declines for secondary assets enabling conversion to other uses.

- This long process of adjustment has created a more balanced occupier market and attractively priced retail assets that survived these pressures.

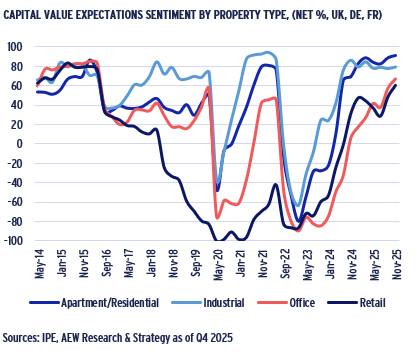

RETAIL MANAGER SENTIMENT REACHES HIGHEST LEVEL IN 10 YEARS

- Manager sentiment for retail continued to improve in Q4 2025. Over the last three years, retail has shown the biggest improvement among all four core sectors.

- In fact, 2024-25 showed a strong improvement in European managers’ sentiment across all sectors based on the latest IPE Real Assets Expectations Indicator survey.

- Our chart shows the net percentage (%) difference between the share of real estate managers who believe property values would increase vs decrease over the next year.

- Based on this, a value of 0 would indicate a neutral sentiment on a sector’s performance over the next year.

- The solid improvement in retail sentiment is likely a result of the substantial repricing of retail assets that started in 2017 well before the other sectors.

- Retail assets that managed to survive the e-commerce challenges have become attractively priced once again.

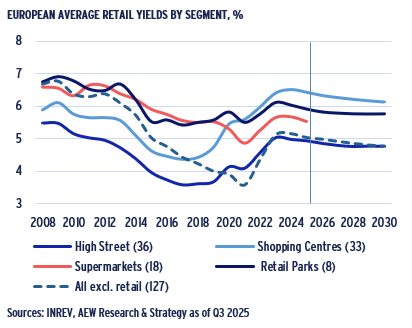

CORE RETAIL YIELDS PROJECTED TO TIGHTEN 10-30 BPS BY 2030

- We project a tightening of shopping centre (SC), high street retail (HSR) and retail park (RP) yields by 30bps, 20bps and 10 bps by 2030 from 2023-24 peaks.

- Our projected retail yield tightening is driven by the latest government bond yields forecasts which are in turn triggered by expected rate cuts as inflation has eased.

- However, prime retail yields are projected to remain above recent historical averages, reflecting the expectation of elevated bond yields and interest rates for 2026-30.

- Supermarket yields tightened during COVID, as they offered strong stability.

- Out-of-town retail park yields also tightened during COVID as access was largely unrestricted.

- Both of these sub-sectors have seen a normalisation of yields, even if no supermarket forecasts are yet available.

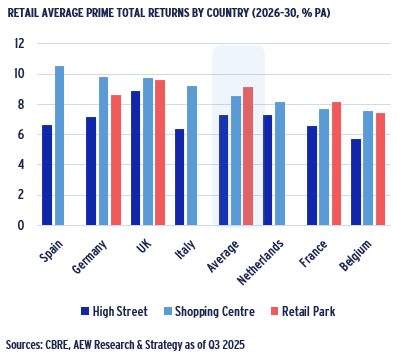

RETAIL PARKS EMERGE AS HIGHEST RETURN RETAIL SEGMENT

- Across the three main European retail sub-sectors 2026-30 returns are projected to average between 7.2%, 8.6% and 9.1% p.a. for HSR, SC and RP, respectively.

- RP coverage focuses on the national level for eight countries and is not yet available in some larger markets shown in the chart, like Spain, Italy and Netherlands.

- Shopping centre returns are expected to exceed both HSR and RP returns in most countries, with the notable exception of France.

- Across all three sub-sectors, prime UK markets are projected to outperform most other European countries, mostly due to high current income yields, even in HSR.

- Our prime returns do not reflect maintenance capex, which are significant especially for shopping centres. Green Street estimates these at 27% of net operating income.

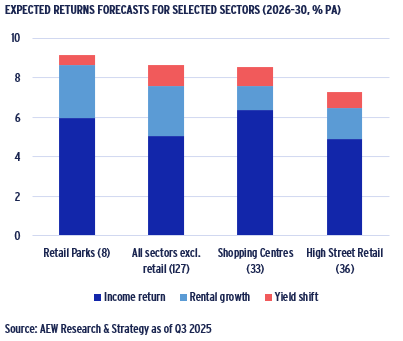

SHOPPING CENTRES & RETAIL PARKS OFFER SOLID INCOME

- At 9.2% p.a. retail park returns exceed our projected 8.7% p.a. non-retail sector returns, while at 8.6% and 7.3% p.a., shopping centres and high street retail trail behind.

- At 6.4% and 6.0% in shopping centres and retail parks offer higher current income yields compared to the 5.0% average across non-retail sectors.

- Projected capital returns for retail are more moderate compared to non-retail sectors. These are dependent on the forecasted yield compression and rental growth.

- Capital return from rental growth for retail parks at 2.7% p.a. is ahead of the 2.6% p.a. for non-retail sectors.

- Both are significantly better than the 1.2% p.a. for shopping centres and 1.6% p.a. for high street retail projected for returns from rental growth.

- Non-retail 1.0% p.a. capital return from future yield shift is in line with shopping centres but ahead of 0.8% p.a. for high street and 0.5% p.a. for retail parks.

- In case future yield tightening becomes less certain, retails’ high current income might become more appealing.

POSITIVE RELATIVE VALUE SIGNAL FOR SHOPPING CENTRES

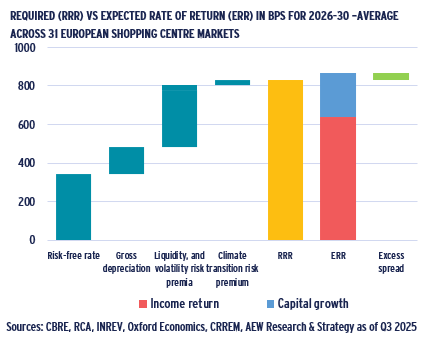

- As before, our risk-adjusted return approach is based on a comparison of the required rate of return (RRR) and the expected rate of return (ERR) over the next five years.

- To illustrate our framework, we show averages across 31 European shopping centre markets in the chart.

- Our estimated 320bps average liquidity and volatility risk premium is the second-biggest risk premium in the shopping centres sector after the risk-free rate of 343bps.

- For the 31 European shopping centre markets included in this relative value analysis, the 2026–30 average RRR is projected at 8.33% p.a. and ERR is estimated at 8.66% p.a.

- This means that ERR has a slight positive excess spread of 34bps over the RRR.

- This is a more positive outlook relative to the all-sector average, which shows a 33bps negative excess spread.

- Regardless, investors need to be selective as there are less favorable spreads in individual shopping-centre markets.

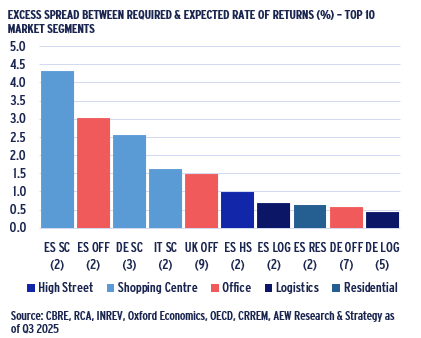

FOUR RETAIL SEGMENTS IN ALL-SECTOR TOP TEN RANKING

- Four of our top ten ranked all-sector market segments, based on the excess spread of ERR over RRR, are in retail.

- Spanish shopping centres rank top, with German and Italian shopping centres in the top five, followed by Spanish high street retail in sixth position.

- Top-ranked Spanish shopping centre markets have an excess spread of around 435bps, offering a very attractive relative value for investors.

- Spain is the most-featured country in our excess-spread top ten ranking, with all five sectors, followed by Germany with three sectors and Italy and the UK with one sector each.

- The still-prevailing beds-and-sheds preference for many investors is not confirmed by our excess spreads, as these sectors have only three segments in our top ten ranking.

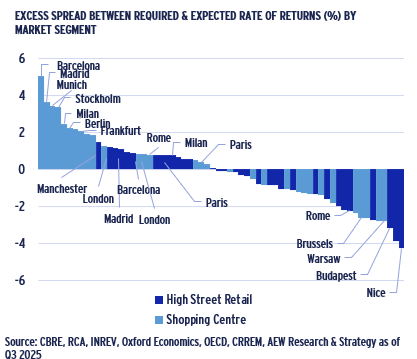

- Individual city-market results offer additional insights across the European retail markets.

MORE SELECTIVE MARKET TARGETING REQUIRED AT THIS PHASE

- As is clear from the chart, our current retail market classification is evenly balanced between positive and negative excess spreads across city-level markets.

- Critical market selection is needed since the range of excess spreads for our 64 retail segments spans from minus 430 bps (Nice HSR) to plus 500 bps (Barcelona SC).

- In general, shopping centres have more positive excess spreads than high street markets. In fact, our top-ten markets are all in the shopping centres sub-sector.

- Our top five include shopping centres in Barcelona, Madrid, Munich, Stockholm, and Milan. High-street markets with the best excess spread are Manchester and London.

- Nice, Budapest, and Rome high street are among the outliers on the negative excess-spread side, together with Warsaw and Brussels shopping centres.

- Please note that the liquidity premium for smaller markets can be punitive when there have been few recorded transactions in the last five years.

This material is intended for information purposes only and does not constitute investment advice or a recommendation. The information and opinions contained in the material have been compiled or arrived at based upon information obtained from sources believed to be reliable, but we do not guarantee its accuracy, completeness or fairness. Opinions expressed reflect prevailing market conditions and are subject to change. Neither this material, nor any of its contents, may be used for any purpose without the consent and knowledge of AEW. There is no assurance that any prediction, projection or forecast will be realized.