- Moderating mortgage rates and a recovery in lending volumes over the past year have supported the recovery in house prices. The ongoing conflict in the Middle East could however lead to an increase in energy prices and force central banks to hike rates to curb inflation. This in turn, could halt the house price recovery and trigger more demand for rental units.

- New supply of housing remains limited and short of government targets despite a recent increase in building permits. In addition, short-term rentals and private landlord sales in some markets have led to a decrease in the private-rented stock despite various attempts at regulating them.

- European prime residential market rents are projected to see 3.2% p.a. growth in 2026-30 in our base case scenario despite tightening rental regulations. With a more uncertain inflation outlook, these forecasts could be revised in the coming quarters.

- Residential investment activity increased modestly year-on-year in 2025 with European volumes totaling €45 bn. With improving financing conditions, liquidity has improved further and led to yield tightening.

- Due to the robust supply-demand dynamics and stable cashflows, investors’ appetite for the different residential sub-segments remains strong. Since 2008, residential has doubled its share in total investment volumes to 20% in 2025.

- Based on our base case, prime residential yields are expected to remain stable over the next five years, with only a couple of markets expected to experience yield compression.

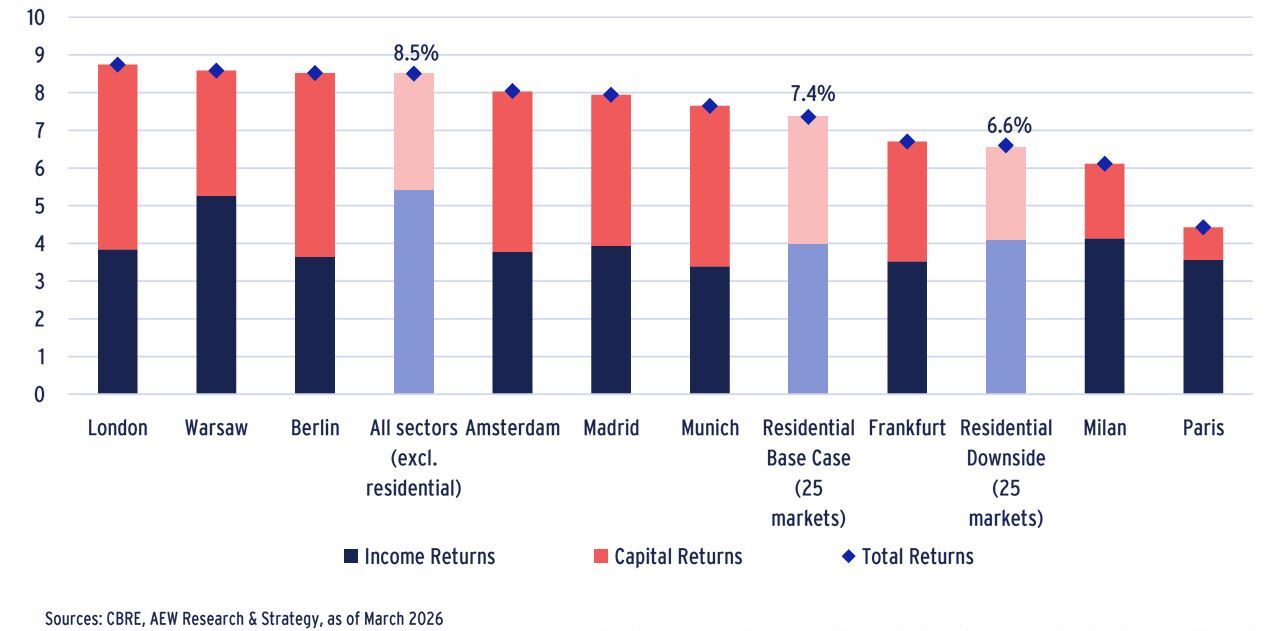

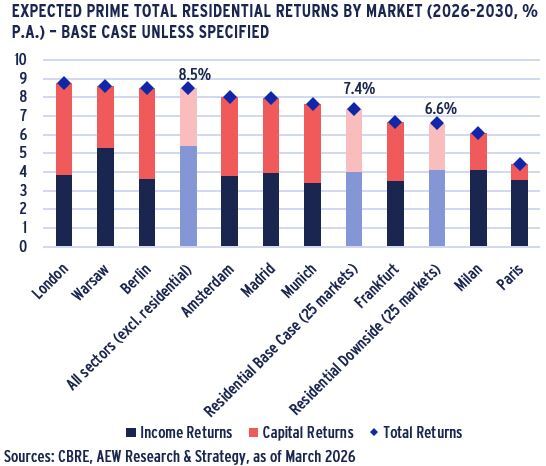

- As shown below, 2026-30 European residential total returns are projected at 7.4% p.a. in the base case, driven mostly by current income (4.0% p.a.) and capital return from rental growth, with limited capital return coming from yield compression.

- If the conflict in the Middle East escalates further, leading to prolonged higher inflation and base rates – as assumed in our downside scenario – the projection for European residential total returns by a modest 80 bps lower than in the base case at 6.6% p.a..

EXPECTED PRIME TOTAL RESIDENTIAL RETURNS BY MARKET (2026-2030, % p.a.) – base case unless specified

RECOVERY IN HOUSE PRICE GROWTH COULD BE HALTED BY THE CONFLICT IN THE MIDDLE EAST

MORTGAGE RATE DECLINE MIGHT PAUSE DUE TO INFLATION UNCERTAINTY

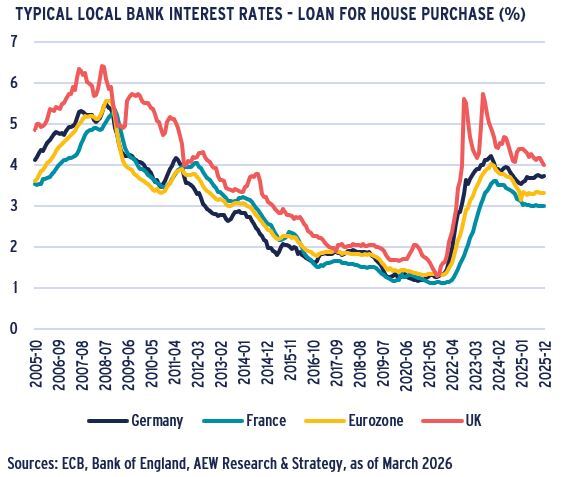

- As central banks have been cutting their base rates, the average Eurozone mortgage rate steadily declined to 3.30% by year-end 2025, a 70 bps decline from 2023.

- This partially reverses the significant increase in mortgage rates from 1.32% recorded since the year-end 2021 after the ECB and BoE started hiking their base rates to curb inflation.

- At 4.0% UK 5-year fixed rate 75% LTV mortgage rates have reduced significantly from their 5.7% peak but remain more than 70 bps higher than in the lower inflation Eurozone.

- However, UK mortgages are also dominated by variable or short (2-5 years) fixed mortgages rates in contrast to typically fixed rates for 20-25 years in the Eurozone.

- A prolonged conflict in the Middle East could lead to a reversal in monetary policies, if inflation stays above target for a sustained period, rate hikes might be deemed necessary.

- Any potential rate hikes could negatively impact lending volumes and residential prices going forward but could also increase demand for rental units.

RECENT RECOVERY IN BANK LENDING TO CONTINUE FOR S1 2026

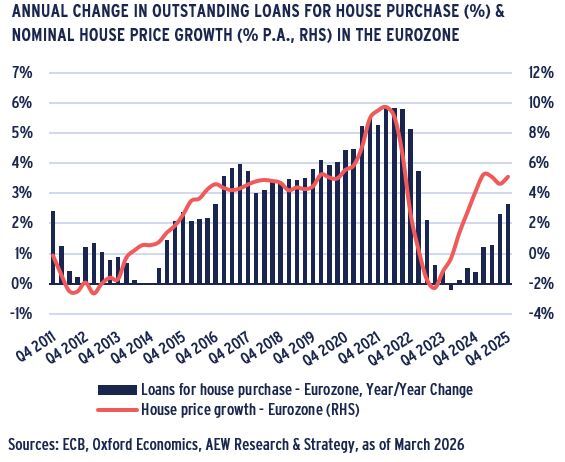

- Lending from banks to finance house purchases has continued to recover in 2025 after slowing down significantly in 2022 and 2023 with the rise in interest rates.

- House price growth and residential mortgage lending volumes have historically been highly correlated.

- House price growth in the Eurozone has gradually increased to over 5% in Q4 2025, after experiencing a modest decline in 2023 and starting its recovery in 2024.

- This rebound in lending and house prices is expected to continue in Q1 2026 as lending approval and funding processes do take time.

- For the rest of 2026, lending might be affected by central banks’ rate hikes in case inflation trends above their targets due to disruptions from a potentially prolonged conflict in the Middle East.

HOUSE PRICE RECOVERY MIGHT SLOW IF MIDDLE EAST CONFLICT CONTINUES

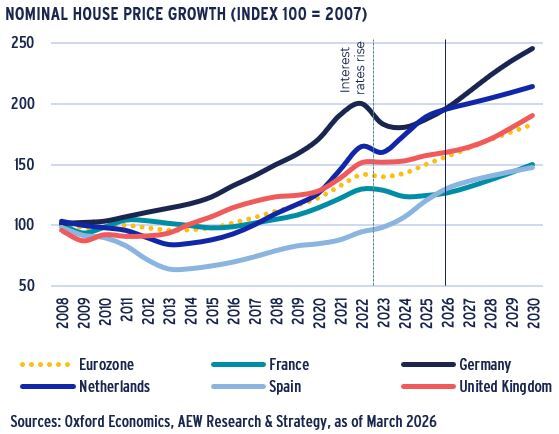

- House prices started recovering in 2024 across Europe, with Germany and France lagging most other countries.

- Spain stands out in Europe with a lasting post-GFC impact. In addition, Spanish residential prices continued to increase by around 8% p.a. on average in 2022-25 despite higher interest rates.

- Going forward, Oxford Economics projects an increase of 4.0% p.a. on average in the Eurozone over the next five years and a similar 3.9% p.a. in the UK.

- This represents an upward revision compared to the 3.5% forecast from last year.

- Again, a prolonged conflict in the Middle East could lead to downward forecast revisions for house prices if central banks change their monetary policy to curb inflation.

LIMITED NEW SUPPLY & COMPETITION FROM SHORT-TERM RENTALS HAVE PUT PRESSURES ON THE RENTAL MARKET

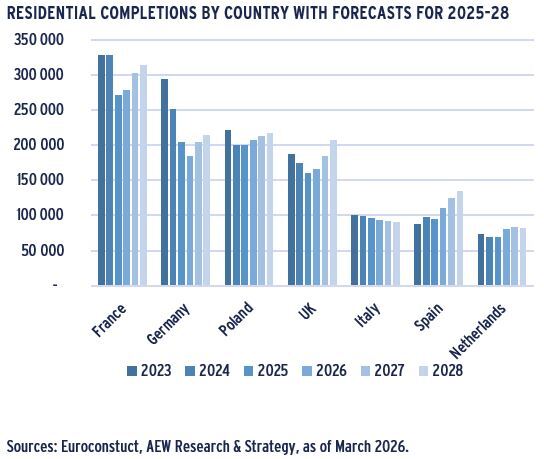

NEW SUPPLY EXPECTED TO INCREASE BUT REMAINS SHORT OF TARGETS

- In Europe, new supply of housing has decreased by 17% in 2025 compared to 2023.

- Germany and the Nordics recorded the sharpest declines at over 30%, while only Spain, Portugal and Ireland recorded increases over the same period.

- Despite a 17% year-on-year decline, at 272,100 p.a. France has built more dwellings in 2025 than any other European country, including Germany (205,000) and the UK (161,000).

- Residential completions in Germany and the Netherlands remain short of their stated annual government targets.

- 2025 German completions are expected to be as low as 205,000 units compared to a government target of 400,000.

- The Netherlands is estimated to have delivered around 70,000 dwellings in 2025, compared to a target of 100,000.

- Going forward, residential completions are expected to gradually increase in 2026-28 compared to 2025 levels in all countries except Italy.

SHORT-TERM RENTALS & SALES REINFORCE SUPPLY SHORTAGES

- Available privately-rented units have also decreased in some markets as private investors continue to sell their rental homes into the owner-occupied market.

- For instance, in the Netherlands, privately-rented rental stock fell by 8% in 2025 as 65,000 rental units were sold.

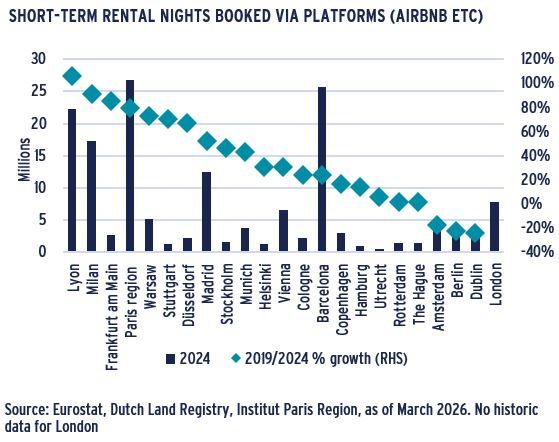

- In addition, an increasing number of dwellings are being let short-term on platforms such as Airbnb, notably in France, Spain and Italy.

- Since 2019, short-term rental nights booked via platforms such as Airbnb have increased by more than 20% in most European cities. Over 70% increases have been recorded in Lyon, Milan, Frankfurt and Paris.

- As a result of the increasing long-term rentals supply shortage, many countries or municipalities have recently tightened their rental regulations, with mixed results.

- In Paris, owners can rent out their properties only for 90 nights per year, compared to 120 nights previously. This has led to a decrease of 15% of listings on Airbnb in 2025.

RESIDENTIAL RENTAL GROWTH PROJECTED AHEAD OF OTHER SECTORS

- Actual prime residential rental growth of 3.3% in 2025 in Europe was slightly weaker than the 2021-25 average of 5.6% p.a.. due to lower inflation.

- Based on our Sep-25 projections, we expect 3.2% p.a. prime residential rental growth across the 25 European markets for 2026-30, above current projected inflation of 2.0%.

- Despite being regulated residential markets, Berlin, Madrid, Munich and Amsterdam are expected to outperform the European average rental growth over the next five years.

- Indeed, most rental regulations across Europe do not apply to newly-built dwellings, where the prime rents we project tend to be achieved.

- London prime residential rental growth has been revised downward somewhat. This is in part due to the 2025 UK Renters’ Reform Bill giving tenants more protection.

RESIDENTIAL INVESTMENT ACTIVITY RECOVERED, WITH OPERATED RESIDENTIAL OFFERING ALTERNATIVES TO INVESTORS

RESIDENTIAL LIQUIDITY EXPECTED TO FURTHER IMPROVE IN 2026

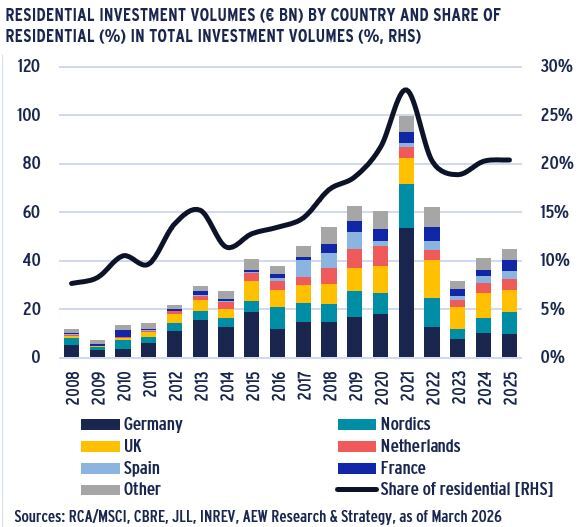

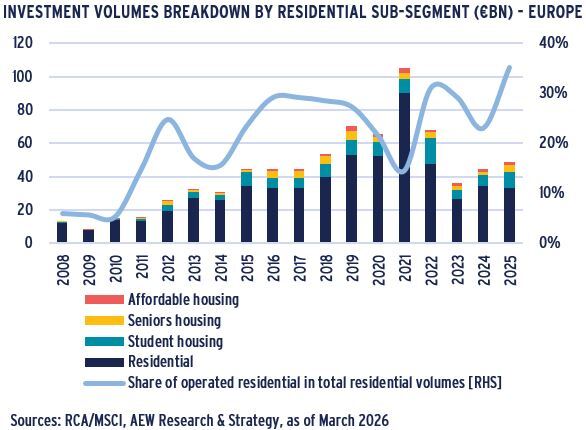

- European residential volumes totaled €45 bn in 2025, a 9% increase compared to 2024. However, this is still down 15% compared to its 10-year average.

- The 2025 pick-up in investment activity has mostly been driven by the Nordics and France.

- In both the INREV and the CBRE 2026 Investment Intentions Surveys, residential took the first position as investors’ preferred sector, ahead of logistics.

- This investor preference can be explained by the strong fundamentals providing the solid stability of cashflows offered and attractive financing conditions.

- On the back of these drivers, 2026 residential investment volumes are expected to increase further as investors seek to diversify away from offices and other sectors.

- JLL estimates that European living investment could reach €70bn in 2026.

SHARE OF RESIDENTIAL HAS INCREASED ACROSS EUROPE TO 20%

- Over the last fifteen years, residential has doubled its market share of total volumes invested in European property from 8% in 2008 to 21% in 2025.

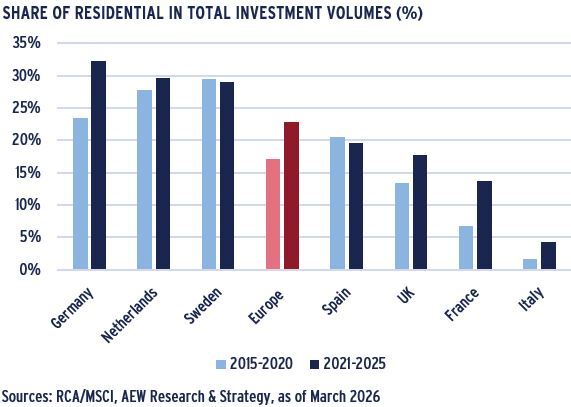

- Residential makes up around 30% of total volumes invested in property in Germany, the Netherlands and Sweden.

- This compares favorably to around 20% in the UK and Spain, 14% in France and only 4% in Italy.

- The share of residential in total investment volumes increased in all countries except Sweden and Spain where it remained stable.

- Some of the largest increases were recorded in the countries where the share of residential is the lowest - Italy, France and in the UK.

- As the stock (including new stock) available to institutional investors remains limited in these markets, the share of residential volumes is unlikely to rise much further.

OPERATIONAL RESI ALTERNATIVES SET NEW RECORD AT 35% OF DEALS

- The residential sector is diversifying, with emerging subsegments such as micro/flex/co-living, in addition to the more established student & senior housing sectors.

- Investment volumes in operated residential now represent 35% of total residential volumes in Europe, a record high.

- With high occupancy rates and strong rental growth, student housing remains a sought-after sector despite student population set to reach a peak in the coming years.

- The lack of senior housing transactions over the past couple of years can be explained by concerns around the profitability of some senior housing operators.

- Consolidation between operators is set to continue, while demographics tailwinds are likely to improve demand.

- Affordable housing is a smaller sub-segment (representing just 4% of total residential investment volumes in 2025).

- However, the recently launched European Affordable Housing Plan could lead to more investments in 2026.

RESIDENTIAL RETURNS WELL POSITIONED FROM DOWNSIDE SCENARIO

STRONG APPETITE FOR STUDENT HOUSING ACROSS EUROPE

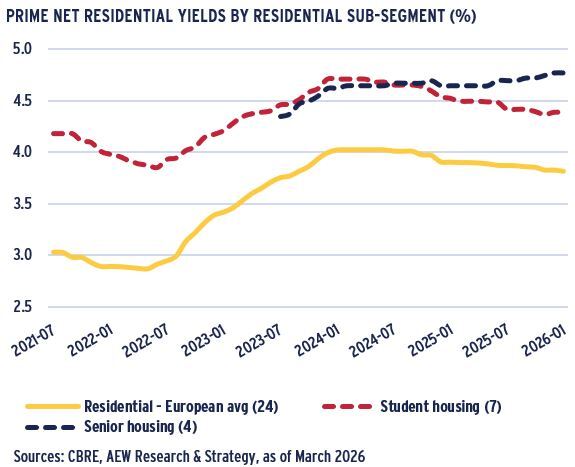

- From the second half of 2024, prime European residential yields have compressed, moving in by 30 bps from a peak of 4.1% to 3.8% at the start of 2026.

- All prime European residential markets have now fully repriced.

- Prime student housing yields have compressed from 4.7% on average across seven European markets, to 4.4% at the start of 2026, driven by strong investor appetite.

- By contrast, average prime senior housing yields moved out to 4.8% across four markets, reflecting concerns about the profitability of some senior housing operators.

- This offers additional excess spread compared to prime residential for new investors coming into the sector.

PRIME RESIDENTIAL YIELDS EXPECTED TO REMAIN STABLE

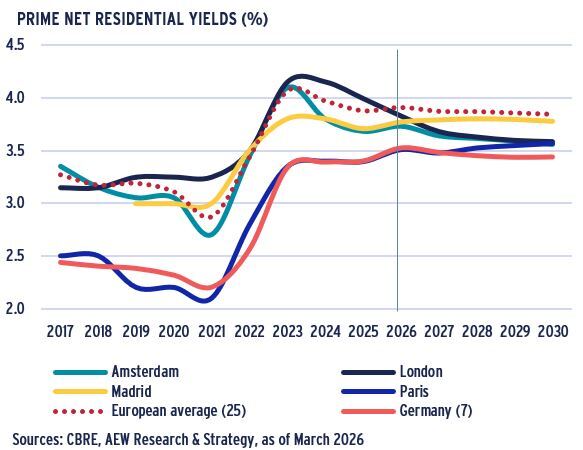

- Our Sep-25 forecasts indicate that prime residential yields are projected to compress from their 3.9% in late 2025 by just 10bps to reach 3.8% in 2030.

- These yield forecasts reflect Oxford Economics’ projected stabilisation of government bond yields as central banks are expected to keep interest rates stable.

- However, the conflict in the Middle East has led to an increase in energy prices. The ECB will therefore be closely monitoring potential inflation spikes and might hike rates, if needed.

- The strongest yield compression is expected in London, where prime residential yields are forecast to decrease from 4.0% to 3.6%.

- Modest yield compression is also expected in other European prime residential markets, notably in Warsaw.

- By contrast, prime Paris yields are forecast to move out slightly by 20 bps over the next five years as a result of higher government bond yields and lower credit ratings.

DOWNSIDE SCENARIO HAS LIMITED IMPACT ON RESIDENTIAL RETURNS

- Prime residential total returns are projected at 7.4% p.a. for the next five years on average across the same 25 markets covered, in the base case.

- This is 110 bps below the 8.5% total returns expected for all property sectors (excluding residential).

- A prolonged conflict in the Middle East could lead to above target inflation, higher bond and property yields.

- In that case, residential total returns will be negatively affected, as indicated in our downside scenario.

- Our downside scenario shows returns at 6.6% p.a., which confirms the limited impact as it is only 80 bps p.a. lower than in the base case.

- In the base case, all residential markets except Paris and Copenhagen should benefit from prime total returns exceeding 6% per annum over the coming 5-year period.

- London, Warsaw, Berlin & Amsterdam are expected to outperform the European average with 8-10% p.a. returns.

- By contrast, prime Milan and Paris residential are expected to underperform with 6.1% and 4.4%, respectively.

For more information, please contact:

IRÈNE FOSSÉ MSC

Executive Director, Research & Strategy Europe

irene.fosse@eu.aew.com

This material is intended for information purposes only and does not constitute investment advice or a recommendation. The information and opinions contained in the material have been compiled or arrived at based upon information obtained from sources believed to be reliable, but we do not guarantee its accuracy, completeness or fairness. Opinions expressed reflect prevailing market conditions and are subject to change. Neither this material, nor any of its contents, may be used for any purpose without the consent and knowledge of AEW. There is no assurance that any prediction, projection or forecast will be realized.