NEXT WAVE OF PHYSICAL CLIMATE RISK

- For any remaining sceptics, Europe’s 2022 post-Covid summer has further confirmed that climate change is for real with new record length droughts, forest fires and the Rhine river at risk of running too low for commercial shipping. These climate change extremes highlight a continuing trend from last summer’s large number of flash floods. In the mean time, policy makers have been distracted from these climate-related emergencies by trying to solve the Russia-Ukraine conflict, runaway inflation and a significant slowdown in economic growth, which looks to be soon spilling over into a full blown recession. In addition, embargo-related gas shortages are likely to force a reactivation of traditional coal plants reversing some of the previous progress in meeting the Paris accord emission reductions.

- In our third report on climate-related hazards, we limit our scope mostly to physical climate hazards. This is a topic we already addressed in our June 2021 report "Climate-informed real estate returns in Europe". As with the previous report, we focus on a quantification of the impact of physical climate hazards on European real estate returns.

- In contrast to last year, we don’t address transition-related climate risks this time. However we do note that with the increasing awareness of climate issues in the real estate investment industry, CRREM has emerged as the de facto industry standard for climate-related transition risk. Its adaptation by many leading industry groups and firms is a testament to the forward looking approach of its pathways.

- Apart from increasing our market coverage from 20 to 196 sector and city specific market segments, we are able to analyse more precise data on the various drivers of river flood risk. We will also take some initial steps to incorporate an estimate for sea level rise risk. In addition, we can do a comparison with a new data source and have an initial look at the concept of urban heat island as well. As before, these analyses do require some assumptions along the way, which we highlight together with our results.

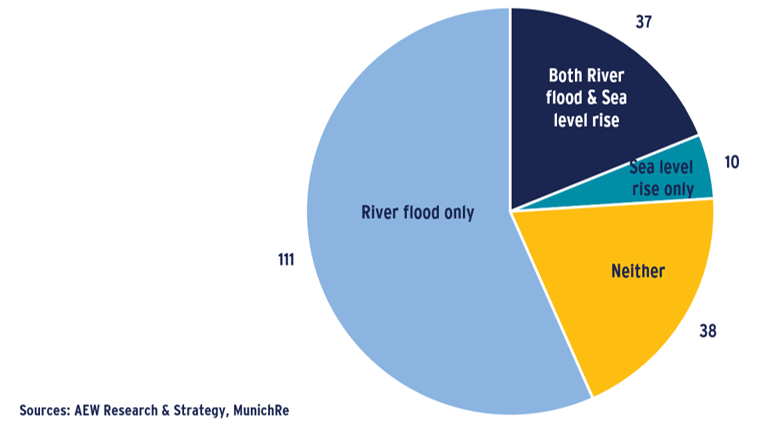

Number of market segments impacted by river flood and sea level rise risk

DESPITE MODEST MARKET-LEVEL PHYSICAL CLIMATE RISKS, EXTREMES WARRANT PRO-ACTIVE INVESTMENT APPROACH

- In this report, we provide an updated estimate of the impact of physical climate-related hazards on European real estate investment returns. This is a follow-up from our Jun-21 report on climate-informed real estate returns in Europe as we adopt the RCP 4.5 climate change scenario. In addition to Munich Re, we add a new data partner with The Climate Company (TCC).

- First the good news, despite 75% of our covered 196 market segments being affected by river flood, the average annual expected loss from this river flood risk is a relative modest 0.7 bps pa of prime capital value from an insurance perspective.

- At 1.4 bps pa French markets post double the European country average risk of river flood. Across sectors, residential’s expected loss from river flood risk is highest, albeit at a modest 1.1 bps pa.

- At an sector average of 3.6 bps pa, Lyon is the most affected city. These averages hide extreme results for individual market segments as highlighted by the near 13 bps pa loss for Lyon residential located at the confluence of the Rhone and Saone rivers.

- These extreme results for specific areas and even on a micro location and elevation level mean that investors can not ignore this risk and should adopt an active acquisition screening and portfolio monitoring approach across their investment strategies.

- Second, when we turn to sea level rise we estimate the average annual expected loss for sea level rise at 1.3 bps across the affected 47 (of 196) market segments. This is based on a pragmatic analytical approach using European sector specific river flood expected losses (for flooded areas only) and high precision data on underlying surface areas affected by sea level rise.

- Unsurprisingly, the Netherlands are most exposed to sea level rise. Rotterdam and Amsterdam have estimated sea level rise losses at above 2 bps pa. level rise cities. Dublin, Copenhagen and The Hague complete the top-5 most exposed to sea level rise cities.

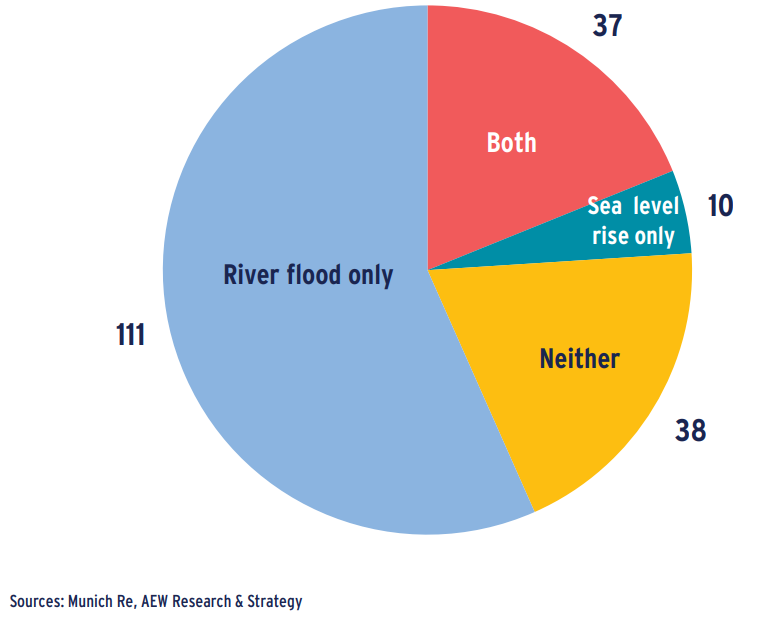

- Thirdly, we estimate the annual expected losses for both river flood and sea level rise combined at a very modest 0.8 bps pa across our entire 196 market coverage. This is due 38 of our 196 segments having no exposure to either and the combined average is further impacted by 10 markets exposed to sea level rise only and 111 of markets affected by river flood risk only and 37 by both.

- Even when we combine river flood and sea level rise expected losses for the 37 market segments that are exposed to both risks, our results shows only a modest average loss of 1.7 bps of prime capital value pa.

- Our focus on river flood and sea level risks is justified by the limitations of available data making a proper quantification in terms of expected loss not yet feasible for other climate-related hazards, such as drought, heat and precipitation stress etc.

- It would help to have more data standardisation on physical risks and resolve inconsistencies between data providers as well as improved data on subsidence - possibly the most expensive physical climate risk – and the widespread risk of urban heat islands.

River flood and sea level rise combined annual expected loss per city in RCP4.5 2050, bps of prime capital value

SECTION 1: ECONOMIC IMPACT FROM CLIMATE RISKS

GDP IMPACT CONFIRMED FROM DISORDERLY TRANSITION

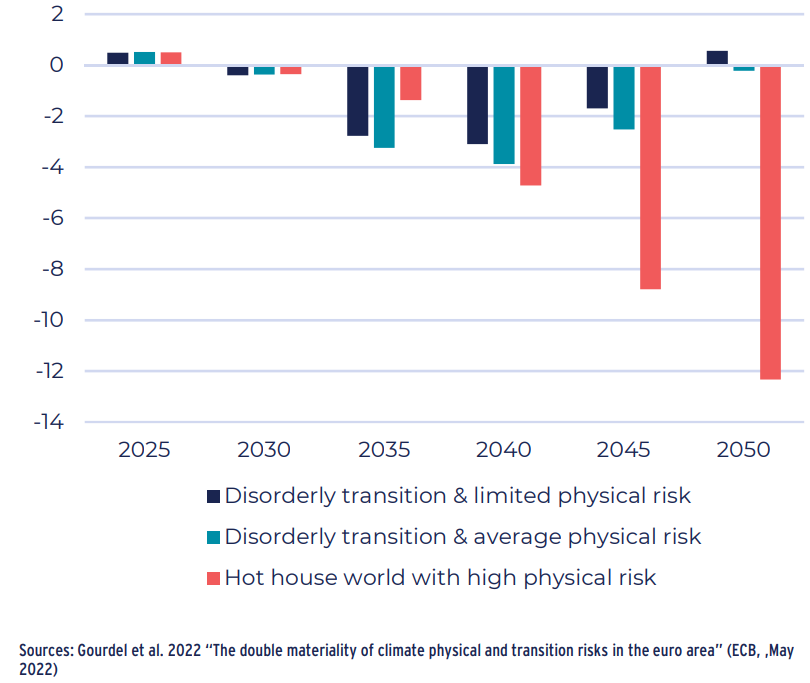

- Following up from last year’s analyses using Ortec Finance, a recent ECB research paper provides further confirmation of the GDP impact of different climate transition scenarios developed by the Network for Greening the Financial System (NGFS), assuming different climate scenarios and considering both transition and physical climate-related risks:

- Orderly transition is baseline scenario (1.5°C in 2100 scenario)

- Disorderly transition (2.0°C in 2100 scenario) with: 2a. Limited physical risks and 2b. Average physical risk

- Hothouse world with high physical risk (“business as usual”)

- The orderly transition scenario implies short-term costs to economic growth but achieves important co-benefits in the medium-term with lower carbon emissions and limited GDP impact.

- In contrast, a disorderly transition shows a negative cumulative GDP growth impact of -2.8% by 2035 compared to the orderly scenario. This negative GDP impact is amplified when physical risks are more severe (-3.3% in 2035).

- The hot house world scenario results in a more significant negative GPD growth impact of -4.7% by 2040 due to high physical risk.

- The underlying NGFS scenarios might not include sufficiently the acute physical risks and could therefore still underestimate the actual GDP impact.

Real GDP percentage deviation from the orderly transition scenario

INTEGRATING CARBON TAX POLICY INTO SCENARIOS

- The ECB paper further develops the concept of “climate sentiment” (Dunz et al. 2021), i.e. firms and banks’ expectations about the impacts of climate change and the transition on their business, and their adjustment in risk assessment, investment and lending decisions.

- Investors and lenders’ heterogeneous expectations about the credibility and impact of climate policies, such as carbon taxes, affects their risk assessment and the feasibility (and costs) of the transition.

- Firms and banks’ awareness of climate policy scenarios could ensure a smooth low-carbon transition and limit physical risks.

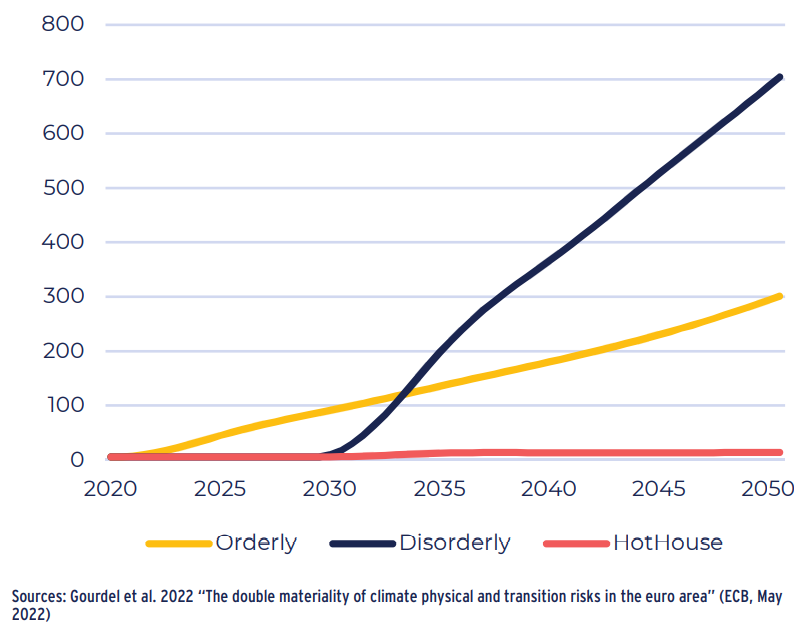

- The orderly transition scenario assumes an immediate and gradual increase in carbon prices, facilitating the transition to a low-carbon economy.

- The disorderly scenario assumes a later and sudden increase in carbon prices. This triggers sharper emission reductions to meet the Paris Accord commitments, higher adjustment costs for firms, and give less time for market players to adjust.

- In the hot house scenario, no carbon tax is implemented (business as usual).

- At the same time, market players need to adjust their risk assessment of physical climate risks and mitigate these risks

Carbon price in US$2010/t CO2 - Different scenarios

TRANSITION AND PHYSICAL RISKS ARE INTERCONNECTED

- In our Jun-21 report, we quantified transition risks by using the CRREM tool as it estimates the costs for building owners to comply with the Paris accord greenhouse gas (GHG) emission reduction pathways.

- Also, we did have an initial estimate of physical climate risks on 20 market segments, which arise from the impact of natural hazards on physical assets such as buildings.

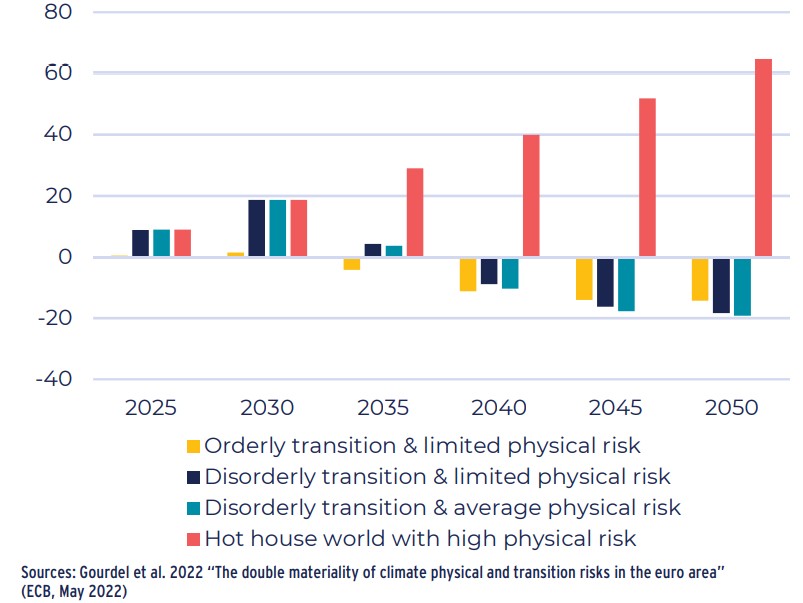

- The ECB analysis highlights that physical and transition risks are interconnected. Delaying the reduction in GHG emissions (or not implementing existing policies or commitments) leads to a higher probability and intensity of physical climate-related hazards.

- This is highlighted by the hot house scenario which assumes no additional policies and very high climate physical risks from 2030 in GDP growth terms.

- In the disorderly transition scenario, GHG emissions continue to rise in 2030-2035 (no additional climate policy introduced before 2030), while the orderly scenario assumes almost no additional GHG emissions from 2025. After 2030, physical damages in the disorderly scenario start to increase

Eurozone additional greenhouse gas (GHG) emissions in different scenarios (% in comparison to 2020)

SECTION 2: PHYSICAL CLIMATE RISKS

ADDITIONAL CLIMATE DATA CONSIDERED

- Our coverage now includes all 196 forecasted commercial real estate market segments in 50 cities across 20 countries, up from 5 cities last year.

- New data from The Climate Company (TCC) implicitly assumes RCP 8.5 by 2040, while Munich Re has a broader scope of Representative Concentration Pathways (RCP) scenarios same as last year.

- RCPs reflect different greenhouse gas (GHG) trajectories, as published by the UN Intergovernmental Panel on Climate Change (IPCC)

- RCP 8.5: Most severe scenario leading to a warming by 2100 of more than 4 degrees Celsius (C) relative to the pre-industrial period, and assuming that only currently announced policy initiatives are implemented

- RCP 4.5: Intermediate scenario leading to a warming of just over 2C and is aligned with governments meeting the Paris-accord commitments

- RCP 2.6: best case scenario leading to warming at the end of the 21st century of less than 2C, exceeding Paris accord policy commitments.

- Despite the recent setbacks, we adopt the RCP 4.5 scenario as our own base case as it still remains IPCC’s intermediate projection.

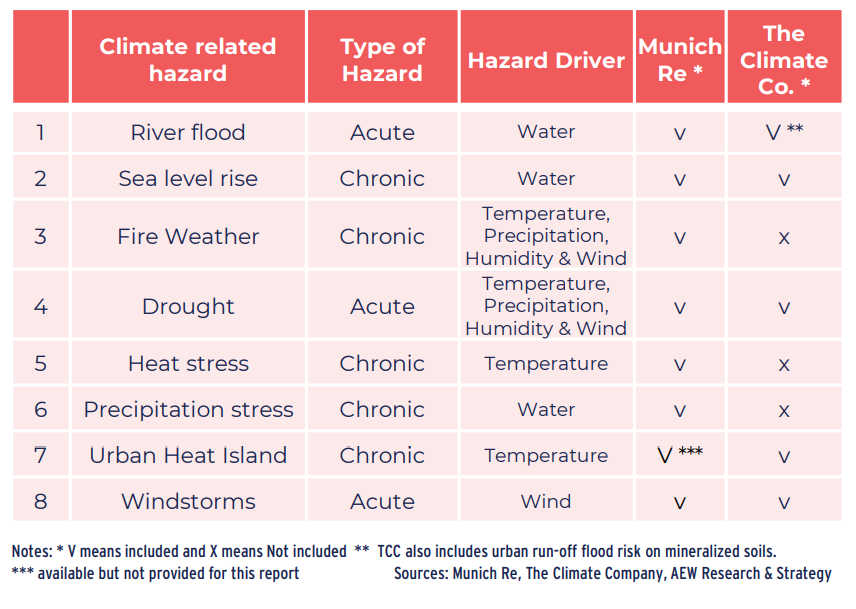

Overview of physical climate change hazards

INCONSISTENT HAZARD SCORES ACROSS TWO SOURCES

- Munich Re’s climate-related hazard scores are classified into five categories: no or very low exposure (1), low exposure (2), medium exposure (3), high exposure (4) and very high exposure (5). Across our 196 markets, their average exposure to climate related hazards is low.

- Their data allows for comparison between RCP 8.5 and RCP 4.5 in 2050 compared to current, while TCC implicitly assumes RCP 8.5 by 2040. This means the scores are not directly comparable from a timing perspective.

- Heat-related hazards show the biggest increase in Munich Re’s risk scores, compared to water-related hazards.

- But, water-related risk scores are low due to markets’ locations despite exposure of 76% to river flood risk, and 24% to sea level risk.

- TCC’s scores fall into four categories: low (1), medium (2), high (3) and severe risk (4) with an average score at medium. TCC adopts no RCP scenario and assumes no future GHG reductions -- in line with RCP 8.5.

- TCC flood risk score is almost double Munich Re’s but for other climate hazards, such as sea level rise and drought (stress) our comparison shows some further inconsistences, which will be addressed later in the report.

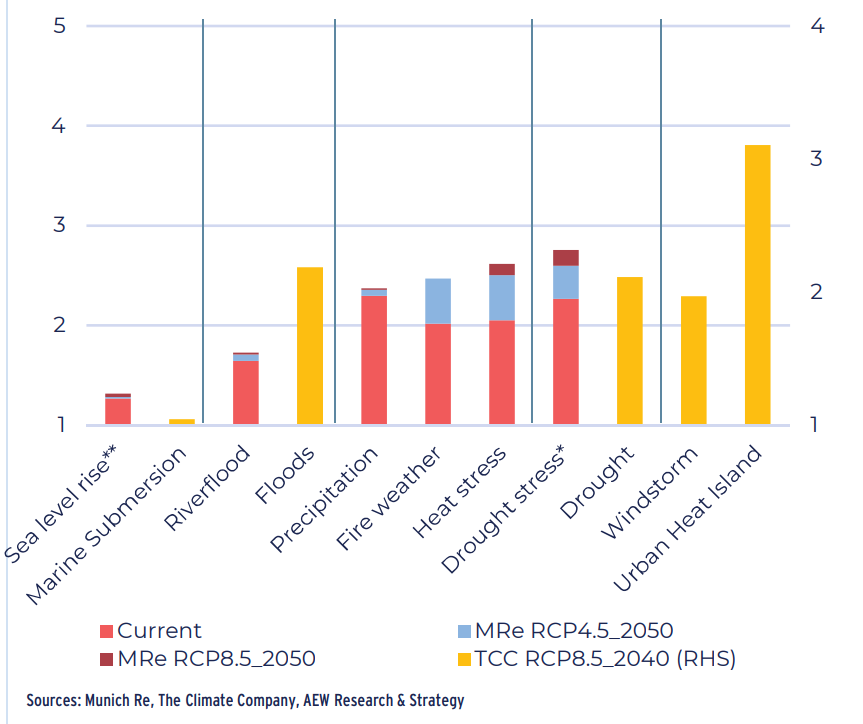

Risk scores per climate hazard across all 196 markets (Munich Re on RHS)

EXPANDED COVERAGE REDUCES MUNICH RE AVERAGE RISK

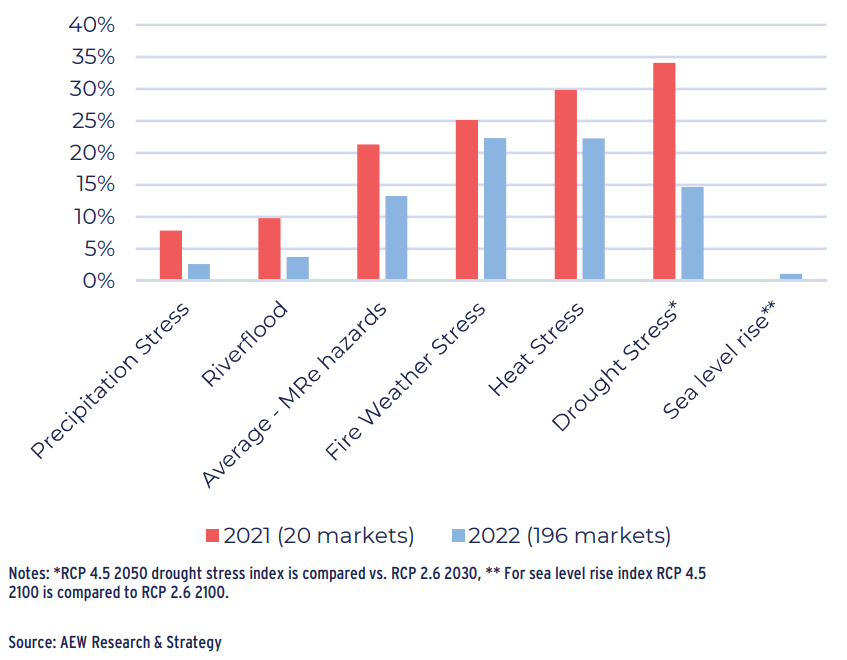

- Expanding our universe from 20 to 196 segments allows a comparison of Munich Re risk scores from current to RCP 4.5 for each hazard.

- Across all hazards, there was a consistent decrease in risk scores, as the average risk score increase came down from 21.3% for the 20 markets covered in 2021 to 13.2% for the 196 covered in the current update.

- Surprisingly, given the current news flows of many European rivers running dry -- the largest reduction in risk score is for drought stress. This came down from above 34% last year to just below 15% now. Most of these changes are simply explained by our increased market coverage.

- Similar to last year, Munich Re’s data precision allows for a higher level of analysis for river flood risk compared to the other climate hazards.

- Based on Munich Re’s feedback, there is not the same degree of potential damage on buildings from these other climate-linked hazards.

- It seems reasonable for a leading re-insurance group to maximise the visibility on the most claim-exposed climate related hazards.

- Finally, we note that there is no data on possibly the most expensive risk -- subsidence (where building foundations are damaged by clay soils affected by droughts) as it is uncovered by commercial insurance. (1)

Change in average risk score from current to 2050 for the RCP 4.5 climate scenario

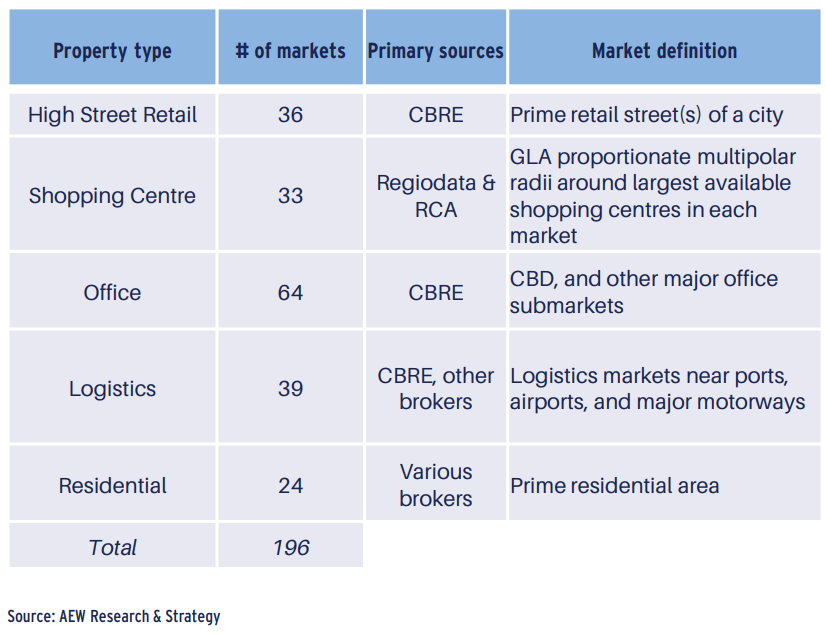

196 PRIME EUROPEAN MARKET SEGMENTS COVERED

- As mentioned, we have significantly expanded our market coverage from 20 last year to include 196 now.

- This coverage includes all European property markets for which we have market forecasts and adds two sectors (residential and shopping centres).

- Similar to last year’s approach, our focus remains on the prime definition of each of the 196 property segments covered in our forecast universe.

- Where available we use CBRE market area definitions, but where not available we use other brokers’ or local sources to define the prime area.

- Focusing on the prime area of each market segment allows us to be precise in estimating a risk premium for physical climate risks as a percentage of prime capital value.

- This will allow us to incorporate both physical and transition climate risk premiums in our upcoming 2023 market outlook report later this year.

- Our climate data providers (Munich Re and TCC) are using our prime market area definitions differently.

- Munich Re can assess the entire prime market area (with results areaweighted) but TCC’s analysis is based on a limited sampling using the centroid for each of our 196 prime market areas

Prime European market coverage and definitions

PRIME MARKETS FOR EACH PROPERTY TYPE ANALYSED

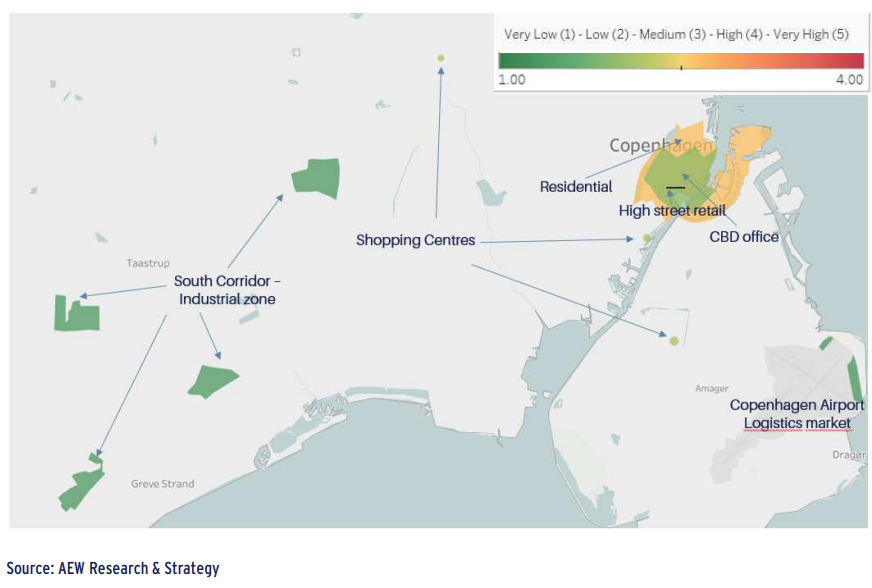

- To illustrate how our prime market area are defined, we provide the example of our covered segments in Copenhagen.

- Unsurprisingly, the size of prime market segments (or polygons) varies significantly as prime shopping centres markets consist of an appropriate radius for the 3-4 most dominant centers while the prime high street market covers only the very best retail street.

- On the other hand, prime logistics, office and residential markets tend to have larger geographic areas as illustrated on the right.

- Logistics and office markets also typically include multiple prime submarkets. As a result, these prime market segments tend to be multi-polar in our analysis, near industrial zones, air or seaports or rail hubs.

- Exposure to physical climate risks (like sea level rise) are assessed for each of the 196 prime market areas in our coverage. Area-weighted average risk scores will be impacted by an area’s size with larger areas having a higher likelihood of having at least some exposure.

Example: Copenhagen – Exposure to sea level rise by property type in 2050

HIGHER PRECISION FOR WATER-RELATED HAZARDS

- To further illustrate the importance of micro location, the physical climate risk assessment varies significantly within a city, particularly for waterrelated risk where elevation is an important variable.

- For river flood and sea level rise, data is available with a 30 metres resolution. Data on the other physical hazards are less precise at available resolution of 25 km.

- The satellite map from Munich Re on the right shows Marseille prime retail markets’ exposure to sea level rise, with the prime high streets and shopping centres highlighted in pink.

- Yellow areas are expected to be submersed by 2100 due to sea level rise, with a direct impact on the Les Terrasses du Port shopping centre.

- The nearby prime high street retail will be only indirectly impacted by this hazard as road and metro accessibility is likely to be reduced.

- It should also be noted that droughts and floods are connected in many ways. After a long drought, any precipitation will not be absorbed by the dried out soil resulting in much worse floods compared to normal.

- Finally, as a chronic climate hazard projected for 2100, sea level rise could allow time for remedies or asset write downs to be made.

Example: Marseille retail markets’ exposure to sea level rise in 2100

SECTION 3: DEEP DIVE INTO RIVER FLOOD AND SEA LEVEL RISE RISK

MOST MARKETS EXPOSED TO SOME FLOODING RISK

- 148 out of 196 covered markets currently contain areas subject to river flood risk. By 2050 this increases to 151 and 152 in RCP 4.5 and RCP 8.5.

- For these 148 affected markets, roughly 25% of their underlying areas are impacted by flooding. This goes up to 27% in RCP 8.5 2050.

- As mentioned, river flood hazard data is available with a 30m resolution and is based on bare-earth digital terrain data.

- For each prime market area segment’s polygon, there is a % value of the underlying associated area for one of three exposure zones provided.

- Munich Re defines Zone 0 as areas outside the 0.2% annual chance floodplain; Zone 500 as 0.2% annual exceedance probability flood event (500 year return period) and Zone 100 as 1% annual exceedance probability flood event (100 year return period).

- 47 out of 196 covered markets are exposed to sea level rise risk (37+10).

- Despite its high 30m resolution, sea level rise hazard is only projected for 2100 and remains largely unchanged for most market segments between the three different RCP scenarios.

Number of market segments impacted by river flood and sea level rise risk

RIVER FLOODING DEPTH PROVIDES NEW DIMENSION

- Munich Re has been able to provide a new dimension in their analyses by including data on flood depths across all markets impacted by river flood.

- Water depth estimates are based on simulations and historical observations and river flood modelling for RCP 4.5 and RCP 8.5 scenarios and the two return periods of 100, and 500 years.

- Our 0.26m estimated area-weighted average river flood depth reflects each area’s coverage of the two annual exceedance zones across all affected 148 markets based on current river flood hazard data provided by JBA Risk Management.

- This overall 0.26m average hides some significant outliers as prime market segments like Silesia, Poland, with over 1.8m mean depth and Lyon with over 1m mean flood depth.

- These overall averages include the 76% of affected segments’ areas outside flooding zones. For flooded areas only, the mean flood depth increases near fourfold increase to over 1m for flooded areas only.

- The importance of micro location is again confirmed when we highlight maximum flood heights of 12m for Silesia and Milan segments.

Average (LHS) and maximum (RHS) current river flood depths per city in meters

EXPECTED LOSS ESTIMATES

- Apart from flood depth, another big improvement in the Munich Re data is the introduction of an estimated per annum expected loss due to climaterelated river flood-caused physical building damage (2).

- Their expected loss is estimated as an annual loss rate expressed as a share of rebuilding costs, assuming a standard residential building.

- Based on these data, the estimated annual average expected loss for river flood across our 148 affected markets is 2.6bps pa in RCP 4.5 2050.

- This means that the cumulative expected loss across all 148 markets affected by river flood is 75bps (2.6 bps over 29 years) to 2050.

- The actual loss on a prime market segment level, however, will fluctuate around the expected loss for any given year.

- Across property types, office markets have the highest level of expected loss at 3.3 bps while high street retail markets are the lowest at 1.1 bps.

- Expected loss is a great advancement from the estimated increase in insurance premium used in last year’s analyses.

- Our results are at market level and do NOT yet reflect any deviation between residential and commercial building damage nor any individual buildings’ micro locations and specific technical designs and heights.

RCP 4.5 2050 annual expected loss for river flood risk per sector, bps of replacement cost

BOTH POSITIVE AND NEGATIVE CHANGES IN FLOOD RISK

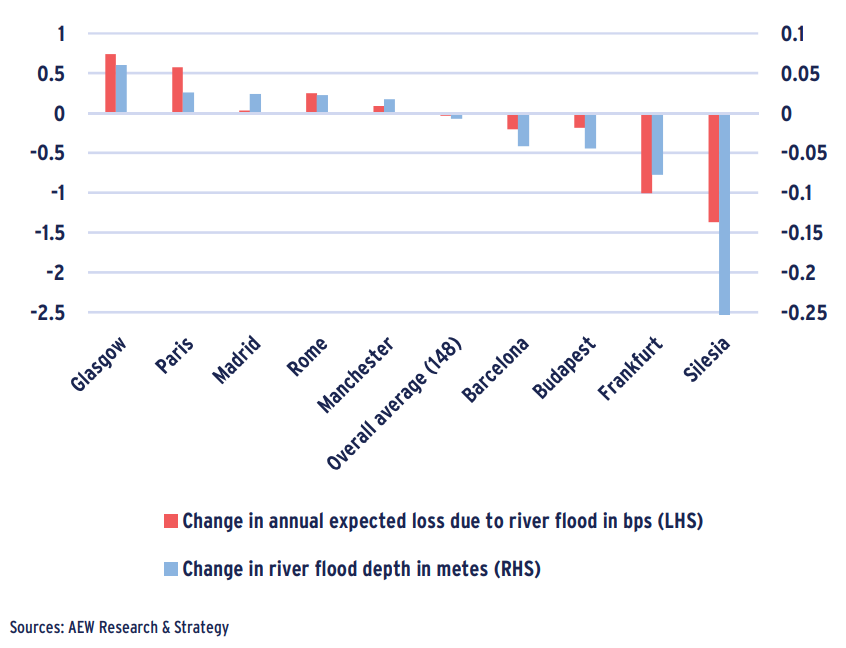

- When we combine Munich Re’s new flood depth and expected loss data it becomes evident that not all cities will see higher levels of flooding when we consider the change from current to 2050 in the RCP 4.5 scenario.

- Surprisingly, some cities are projected to experience lower river flood risk, which includes both overflow and runoff. In fact, a small number of markets are showing very large declines.

- As a result of these offsetting results among cities, both the overall average depth of flooding and expected loss only show marginal change from current. As usual, an average can hide significant differences.

- The largest increases from current to RCP 4.5 2050 in flood depth and expected loss are observed in Glasgow, Paris, Madrid, and Rome.

- In other markets, higher temperatures result in rivers drying out, like in Barcelona, Budapest, Frankfurt and Silesia, triggering decreases in the mean average flood depths and associated expected losses.

- We focus in on river flood risk because with the currently available data we are unable to properly quantify other climate-related risks, such as drought, urban heat island, and fire weather in expected loss terms.

Change in expected loss and average flood depth from current to RCP 4.5 2050

AVERAGE FLOOD DEPTHS DRIVE EXPECTED LOSSES

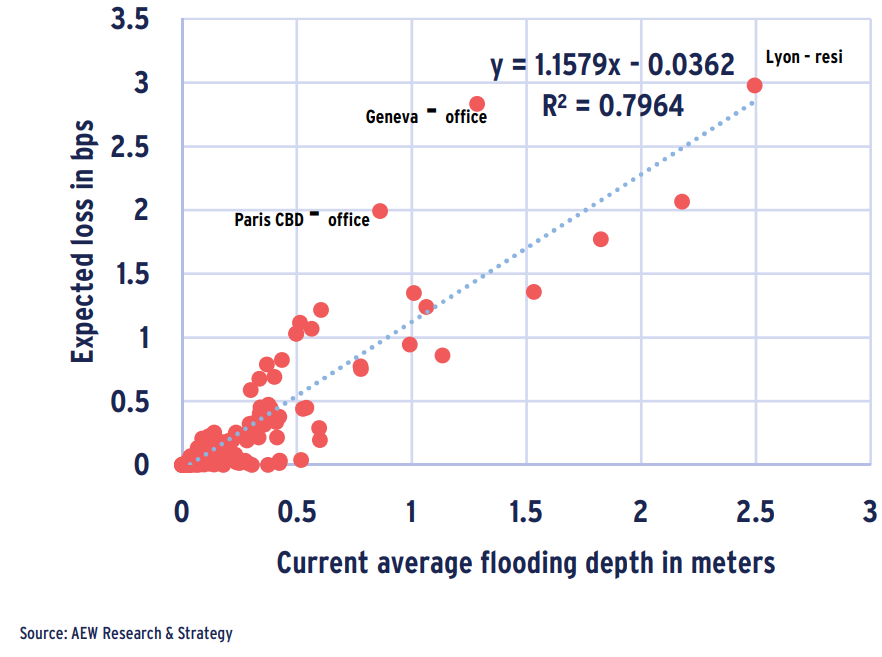

- Based on our above analysis, it seems that flood depth is the primary driver that determines the expected loss for river flood.

- Our scatter chart shows both the expected loss per market and the mean depth of river flood for each of the 148 affected by river flood markets.

- The best fitted line shows a strong positive correlation between the two variables. Our R-squared shows that near 80% of the variation in expected loss is explained by a market’s modelled flood depth.

- This means that for each market on average, a one meter increase in mean flood depth will drive an 1.15 bps increase in annual expected loss.

- It is noted that the Paris CBD and Geneva office segments are outliers and the furthest markets from the fitted line.

- Despite some limitations, using this causal and precise relationship between flood depth and expected loss allows us to model average expected loss for river flood levels across different areas, such as flood areas only, or maximum points of flooding, which are discussed a bit later.

- Please note that we also tested the relationship between the risk scores and expected loss directly, but did not find a strong linear relationship.

Flooding depth is the main driver of expected loss

FROM REPLACEMENT COST TO PRIME CAPITAL VALUE

- Munich Re provides expected loss estimates as a percentage of replacement costs. However, real estate investors are more used to thinking in terms of prime capital values.

- Therefore, we need a way to adjust for the difference between replacement costs and prime capital values to convert loss as a percentage of prime capital values. We do this in two steps.

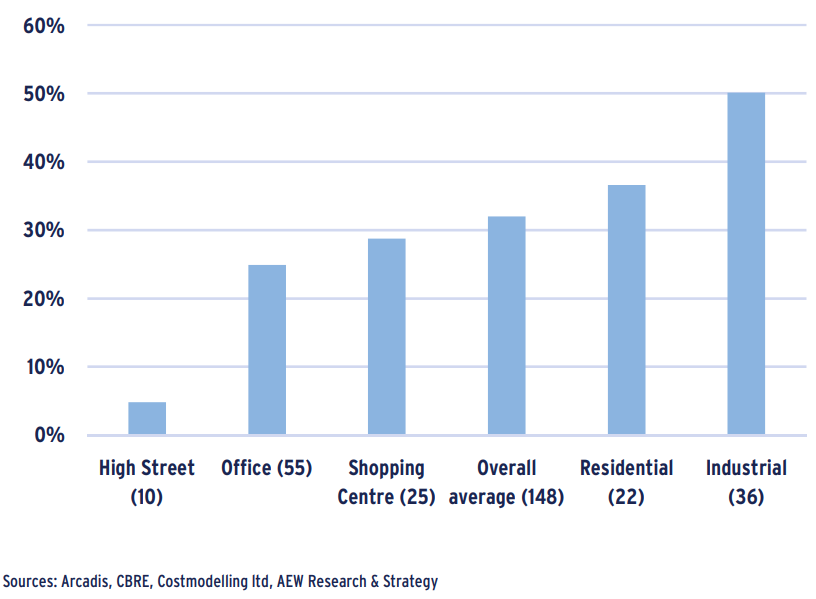

- First, we calculate replacement costs, by using the Arcadis international city-level construction cost index and Costmodelling’s detailed standard construction cost estimates per property type.

- Second, we take the ratio of the estimated replacement costs as percentage of our CBRE prime capital value for all 148 market segments.

- Across all sectors, replacement costs constitutes 32% of prime capital values as at Q2 2022, with industrial at 50% and prime high street at 5%.

- These relatively low ratios are explained by the prime nature of CBRE capital values stressing the importance of location and it’s associated high proportion of land value.

Replacement cost, as % of prime capital value

LOW AVERAGE LOSSES HIDE OUTLIERS

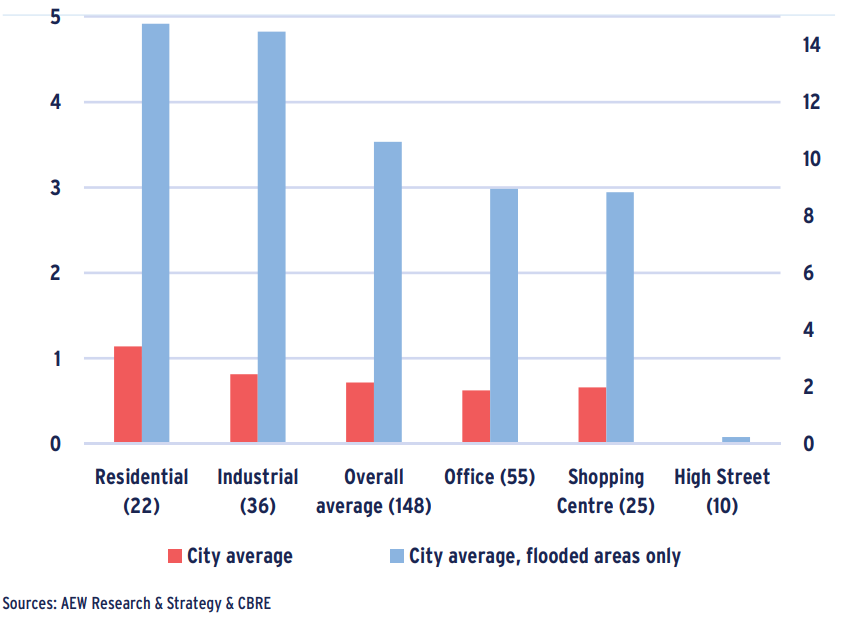

- In our next step, we can now apply the replacement cost to capital value ratio to estimate the expected loss as a basis point share for each of our 148 river flood affected market segments’ prime capital value.

- These estimates show that across all affected market segments that the average annual expected loss is a relative modest 0.7 bps.

- Due to its outsized prime capital values retail records virtually no impact, while residential’s expected loss is highest at 1.1 bps.

- Highlighting the need for active monitoring, it is noted that some individual cities are showing expected losses as high as near 13bps, especially in the residential and industrial sectors.

- Such active monitoring could identify the most affected micro-locations as well. But this goes well beyond our market-level research scope.

- Since only an average of 24% of affected markets’ surface area is projected to flood, an expected loss for flood areas only can be estimated.

- Unsurprisingly, average expected loss in flood areas only is higher at 3.5 bps, with residential and industrial at near 5.0 bps.

Estimated river flood annual expected loss per sector, as bps of prime capital value

FRENCH MARKETS MOST EXPOSED TO RIVER FLOOD RISK

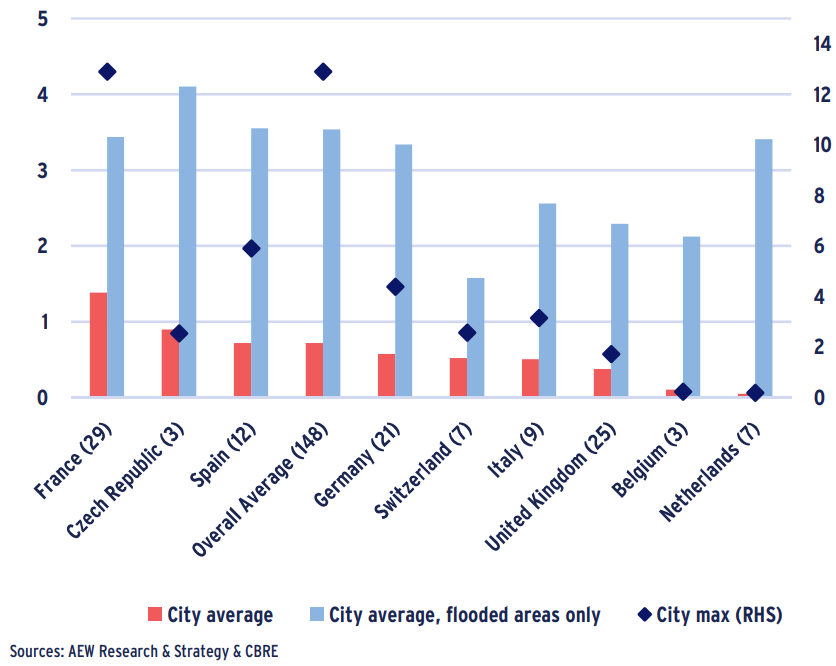

- French markets stand out with significantly higher average expected loss at 1.4 bps when considering the same river flood expected loss data on a country level.

- France records double the overall 0.7 bps 20-country European average. This is due to the many Paris segments affected by river flood.

- France also shows the highest single segment average loss at 13 bps, more than double the next highest for Spain at near 6 bps.

- In contrast, Dutch markets show a surprisingly low average expected loss at 0.2 bps with Germany and UK also below the European average.

- For flooded areas only, the differences in expected losses across countries become less significant.

- Expected loss for flooded areas only for Dutch markets is estimated at 3.4 bps, close to the European average of 3.5 bps and not that far from Czech Republic with the highest average expected loss of 4.1 bps. Switzerland with 1.6 bps is the only outlier in that respect.

Estimated river flood annual expected loss per country, as bps of prime capital value

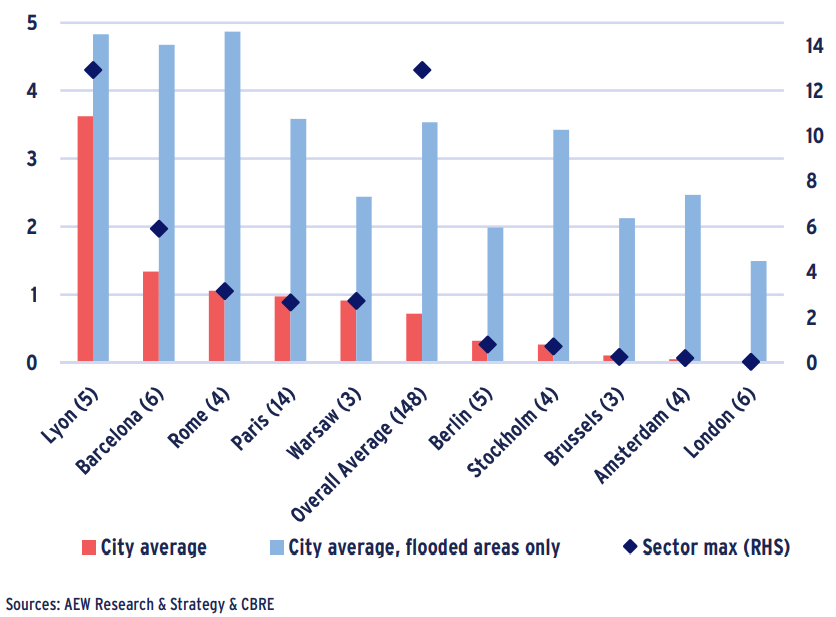

LYON RESIDENTIAL HAS HIGHEST RIVER FLOOD RISK

- Among our 50 covered cities, Lyon is the most affected with an average expected loss of 3.6 bps across its five property type segments.

- This is more than five times the 0.7 bps European average.

- But the high Lyon average is mostly due to a single sector -- Lyon residential -- with a near 13 bps expected loss.

- In that respect, other outliers can also be identified as Silesia industrial at near 12 bps (not shown) and Barcelona shopping centers at 6 bps.

- When we switch again to flooded areas only, with a 4.8 bps expected loss Lyon stands out less from other markets, like Rome and Barcelona.

- This is explained by the fact that 95% of the Lyon residential market segment’s surface is located in the highest zone 100 with a 1% annual chance flood event.

- It is unclear from our data whether investors are in fact actively monitoring and pricing these risks in for the most affected market segments, whether flooded area only or overall. If they are not, we think they should.

Estimated river flood annual expected loss for selected cities, as bps of prime capital value

AVERAGE SEA LEVEL RISE LOSS AT TWICE RIVER FLOOD #

- When we turn to sea level rise, limited data on depth, defenses or loss forces us to use of river flood data to estimate sea level rise loss.

- We apply European sector specific losses – for flooded areas only – such as for high street (0.1 bps), industrial (4.8 bps) and residential (4.9 bps).

- High precision data on underlying surface areas affected by sea level rise is applied for each of the 47 affected segments for our estimate.

- On average 37% of the underlying areas is flooded for markets affected by sea level rise compared to 24% for river flood affected segments.

- Next, we assume that expected loss of river flood is similar to sea level rise, for flooded areas since the damage comes from water in both cases.

- This pragmatic approach is not endorsed by either Munich Re or TCC but allows an in-house estimate that can later be refined with better data.

- The average expected annual loss for sea level rise is estimated at an average 1.3 bps across affected 47 markets based on this approach.

- This is nearly double the average river flood risk of 0.7 bps for the 148 market segments affected.

Estimated sea level rise annual expected loss per sector, as bps of prime capital value

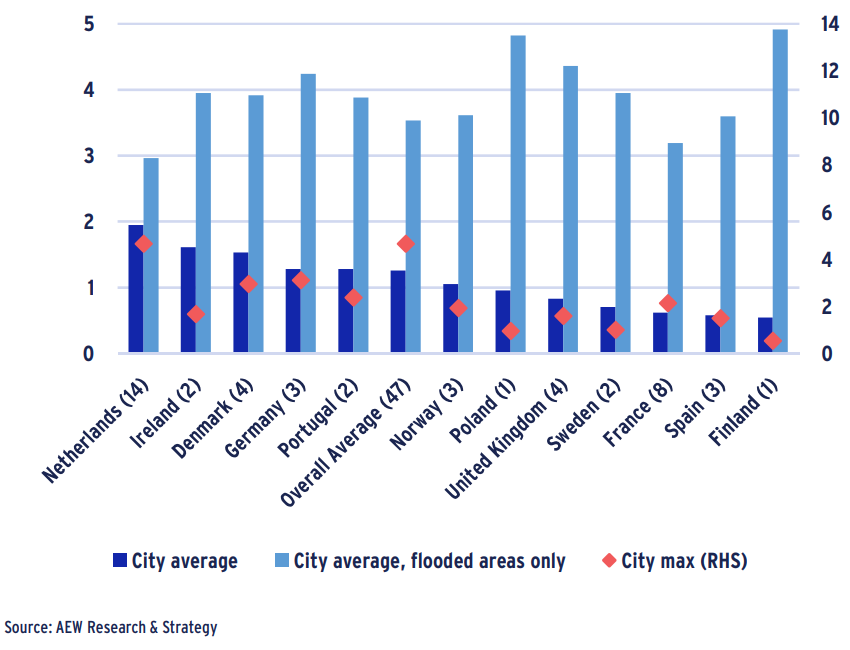

NETHERLANDS MOST EXPOSED TO SEA LEVEL RISE

- Dutch markets are most vulnerable to sea level rise as they have the highest proportion of their market segments in the sea flooding zones.

- Sea level rise-related average expected loss for the Dutch markets is estimated at 1.9 bps per annum, about 50% above the European average.

- Dutch markets also harbour the maximum individual market segments expected loss at 4.7 bps. This can be partly explained as we have no current or future data on defences, which can limit the impact.

- However, the lack of more extreme single segment outliers (like Lyon residential in the case of river flood) are driven by our estimation approach as we apply European-wide property type averages to each affected city segment.

- Sea level rise expected losses are also estimated to be above the 1.3 bps average expect loss for Ireland, Denmark, Germany, and Portugal.

- Other countries with a high number of affected markets to sea level rise such as the UK and France show below average values of expected loss at 0.8 and 0.6, respectively.

Estimated sea level rise annual expected loss per country, as bps of prime capital value

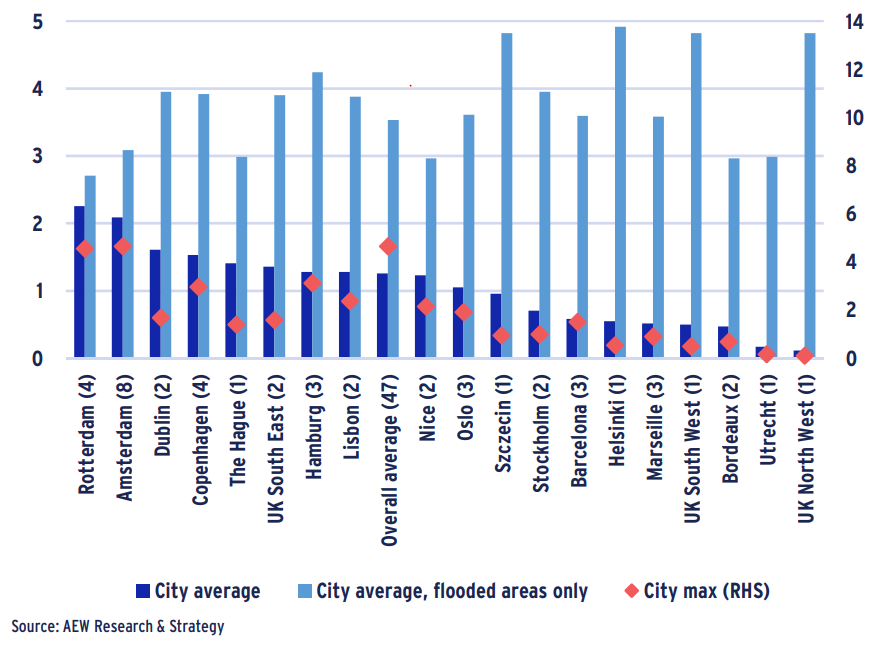

AMSTERDAM AND ROTTERDAM HIGHEST SEA LEVEL RISKS

- Based on our estimates, the Dutch cities of Rotterdam, Amsterdam and The Hague are within top-5 most exposed to sea level rise cities with city averages of expected loss varying between 1.4bps and 2.2bps.

- Like with river flood risk, these city averages are skewed to some degree by a single sector, which in this case is consistently industrial.

- For Rotterdam and Amsterdam industrial market segments, the surface area projected to get flooded is 95% and 97%, respectively. This is very similar to the Lyon residential segment for river flood, which showed a expected loss for river flood of 13 bps.

- Again we need to emphasise, that our sector maximum values of expected loss for sea level rise within cities are significantly closer to city averages compared to river flood losses due to our approach in estimating sea level losses by using European-wide property type averages to estimate each affected city segment.

- It should be recognised that our analytical approach disregards the many significant differences between river flood and sea level rise.

Estimated sea level rise annual expected loss per city, as bps of prime capital value

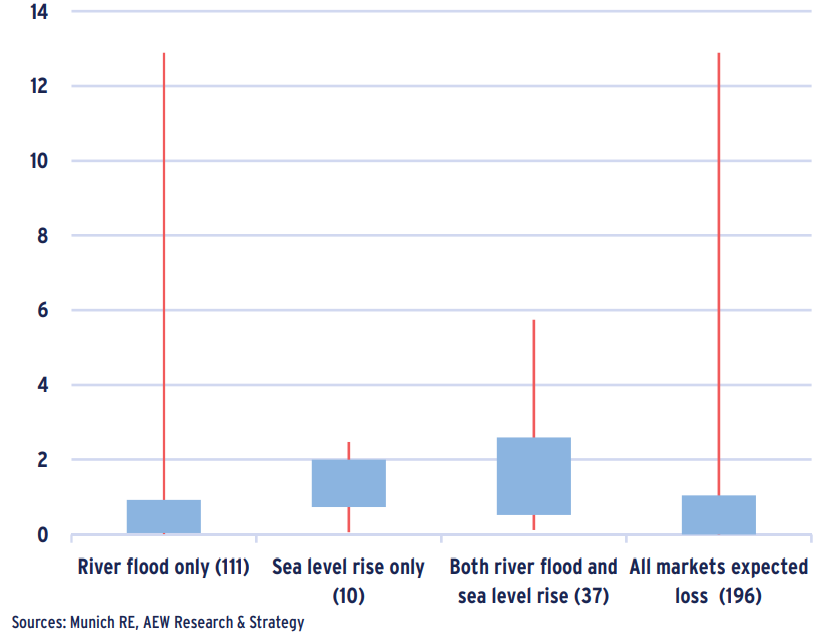

COMBINED AVERAGE WATER-RELATED RISK BELOW 2 BPS PA

- In our final step on water-related climate hazards, we combine the estimated expected losses for both river flood and sea level rise.

- Our graph illustrates the min, max, and quartile borders of expected loss estimates for the various groups of affected market segments.

- Across our entire 196 market coverage, the average and median combined water-related expected loss is a very modest 0.8 bps and 0.1 bps, respectively. This is due to 38 of 196 segments having no exposure.

- As before, our average results hide some interesting outliers discussed before, while many of the remaining values are centered near or at zero.

- The fact that only 24% of markets are exposed to sea level rise risk and 76% of markets is affected by river flood risk drives these results.

- Even combining both river flood (RF) and sea level rise (SLR) expected losses together for the 37 market segments that are exposed to both risks results shows modest average and median loss at 1.7 bps and 1.1 bps.

- Again, the impact of specific market outliers is something to look for in setting up a proper monitoring across portfolios.

Variation in combined expected loss in affected markets, bps of prime capital value

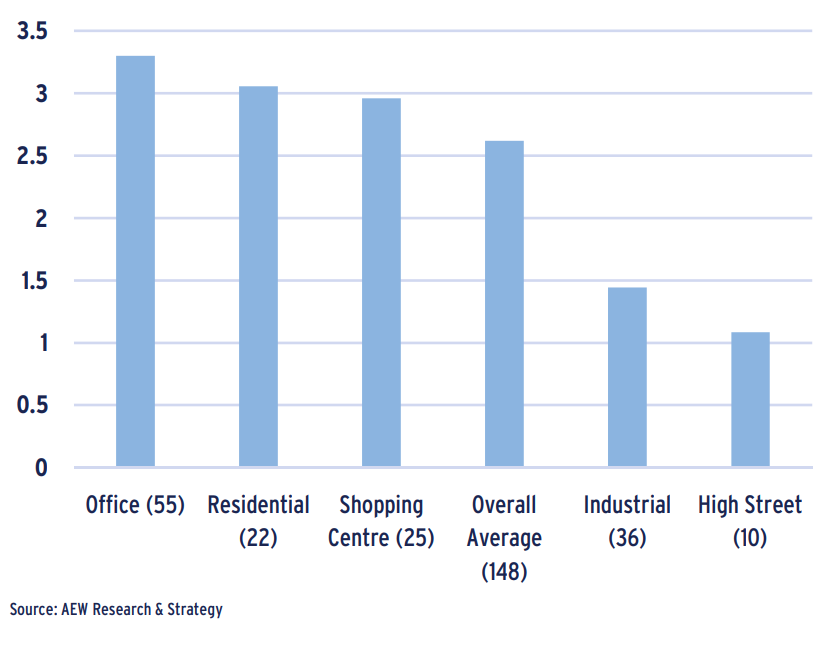

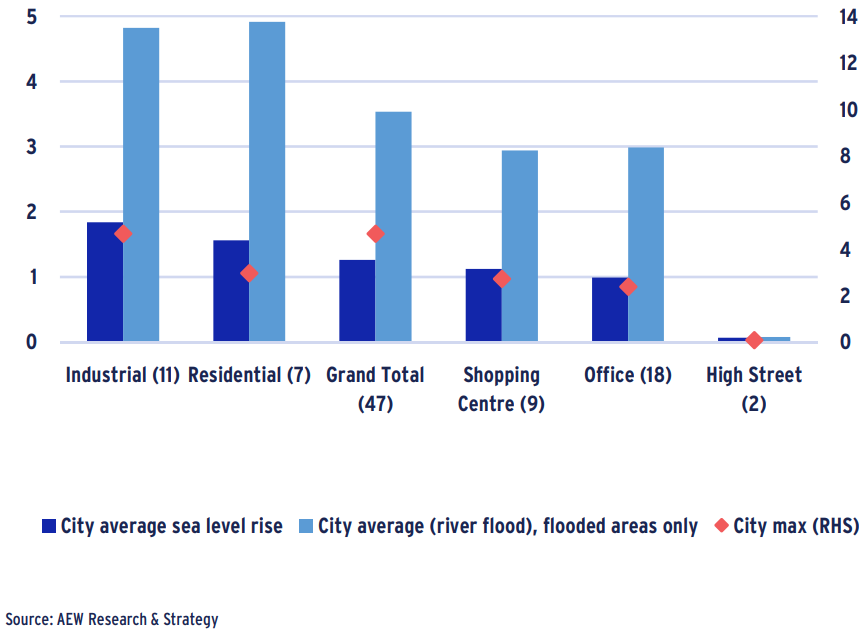

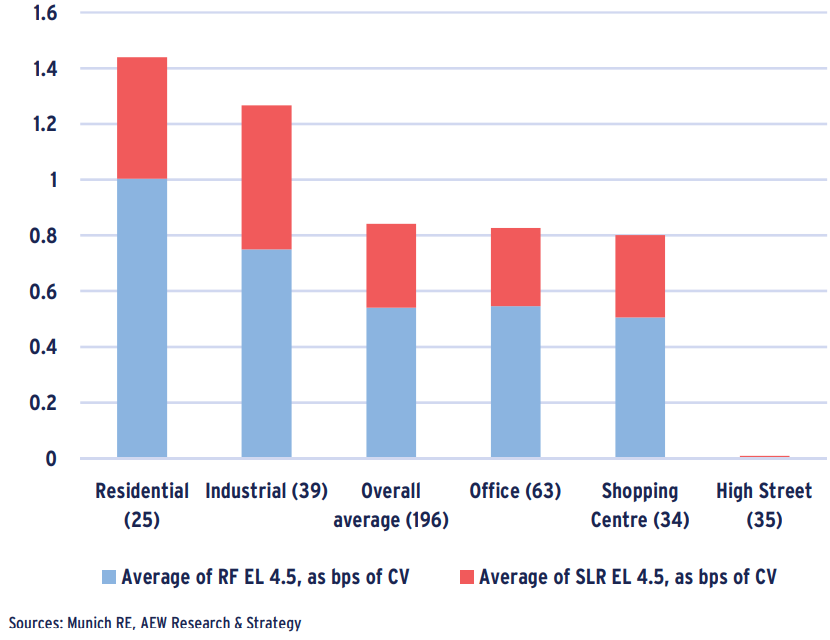

RESIDENTIAL AND INDUSTRIAL LEAST RESISTANT

- Grouping our results by sector indicates that industrial and residential markets have the highest average expected loss at 1.3 bps an 1.4bps, respectively.

- Both of these sectors are vulnerable due to the relatively high proportion of the replacement cost as percentage of prime capital values.

- Many industrial market segments are also located in costal areas near sea ports, which increases their exposure to sea level rise risk.

- High street retail has the lowest average estimated value of expected loss at 0.01bps, which is primarily the result of replacement cost being extremely low relative to the prime high street retail capital values.

- Estimates for shopping centres and offices are very close to the overall average and both stand at near 0.8bps.

- Please note that combining sea level rise (SLR) and river flood (RF) risks does not mean that these risks always occur at the same time, as each risk’s frequency and severity will differ widely.

River flood and sea level rise annual expected loss per sector in RCP 4.5 2050, bps of prime capital value

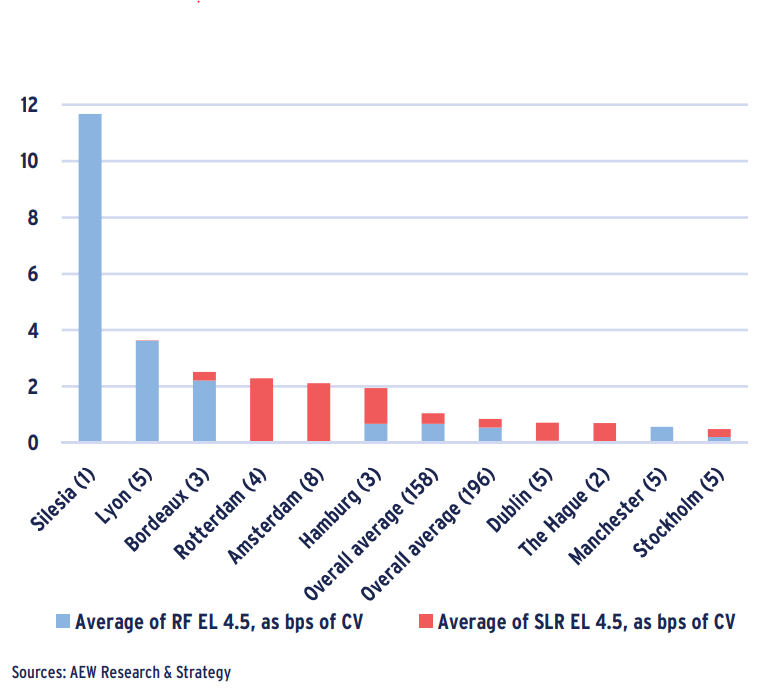

BORDEAUX AND HAMBURG ADDED TO TOP RISK MARKETS

- Our combined expected loss premium per city show some new cities emerging in our top five.

- As before, Silesia industrial has the highest estimate of expected loss from river flood at near 12 bps per annum. Also, Lyon is the second largely affected city, as big proportions of its prime property markets are sitting at the junction of the Rhône and Saône rivers

- However, cities not previously showing in our top risk markets that now make an appearance when considering the combined risk are the in-land seaports of Bordeaux and Hamburg.

- As mentioned before, Rotterdam and Amsterdam, are only exposed to the sea level rise risks and not river flood risk.

- Across the 158 affected markets that are exposed to either river flood, sea level rise, or both our estimated expected loss is 1.1 bps.

- Once we the add 38 non-affected market segments the average comes down to 0.8 bps.

Estimated sea level rise annual expected loss per city, as bps of prime capital value

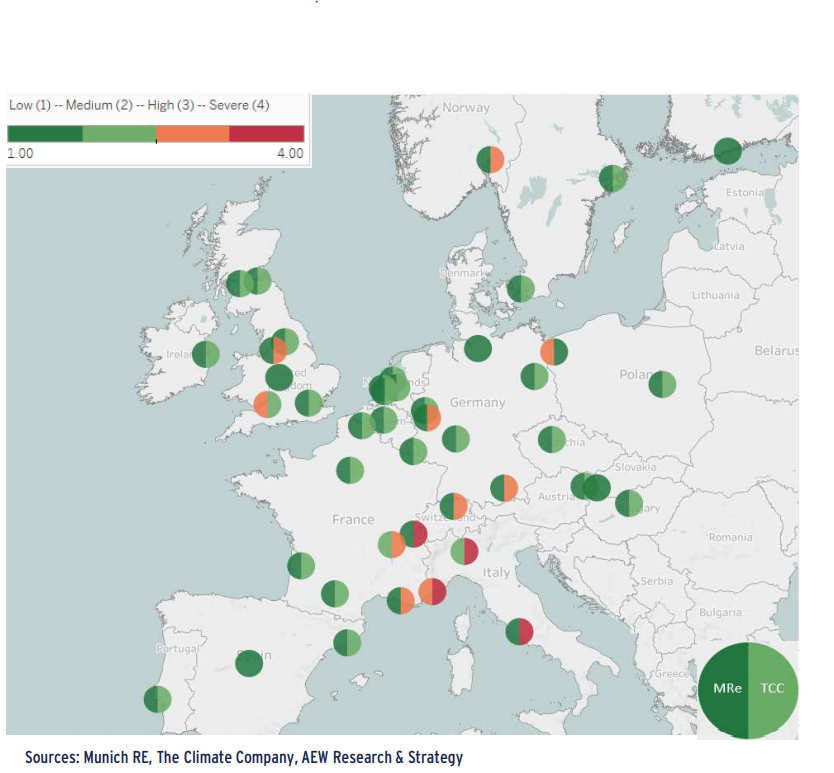

INCONSISTENCIES TRIGGERED BY ANALYTICAL APPROACH

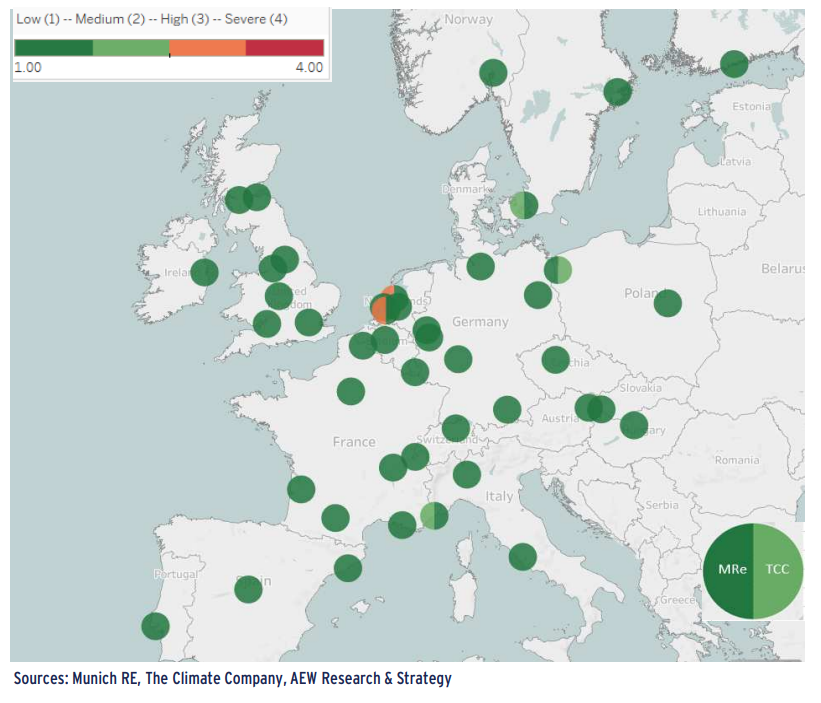

- Where we have data from both our two data partners – Munich Re and The Climate Company (TCC) we do a comparison. TCC includes urban run-off flood risk on mineralized soils in their estimate.

- In general this highlights that for a given climate hazard, the risk assessment can lead to different conclusions for the same market

- As discussed before, river flood risk is affecting 148 market segments across Europe according to Munich Re with no clear geographic pattern.

- But, the average risk score across markets is lower for Munich Re than TCC. This could be mostly explained by the sampling and area definitions, given the importance of elevation in the estimation of this hazard. TCC uses a single location while Munich Re calculates an areabased average. Time horizons also differ by 10 years between the two providers (2040 for TCC, 2050 for Munich Re).

- Major inconsistencies are concentrated in a handful of segments in the flowing markets across Europe: Szczecin, Bristol, Geneva, Frankfurt, Rome, Milan, Nice, Barcelona, Lyon and Warsaw.

River flood risk : comparison between Munich Re & The Climate Company

MORE LIMITED INCONSISTENCIES FOR SEA LEVEL RISE

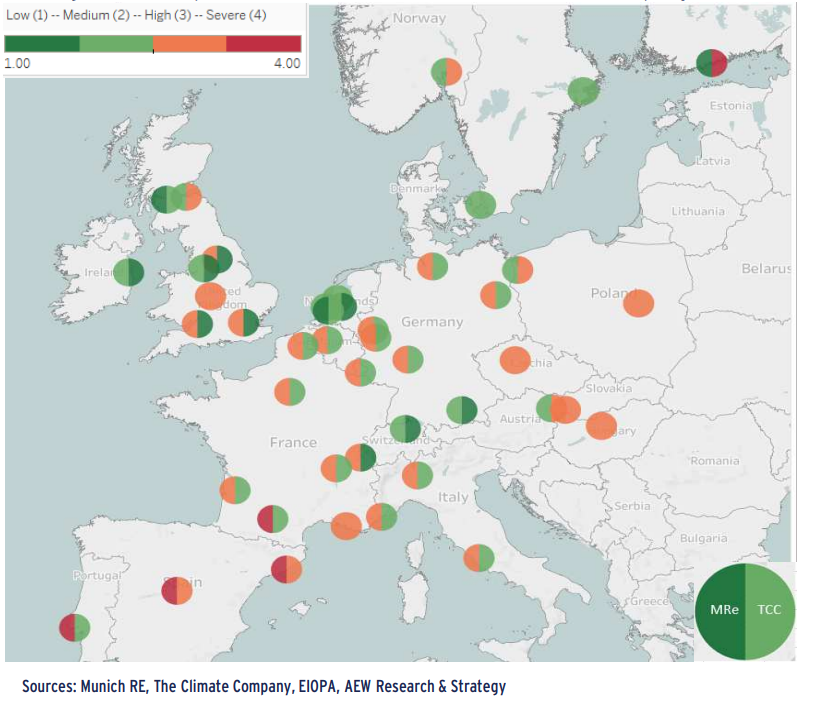

- Inconsistencies are more pronounced with sea level rise (Munich Re) or marine submersion (TCC) risk as our source show big differences in the number of affected markets - 47 markets based on Munich Re data (24%) but just 9 markets according to TCC (5%).

- Overall, the risk of marine submersion is deemed low in the majority of markets along the coast except in the Netherlands. The markets the most at risk are Amsterdam, Rotterdam, Barcelona, Szczecin, Copenhagen and Hamburg according to both providers, with limited differences across property types.

- Despite their smaller number of affected markets, the average risk score of TCC affected markets is significantly higher than Munich Re.

- The additional 10 markets considered at risk by Munich Re can be partly explained by differences in time horizons, which differ by a very long 60 years (2040 for TCC, 2100 for Munich Re).

- Inconsistencies in the results might also be explained by the difference in taking into account existing and/or future sea defences.

Sea level rise risk: comparison between Munich Re & The Climate Company

DATA STANDARDISATION REQUIRED ON PHYSICAL RISKS

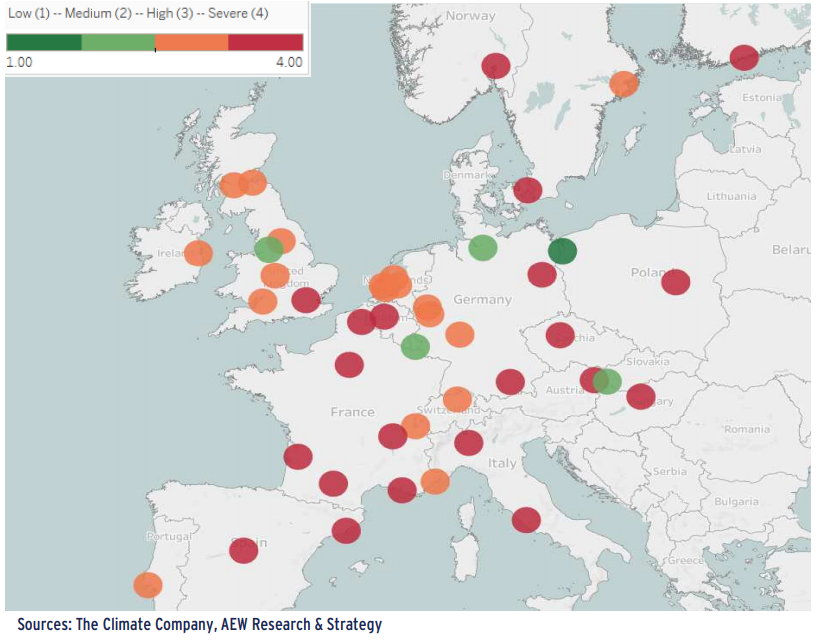

- Finally, drought risk is affecting a very large number of markets across Europe (84% of markets in case of TCC, 95% in the case of Munich Re).

- As expected, the most affected markets are located in Southern and Eastern Europe, in particular Madrid and Barcelona, with limited differences across property types.

- Compared to the water-related hazards, the inconsistencies in drought risk between Munich Re and TCC are more limited, except for Helsinki.

- There the risk score is significantly higher based on TCC compared to Munich Re as the methodologies focus more on the change over time than on current levels. Other markets with high inconsistencies include Bristol, Geneva, Leeds, Zurich, Oslo, London and Toulouse.

- Our results are consistent with the EIOPA May 2022 report on European insurer exposure to physical climate change risk, “Climate change related risks are long-term risks for which a standardized methodology for assessment is not yet widely and fully developed. The complexity and uncertainty in terms of time horizons and potential future pathway and developments make it difficult to precisely assess and quantify them”

Drought risk: comparison between Munich Re & The Climate Company

SECTION 5 : INITIAL LOOK AT URBAN HEAT ISLAND RISK

URBAN HEAT ISLAND RISK MOST COMMON RISK IN EUROPE

- Urban Heat Islands (UHI) occur when a city experiences much warmer temperatures (up to 12°C) than surrounding areas as a result of urbanisation, waste heat emissions and air pollution.

- UHIs have a significant impact on human health and buildings’ energy consumption (increase in the use of air conditioning), exacerbating heatwaves. UHIs can also lead to power and IT breakdowns as well as travel disruptions.

- UHI is a common physical risk hazards in European cities. Almost 60% of the markets covered were subject to high or severe UHI effects, including in Northern Europe, with only 12% of markets with a low risk score.

- According to TCC, the most affected property types are prime office and residential areas due to their central, urban locations.

- The most affected markets are Rome, Paris CBD, Barcelona, Toulouse, Munich, Milan, Madrid and Berlin, but also Oslo and Copenhagen.

- The least affected markets are logistics and residential out-of-town markets, with lower urban density, as well as UK markets.

Urban Heat Island Risk across 196 markets in 2040

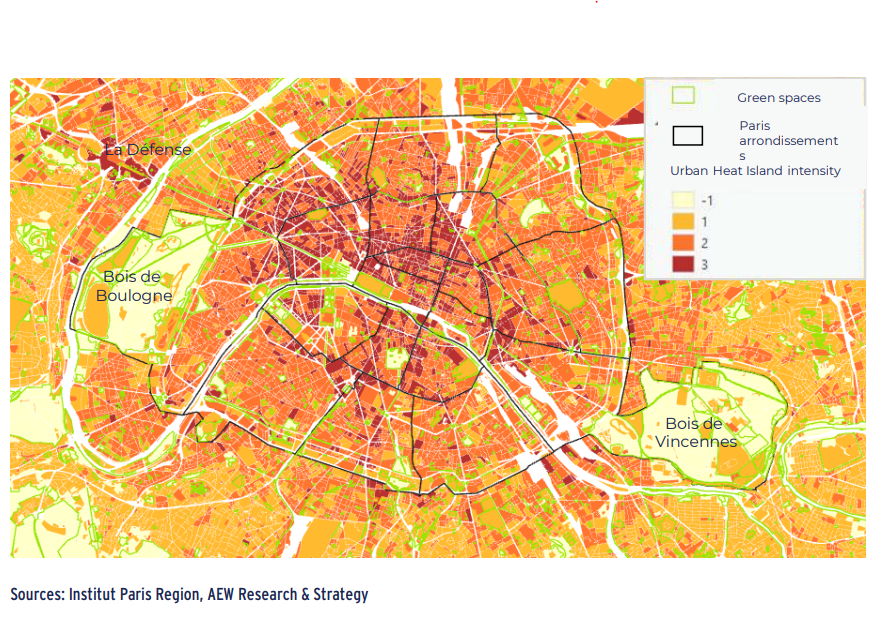

URBANISATION AND LAND COVER ALSO MATTER

- Urban Heat Islands (UHI) are not uniformly distributed across a city, as they depend on the urban and building design and construction materials used, as illustrated by the map on the right of Paris. For these reasons, central, dense areas of Paris are more subject to UHI.

- Air pollution and UHIs also intensify each other.

- Mitigation factors include green spaces and tree coverage, which cool down temperature by providing shade and water evaporation (see the limited UHI effect in parks).

- Painting roofs white to increase the albedo also mitigate UHI effects

Urban Heat Island hazard in Paris

URBAN HEAT ISLAND LINKED TO TEMPERATURE VARIABLES

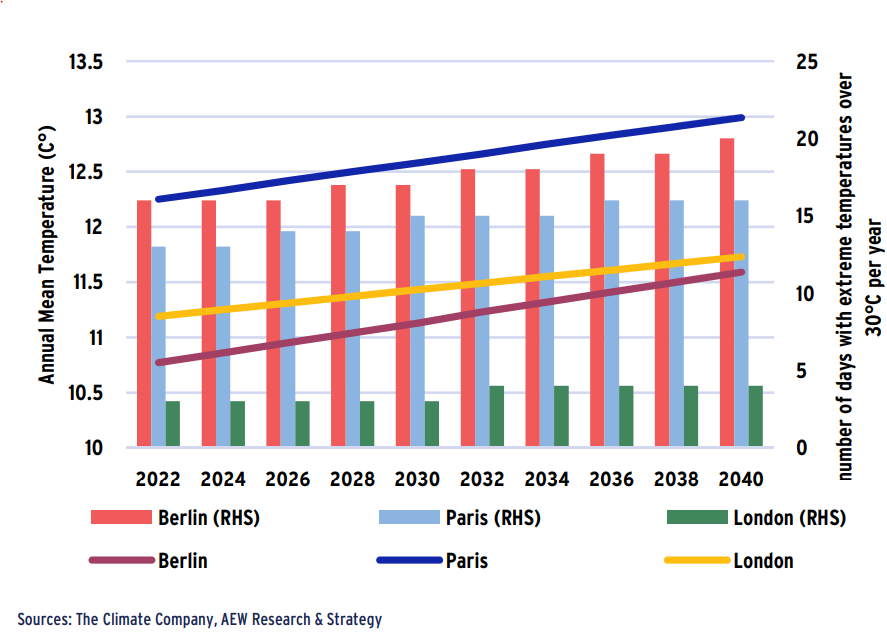

- In addition to the degree of urbanization, The Climate Company estimates the vulnerability to Urban Heat Islands based on 2 temperature variables: Temperature Trend (annual mean temperature) and Thermal Stress (number of days with extreme temperatures over 30°C per year).

- Based on the trend to 2040 (in a RCP 8.5 scenario), a risk score is derived for a specific location. Both annual mean temperature and the number of days with extreme temperature are expected to increase significantly.

- London is expected to experience an increase in the annual number of days over 30 C° from 3 days in 2022 to 4 days in 2040. While this appears limited in absolute terms, this represents a 33% increase.

- After the record drought recorded in the summer of 2022, its is important to accept that long term projections remain uncertain with high interannual variability.

- This means that from one year to the next, it is possible to find values above and below the projections

- The average mean temperature is forecast to increase by 8% in Berlin over the same period. Berlin’s more continental weather means that the city’s annual mean temperature is lower than Paris and London (as cold winter temperature offset warm summer), but the city is more exposed to extreme temperature than Paris and London.

Temperature Trend (annual mean temperature) and Thermal Stress (number of days with extreme temperatures) by city – 2020-2040

This material is intended for information purposes only and does not constitute investment advice or a recommendation. The information and opinions contained in the material have been compiled or arrived at based upon information obtained from sources believed to be reliable, but we do not guarantee its accuracy, completeness or fairness. Opinions expressed reflect prevailing market conditions and are subject to change. Neither this material, nor any of its contents, may be used for any purpose without the consent and knowledge of AEW.