EUROPEAN REAL ESTATE DEBT MARKETS RE-ALIGN

- 5-year swap rates have pushed all-in real estate interest rates to over 4%, their highest levels since 2013. This has been triggered by record high inflation, central bank rate hikes, and uncertainty on the macroeconomic outlook.

- In contrast to these dramatic moves in rates, traditional sector-level loan-to-value (“LTV”) ratios show stable levels and do not signal any major systemic market-wide risk.

- Our updated in-house granular loan data shows not only higher all-in rates for the post-pandemic era, but also continued modest LTV levels. This is consistent across all property sectors and the big German and French markets as well.

- Green Street data on REITs’ traditional secured borrowing costs shows a similar trend to our in-house AEW all-in interest costs estimates. Both confirm the impact of the increased 5-year swaps rates, initial Covid lockdowns and the Ukraine war.

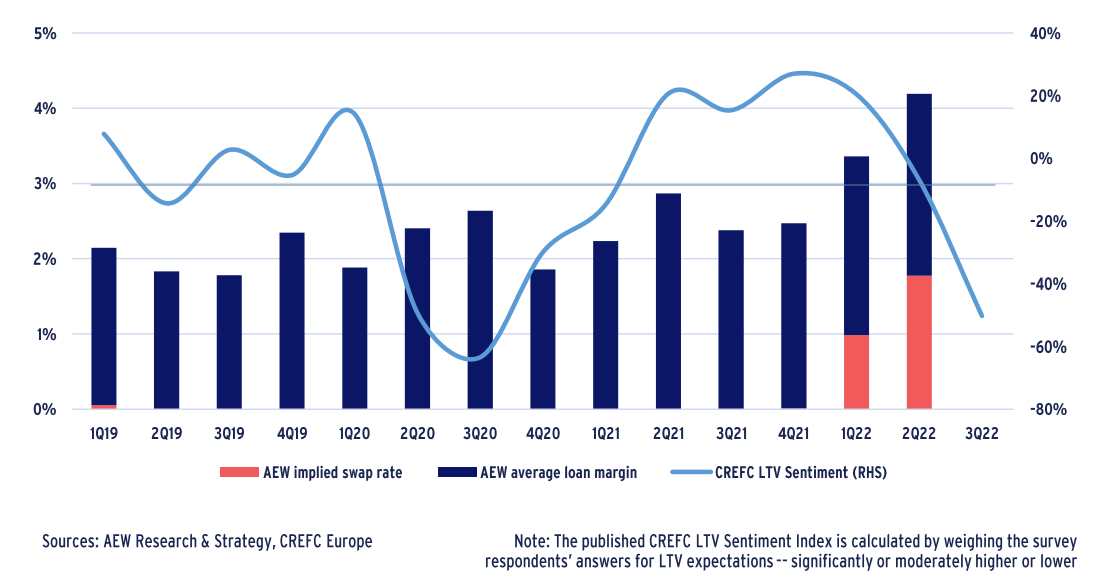

- Chatham Financial data shows that loan margins remain stable. Loan margins from our in-house database are more volatile with their biggest spike in Q2 2021. This might be a result of the second Covid lockdowns and limited in-house data.

- From CREFC’s sentiment survey we note a delayed impact from expected LTVs on the actual recorded loan LTVs in our in-house data. The most recent 3Q22 decline in LTV sentiment is likely to trigger a decline in actual LTVs in the rest of 2022 to 45-50%.

- This potential of lower refinancing LTVs together with the already accumulated capital value declines for some of the underlying collateral amplified by the higher interest rates might trigger significant refinancing problems for loan maturities in 2023-25.

- In the first instance, we estimate the extent of the refinancing challenges by estimating the debt funding gap. This is defined as the gap to be bridged between the original debt amount due at loan maturity and the new debt available to repay it.

- Our initial estimates show that across the UK, France, and Germany there could be a cumulative EUR 24 bn debt funding gap for the next three years.

- Based on the experience from the global financial crisis, this relatively modest gap will likely be bridged by a combination of equity top-ups, junior debt plugs, senior loan extensions & restructurings, loan write-downs, and discounted loan sales.

All-in interest rates vs. CREFC LTV sentiment change

2021 AVERAGE ACQUISITION LTV MODERATE AT 50%

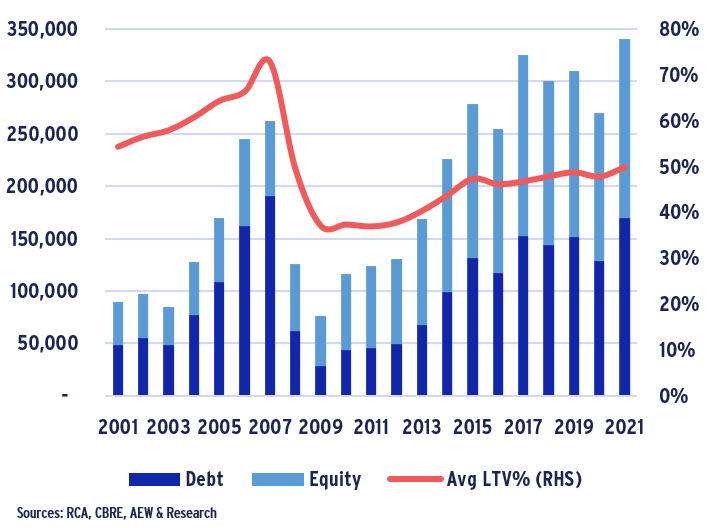

- Based on our latest data and estimates, debt used to fund new acquisitions recovered strongly by 32% from 2020 to €170bn in 2021, a post-GFC record.

- This was due to very strong acquisition activity in the post-Covid rebound as the European investment market posted a record high making up for a lost time during the pandemic.

- Despite these new records, the total amount of debt over acquisition volumes (or LTV) remains at a level just below 50%.

- The 2021 situation should prove less concerning than the pre-GFC €191bn of estimated acquisition debt origination in 2007 at an average of 73% LTV.

- Demand for debt finance was strong in 2021 due to historically low interest rates with many investors locking in low rates as they might have started anticipating increases in 2H 2021.

- Supply of debt from alternative lenders stepped up even if bank lending was still limited by the wide range of regulations, notably tier 1 capital requirements.

Annual loan origination for acquisitions (in EUR mln) with market-wide LTV

REPORTED REIT LTVs EXCEED PRIVATE FUNDS

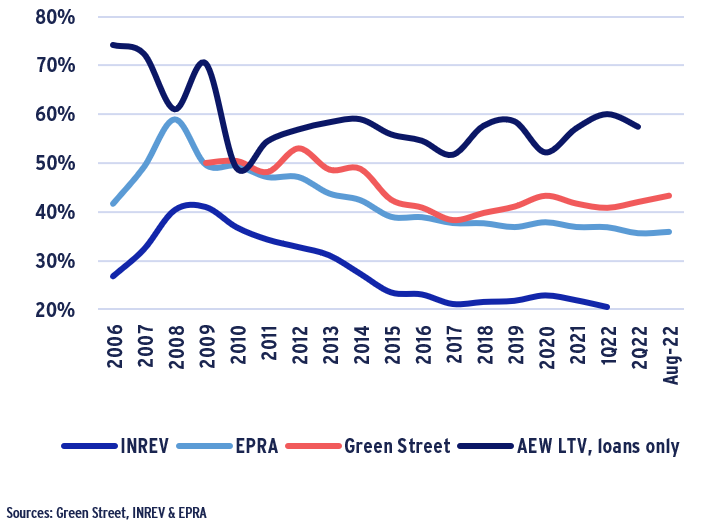

- Based on the latest data, we note good stability in the latest available 2022 EPRA (listed property companies, including REITs) and INREV (private real estate funds) reported loan-to-values (LTVs).

- During 2021 and year-to-date 2022 the reported INREV and EPRA LTVs have decreased by 230 bps and 200 bps, respectively, mostly as a result of increasing capital values.

- However, Green Street data shows a different trend with REIT LTVs in its coverage showing a return to Covid-related highs of 43.3% in 2020, likely due to its more timely adjustment of estimated values compared to the reported EPRA LTV.

- Even with these differences, reported LTVs have remained in a tight range of 40-45% for REITs based on the EPRA data and 20-25% for private real estate funds based on the INREV data.

- In both cases, reported LTVs remain well below 2008-09 record levels, confirming our acquisition LTV data above.

- Finally, we add our in-house AEW loan-level LTV data. Since it shows only the liability side of lending and is therefore higher than the other series. It shows a more volatile trend between 52% and 60% over the last 10 years.

Reported property sector average LTV & AEW LTV for loans only (RHS)

5-YEAR SWAP RATES PUSH ALL-IN RATES UP

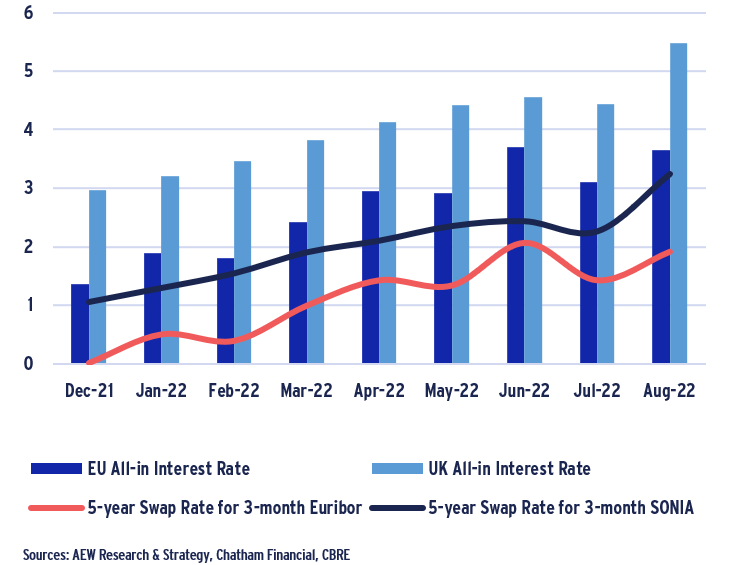

- Given the prolonged elevated levels of inflation, central banks have started increasing their base policy rates in late 2021. This has led to various other rates trending up.

- Since year-end 2021, there has been a significant increase in the 5-year swap rates both for 3-month SONIA (UK) and Euribor at 2.2% and 1.9% , respectively.

- With loan margins also trending up, this has led all-in interest rates to increase by 250-260 bps for both to reach record highs of 5.5% for the UK and 3.7% for Europe.

- These increases will have several consequences in our view:

- Fewer investors will use this more expensive debt in new acquisitions as it is no longer accretive at these levels

- With leveraged buyers priced out, transaction volumes might come down and initial yields are likely to move out

- Refinancing of existing loans at these higher interest rates could pose problems with ICR/DSCR coverage

- Downside pressure on prices could start affecting collateral values and affect lender LTV hurdles for new loans and refinancing

Recent trends in all-in borrowing costs and 5-yar swap rates, UK and Continental Europe (% pa)

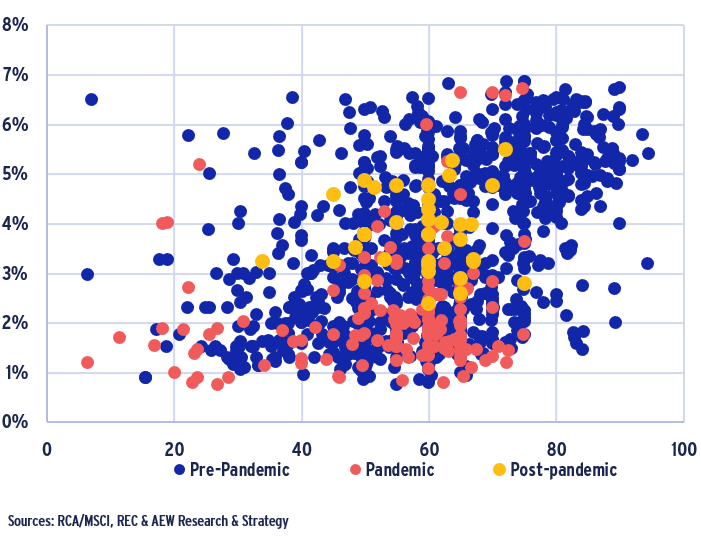

POST-PANDEMIC LOANS AT HIGHER RATES & LOW LTVs

- We updated our granular loan by loan database with another 100 records of loans originated since Aug-21 to bring our data set close to 1,350 loans from our three sources – AEW lending and finance platforms, RCA/MSCI and REC.

- As before, our data goes back to 2003 and we estimate that it covers about 10% of acquisition debt origination since 2010.

- For this and further charts, we define the pre-pandemic era from 2003 to Q1 2020, the pandemic period as Q2 2020 to Q4 2021, and the post-pandemic period as 2022 year-to-date. The post-pandemic period also coincides with the Russian invasion of Ukraine.

- Our scatter chart data shows that post-pandemic loans (yellow) remain in the lower LTV category. But compared to loans originated during the pandemic period (red) show higher interest rates.

- As before, our granular loan level data allows for a more precise interrogation of the impact of external market shocks, like the recent increase in the 5-year swap rates.

- It also allows for some comparisons with new data from other sources, like Green Street and Chatham Financial.

All-in interest rates and actual LTVs on loan-level 2003-2022

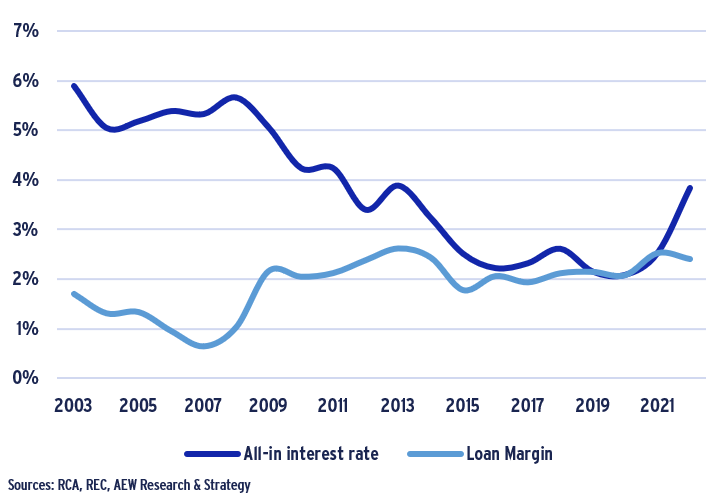

ALL IN RATES AT HIGHEST LEVEL IN 8 YEARS

- Given the extraordinary increase in the five-year swap rates, the all-in interest rates have spiked to 3.8% as of mid-year 2022. This is the highest level since 2013.

- Based on our granular loan-by-loan data, margins showed a small reduction from 270 bps in 2021 to 240 bps for the 2022 year-to-date average.

- The average 1.1% increase in all-in interest rates from 2021 to 2022 has made debt non-accretive for most leveraged equity investors.

- It seems reasonable to assume that most leveraged investors will abstain from further acquisitions as prime property yields have not widened as much as all-in debt costs – until sufficient property repricing occurs.

- The reduced number of (leveraged) investors active in the market might push acquisition yields even further out.

Average European CRE loan margins & all-in rates

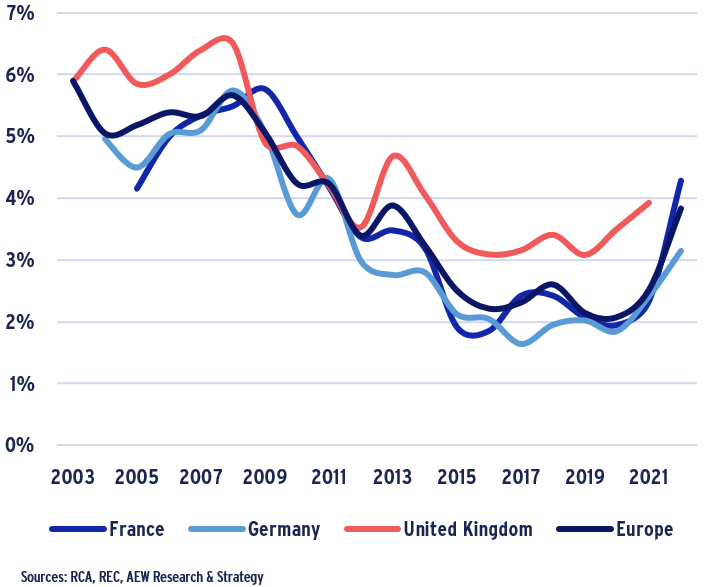

INCREASE IN ALL-IN RATES IN ALL MAJOR MARKETS

- Our granular data confirms the trends shown earlier that European all-in interest rates are consistent across the major national markets.

- French all-in rates have increased by an impressive 200bps since 2021 reaching 4.3%, the highest level in the last 10 years.

- German all-in rates increased by a more modest 70 bps in 2022 from year-end 2021 reaching their highest level since 2012.

- In-house UK loan data does not allow yet to estimate average all-in rates for 2022 as it lacks sufficient qualifying observations. This is driven mostly by our lending business focusing on non-UK markets.

All-in rates per country

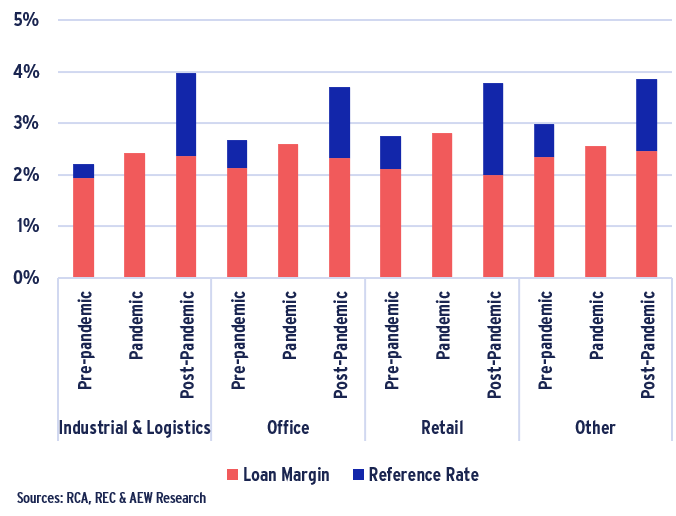

POST-PANDEMIC RATE INCREASE DRIVEN BY SWAP RATES

- Our sector-level breakdown clearly shows the impact of the increase in the 5-year swap rate and its dramatic impact on all-in interest rates across the board.

- As a result, all-in interest rates are at post-GFC record highs across all property sectors in Europe.

- Our data also shows that margins came down a bit in retail and offices during the post-pandemic period (1H 2022).

- At the same time, the highest average margins are recorded for logistics loans as lenders might be concerned about the Amazon announcement in May that they are not taking any further space, an overreaction from our perspective when looking at the European market only.

Loan margin by property type for pre-, post-, and pandemic periods

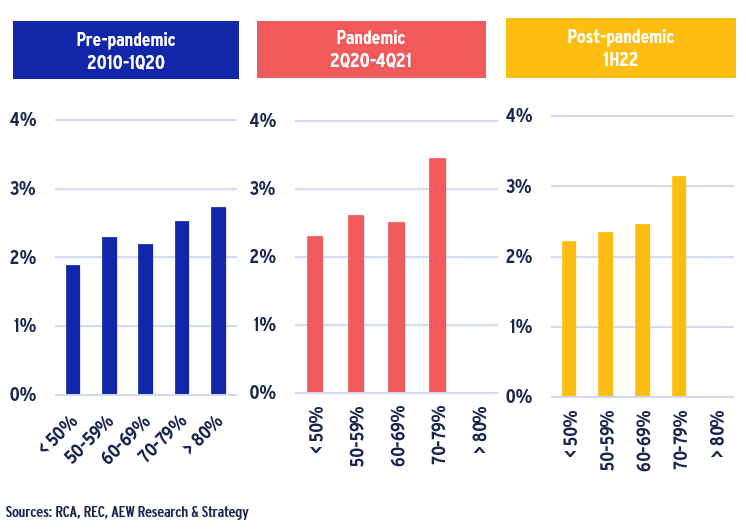

POST-PANDEMIC HIGH LTV LOAN MARGINS REMAIN HIGH

- Based on our most recent data, it is clear that loan margins by LTV loan buckets have not changed significantly from the pandemic period.

- Since the onset of the pandemic, there were no loan recorded with LTVs above 80%.

- Loan margins for loans with LTVs between 70-79% are at 3.1%, 60bps higher relative to the pre-pandemic period.

- On the other hand, loan margins for low risk and below 50% LTV loans remained again mostly flat over the period.

- Both data points are consistent and confirm that in the post-pandemic period, lenders retained their “risk-off” attitude adopted during the pandemic period.

- In the post-pandemic era of increased uncertainty around inflation, base rates and a potential recession, this is a prudent approach.

Loan margin per LTV Bucket for pre- vs post-Covid periods

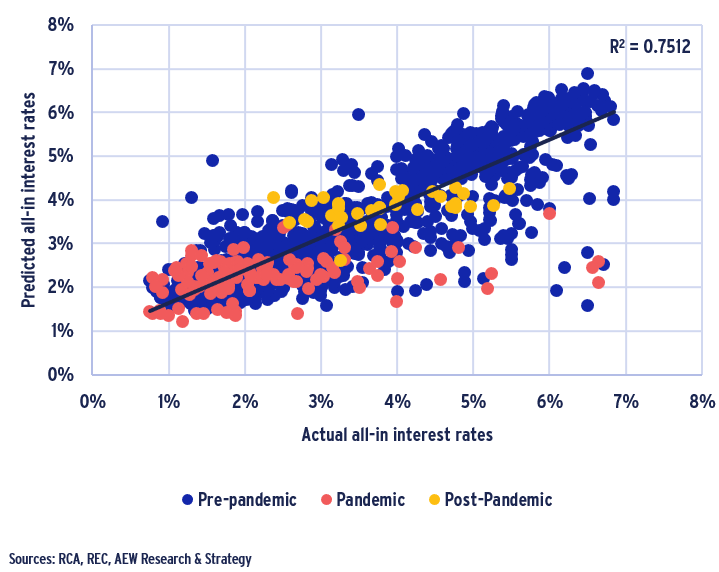

GRANULAR DATA ALLOWS US TO QUANTIFY LOAN PRICING

- As in our previous two reports on the European debt market, we have updated our model which predicts the all-in interest rate based on key loan variables such as the LTV, origination vintage, property sector, and collateral location.

- Compared to our 2020 and 2021 results, it is noted that the explanatory power of our model has maintained an R-squared of 75%.

- The post-pandemic loans in orange show a good model fit and fewer outliers than we saw in the pandemic era (red) and pre-pandemic period (blue).

- It is reassuring to confirm the robustness of our model’s predictive strength despite the post-Covid uncertainty related to geopolitical risks, monetary policy, and macroeconomic uncertainties.

Actual vs. predicted all-in CRE interest rates

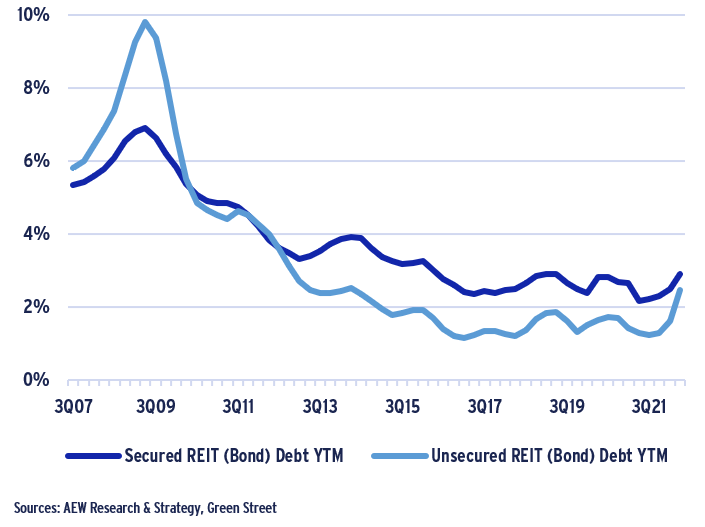

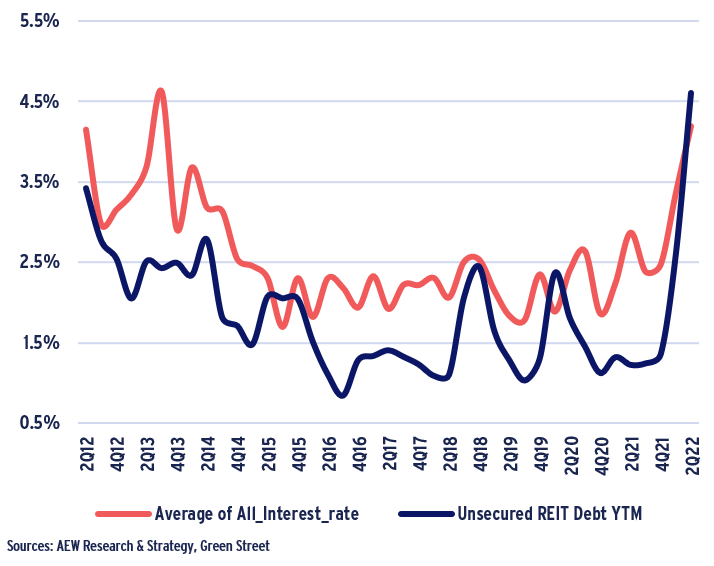

GREEN STREET TRACKS SECURED & UNSECURED YIELDS

- Historical data from Green Street provides an interesting comparison between the costs (as expressed in yield-to-maturity) for two of the main sources of debt used by European and UK REITs.

- The apparent yield advantage for REITs to use unsecured bonds is skewed by the fact that most of the secured REIT bonds are issued in pounds by UK-domiciled REITs where debt yields have been higher.

- In fact, from 2014 until year-end 2021 the average spread between unsecured bonds versus secured bonds was 100-150 bps.

- This can be partially explained by the ECB’s more active quantitative easing (QE) programme relative to the BoE.

- This allowed the ECB to buy REITs’ corporate bonds at issuance and drove both corporate and government bond yields in the Eurozone to historical lows.

- More recently, enduring and record-breaking inflation has forced central banks to raise policy rates and halt or even reverse their QE programs, which has led to bond yields widening out.

Yield to maturity on European REIT debt, 4-qrarter trailing average

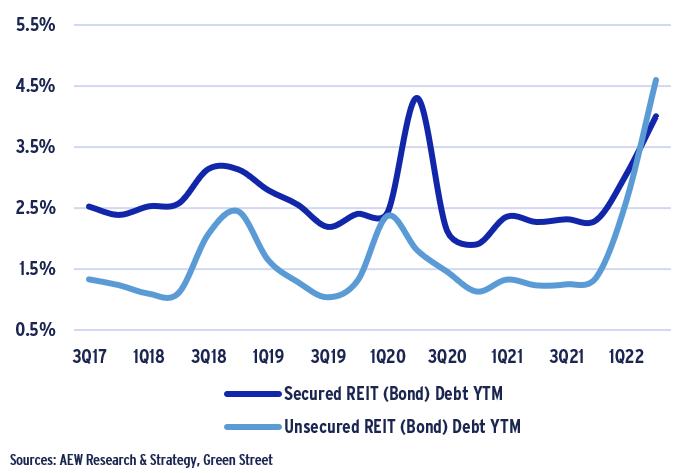

UNSECURED BONDS WIDEN AHEAD OF SECURED YIELDS

- When we consider the most recent quarterly data, it becomes clear that the bond market has responded to the current macro concerns.

- The high degree of correlation between secured and unsecured bond yields is mostly based on Green Street’s methodology, as quarterly yields are based on pricing in the secondary bond market.

- In other words, it’s a spot mark-to-market yield of publicly traded secured and unsecured REIT bond debt. It does not only represent yields on bonds from primary issuance in that quarter.

- Yield widening for unsecured bonds over the last two quarters has pushed their yields above the secured bond yields for the first time in 10 years.

- In a more normally functioning market, where central banks are less active investors, at similar leverage levels we would expect the secured bonds to have lower yields than unsecured bonds as they rank senior in priority of payments.

Yield to maturity on European REIT debt

HIGH CORRELATION BETWEEN PRIVATE AND PUBLIC DEBT

- Green Street’s bond yield data makes it possible for us to compare it to our in-house AEW all-in interest cost data.

- We compare our in-house secured all-in mortgage interest rates to unsecured REIT bond yields.

- In general, we note a high degree of correlation between the two data series, especially in the last six quarters.

- In this case, our in-house AEW all-in interest cost series shows less volatility than the Green Street data.

- Our all-in interest rates confirm the impact of the initial Covid lockdowns in Q2 and Q3 2020 but to a much more moderate degree than the Green Street data, which shows a more immediate response in Q1 2020.

- The Ukraine war impact in Q2 2022 shows a more similar increase between the two sources as it was mostly driven by the 5-year swap rate increase over the period.

- The central banks’ QE policies have kept bond yields lower than secured mortgage loans that were not part of purchasing programmes.

AEW all-in interest rates vs. Green Street unsecured REIT bond YTM

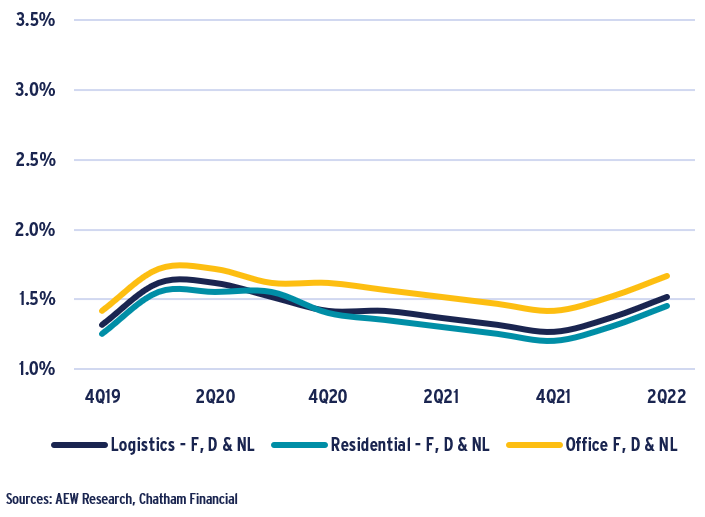

CHATHAM MARGINS SHOW COVID & UKRAINE IMPACTS

- Quarterly historical data from Chatham Financial shows CRE loan margins for Northern European markets (France, Germany & Netherlands) in a tight range between 120 and 170 basis points over the last three years.

- Chatham Financial’s data is based on loan origination records based on its debt and hedging advisory business and filters for senior loans with LTVs at around 50%.

- It is noteworthy to see that office loan margins are consistently 15-20 bps higher than logistics and residential over the period.

- The 30 bps loan margin widening in Q1 2020 shows an immediate impact from the Covid lockdowns across all three sectors.

- After this initial shock, margins settle back down to their pre-Covid Q4 2019 levels over the subsequent two years. §The impact of the Russian invasion of Ukraine in Q1 2022 has triggered a 25 bps loan margin widening across sectors over the last two quarters.

Loan margins for Northern Europe (France, Germany & Netherlands) per property sector

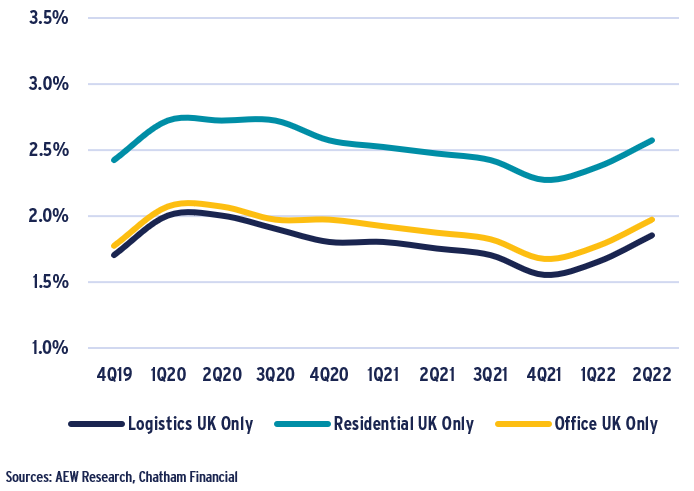

UK LOAN MARGINS HIGHER, ESPECIALLY IN RESIDENTIAL

- When we next consider the quarterly historical data for the UK only, we note a few interesting similarities and differences.

- First, UK margins for office and logistics are 35-40 bps above the Northern European averages. This could be due to higher funding costs for UK banks compared to their European counterparts.

- Second, loan margins for residential projects are more than 100 bps above their Northern European averages, which might be explained by a higher proportion of development loans in the UK sample.

- Similarities between the UK and Northern Europe are evident from the timing of the changes in margins over the available time period as far as the Covid and Ukraine war impacts on margins.

Loan margins for UK only per property sector

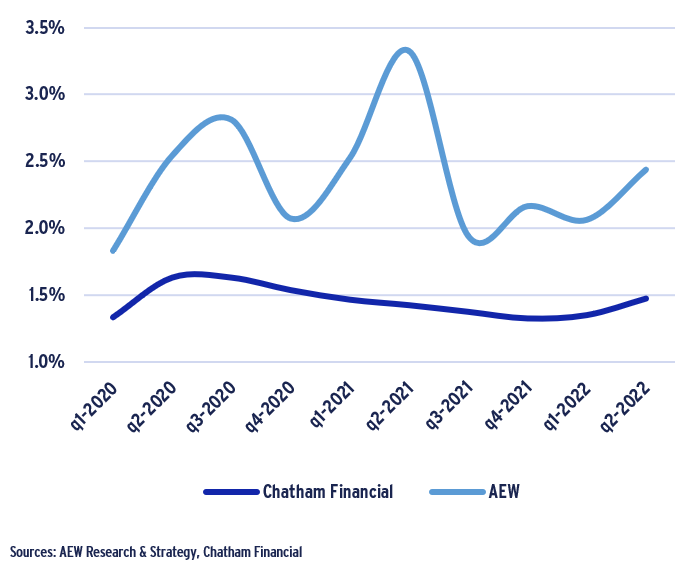

MORE VOLATILITY IN IN-HOUSE DATA

- The Chatham Financial loan margin data allows also a comparison to our in-house AEW loan margin data.

- The best segment for such a comparison is Northern Europe across all sectors where both sources have a sufficient sample size.

- Our AEW loan margin data shows a more volatile and exaggerated pattern than Chatham’s.

- Similar to Chatham, our margins show the impact of the initial Covid lockdowns in Q1 2020 and the Ukraine crisis in Q2 2022.

- However, the biggest spike in AEW margins is shown in Q2 2021, which might be a result of the second Covid lockdowns. Chatham Financial shows a moderating trend and no widening.

- These differences are most probably due to the strength of the underlying datasets. Our AEW data for the subset selected for comparison counts just over 40 loans for the last six quarters.

- Our limited data points are likely to create some noise when compared on a quarterly basis, highlighting the need for an industry-wide loan-by-loan data source to pool these data.

Quarterly average loan margins for All Property Sectors (excl. retail) for Northern Europe (FR, DE & NL)

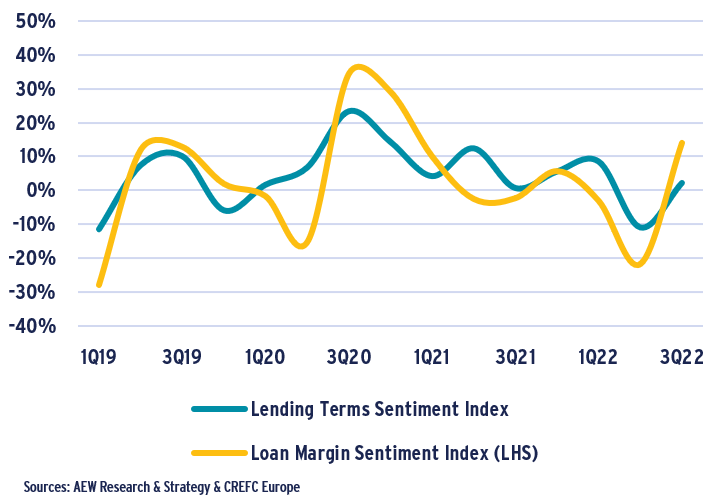

CREFC EUROPE SURVEY SHOWS MARKET SENTIMENT

- Historical trend data from CREFC Europe (the trade association for real estate finance) shows that loan margins were expected to increase as the Covid lockdowns hit in 2Q20.

- Their latest quarterly survey responses show a similar increase in expected loan margins in response to the prolonged Ukraine crisis, record-high inflation, and recent central bank base rate hikes.

- It would be reasonable to expect further margin widening if the macroeconomic outlook continues to worsen, with potential blackouts and rationing in the coming winters.

- When we consider additional data on expected lending terms, we note a very close correlation with the margin outlook. When margins are anticipated to go up, lending terms tighten, to a lesser extent.

- This all makes sense from a survey among 60-80 leading banks, insurers, debt funds, borrowers, and advisors across Europe, including the UK.

- Please note that the published CREFC LTV Sentiment Index is calculated by weighing the survey respondents’ answers for LTV expectations -- significantly or moderately higher or lower.

Loan margin & lending terms sentiment change

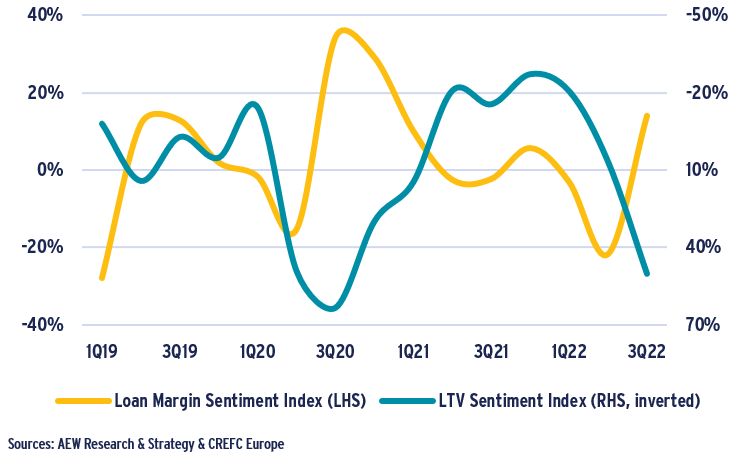

LTV & MARGIN SENTIMENT NEGATIVELY CORRELATED

- This rationality in the European lending market is further confirmed when we compare the same loan margin sentiment data to survey results for where LTVs will be heading.

- Sentiment for LTV and loan margins are negatively correlated, which means when lenders want to become more cautious, LTVs come down and margins go up.

- This was very clearly the response to the Covid lockdowns in Q2 2020, but also more recently in Q3 2022.

- Again, it would be reasonable to expect further margin widening and LTV declines if the ECB will follow the Bank of England in predicting a recession and raise its policy rates further to control inflation.

Loan margin sentiment index vs. LTV sentiment index

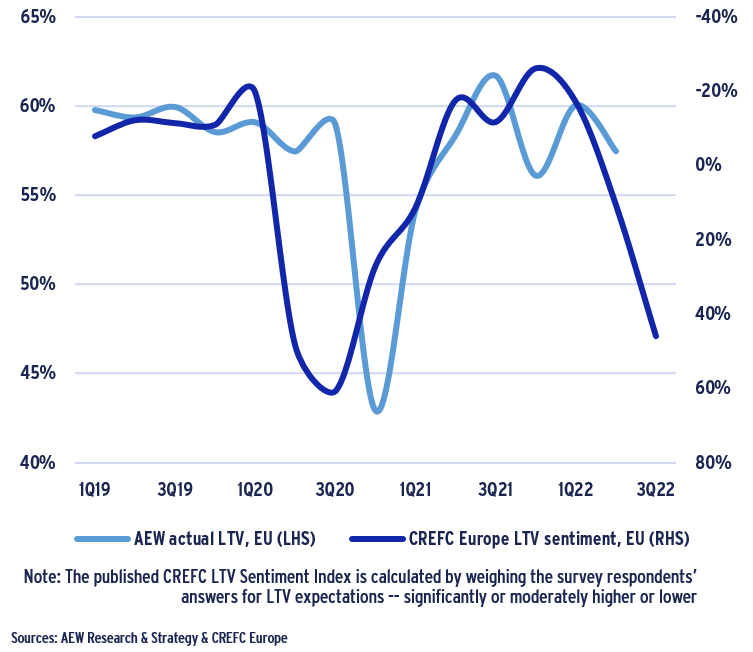

SENTIMENT SIGNALS LTVs TO COME DOWN

- CREFC Europe’s sentiment survey allows us to further analyse our in-house loan-by-loan data for Europe excluding the UK across all property sectors.

- The high degree of correlation between the change in the CREFC LTV sentiment and actual recorded loan LTVs is remarkable.

- The Covid-linked Q2 and Q3 2020 LTV sentiment movement shows a delayed impact in actual LTVs dropping from 60% to 45% in Q4 2020.

- The most recent Ukraine-linked LTV sentiment shift in 3Q22 results (similar to the 2Q20 Covid impact) might trigger a similar decline in actual LTVs in the second half of 2022 to 45-50%.

- If lenders reduce their actual LTVs in line with what the CREFC sentiment survey implies, it could pose significant refinancing problems in future years, with loans maturing in the next three years.

- This is something we have highlighted in our Sep-20 debt market report and can re-visit again today as some banks are no longer active in the current market conditions.

AEW actual LTV vs. CREFC EU LTV sentiment (excl. UK)

COLLATERAL VALUES TO POSE REFINANCING CHALLENGE

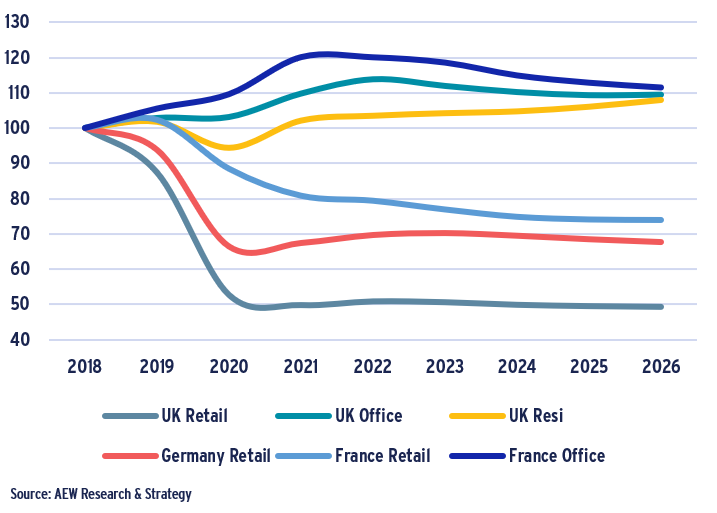

- When considering re-financings of loans maturing in 2023 and after, the first logical step is to consider how the underlying collateral values have evolved since the loan origination.

- Based on previous work, we know that European loan maturities are not standard and range between 3 and 7 years. This allows for the reasonable assumption that the average loan maturity is 5 years.

- Loans maturing in 2023 were, therefore, originated in 2018. Based on this we can evaluate the prime capital values for some of the biggest sectors across the UK, France, and Germany. We stick with these three countries for convenience.

- Unsurprisingly, retail shows the most dramatic decline in values since 2018 with the UK at -50%, Germany at -30%, and France at -23% by 2023. Other sectors are showing various capital value improvements since 2018.

- We include years past 2023 to assess 2019 and 2020 loan vintages as well, which require refinancing in 2024 and 2025, respectively.

Prime capital value of selected European property markets (2018 =100)

RE-FINANCING LTVS TO ADD TO PROBLEM

- Apart from a decline in collateral value, there is also a potential for lenders to not want to refinance at the original loan’s LTV level.

- In fact, the CREFC LTV sentiment results show that (senior) lenders can be expected to reduce their actual LTVs downwards to 45-50%. Therefore, we assume in our analysis a 50% refi LTV.

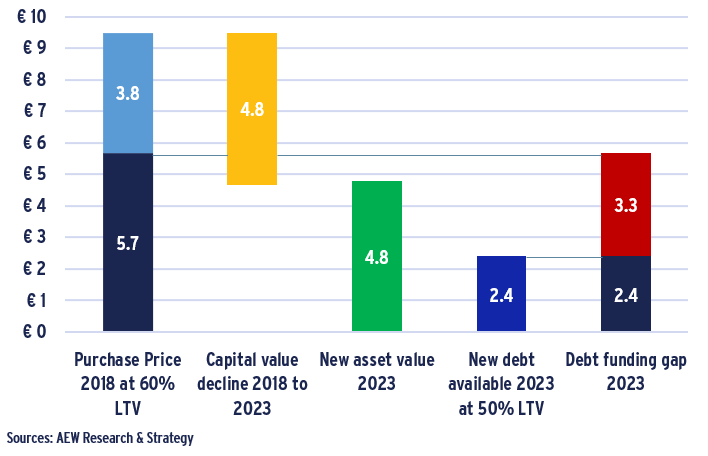

- As an example, we provide our estimate of the debt funding gap (DFG) for all 2018 originated UK loans secured by retail collateral as follows:

–Transaction volumes are adjusted for non-levered deals (17% of 2018 UK retail volume).

–Average LTV for the market in the year 2018 (60% for UK retail according to the in-house data) is assumed at purchase.

–5 year capital value forecast for UK retail shows a -50% decline in value between 2018 and 2023. –New debt volume is estimated at 50% LTV of new value.

–Additional equity (or junior debt) is needed to avoid loan default, we highlight this in red as the debt funding gap.

Step-by-step estimation of the Debt Funding Gap for all 2018 loans secured by UK retail transactions in EUR bn (dark blue = debt, light blue = equity, amber = value decline, green = asset value, red = DFG)

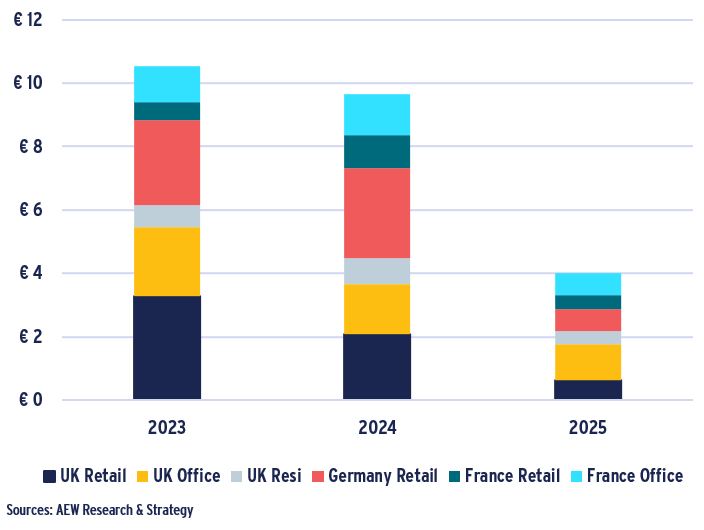

EUR 24 BN DEBT FUNDING GAP QUANTIFIED FOR 2023-25

- Based on the above five-step approach for each of the five segments impacted, we estimate a 24.2 bn EUR in DFG for the next three years.

- Over half of this funding gap is related to UK real estate debt (12.8 bn EUR), followed by Germany (6.2 bn EUR), and France (5.1 bn EUR).

- Across sectors, retail constitutes nearly 60% of the DFG (14.3 bn EUR), followed by office with 8 bn EUR, and residential with 1.9 bn EUR.

- In relative terms, the 24.2 bn EUR debt funding gap represents nearly 9% of the last three years’ historical transaction volumes in the affected market segments.

- Based on our latest estimates, the 2023-2025 UK commercial real estate DFG is around £11bn. This is significantly below our previous Sep-2020 estimate of £30bn. Again, this is much lower than the £70bn witnessed during the aftermath of the Global Financial crisis.

- The reason for the lower DFG in 2023-2025 is mainly because of stricter bank regulations in the aftermath and more conservative acquisition LTVs. In addition, we also expect capital value declines to be less severe compared to the GFC.

Market-wide debt funding gap (DFG) across selected markets in EUR bn

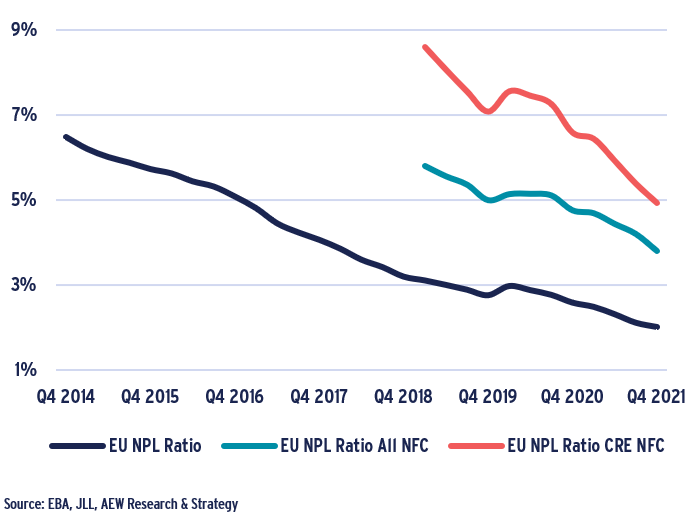

NPL STILL TRENDING DOWN FOR NOW

- With recent rate hikes and the post-Covid economic recovery slowing on the back of the Ukraine conflict, it is appropriate to consider the potential problems with the refinancing of legacy loans.

- To assess the risk of significant distress with traditional real estate lenders, the EBA data on the non-performing loan (NPL) ratio is useful.

- There is a clear consistent decline of overall NPLs across Europe as well as for both non-financial corporate (NFC) and commercial real estate borrowers to levels between 2-5%.

- Of course, this historical NPL data is not forward-looking and does not consider the impact of potential collateral capital value changes for loans maturing in the next few years.

- Regardless of what future NPLs might be coming along, it is good to see that there has been a near resolution of the NPLs created during the GFC.

- It seems banks have the infrastructure in place to deal with the next wave of potential NPLs.

Historical trend of NPL ratio (as % of total loan portfolio)

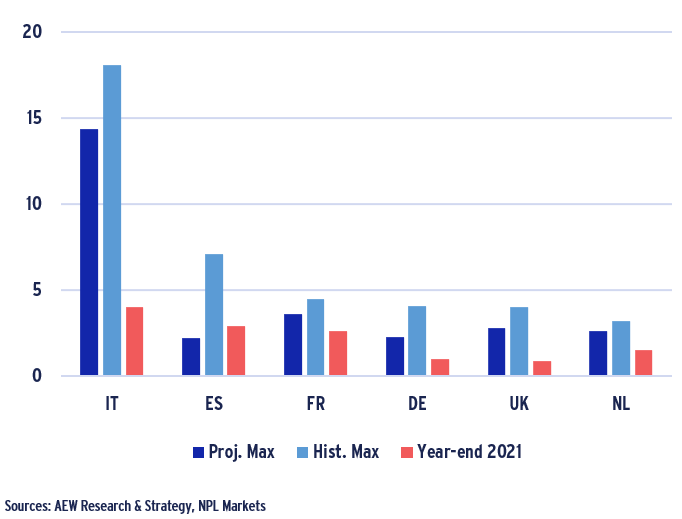

FEARED POST-COVID NPL SPIKE DID NOT YET COME

- As a further check of current distress in real estate lending, we consider national NPL ratios. §Despite the impact of Covid, our six-country average European NPL ratio stood at a near-record low of 2.2% by year-end 2021.

- Previously we had highlighted that Covid could be expected to impact the credit quality of bank loans, including those secured by real estate.

- In their Apr-22 update, advisors NPL Markets estimate that NPL ratios will not come close to exceeding their historical maximums – a reversal from the 2020 estimate.

- Based on this, it seems banks might not yet need to re-start the cycle of increasing reserves, taking write-downs, selling NPL loan portfolios, and re-structuring existing loans.

- But, the NPL Markets projections are not real estate specific. This means that an increase in refinancing problems in real estate could be absorbed as other sectors are not projected to be distressed.

Current European NPL ratios per country compared to historical and projected maximum

BANKS BETTER POSITIONED TO ABSORB LOSSES

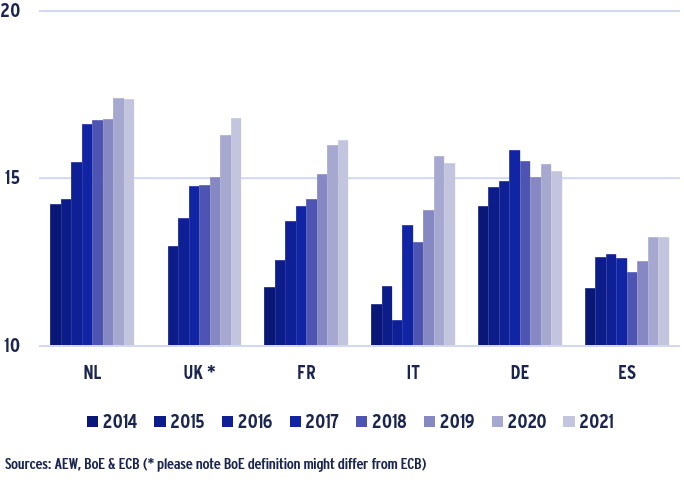

- Finally, it is useful to consider European banks’ position to absorb losses going forward.

- Since 2019, there has been a significant improvement in tier 1 capital ratios across all European banks with the exception of Germany.

- This confirms that banks are now better positioned to absorb losses than before the Covid pandemic.

- Each individual bank’s capital reserves and profitability will impact on the extent and speed in which it can absorb loan write downs or sell NPL portfolios at discounts.

- Given the higher overall tier 1 capital ratios compared to the GFC, it seems reasonable to expect a more pro-active and quicker resolution of non-performing real estate loans.

Banks’ tier 1 capital ratio evolution, selected countries

This material is intended for information purposes only and does not constitute investment advice or a recommendation. The information and opinions contained in the material have been compiled or arrived at based upon information obtained from sources believed to be reliable, but we do not guarantee its accuracy, completeness or fairness. Opinions expressed reflect prevailing market conditions and are subject to change. Neither this material, nor any of its contents, may be used for any purpose without the consent and knowledge of AEW.