New Logistics Demand Drivers offset Impact from Iran Conflict

- Regardless of short-term cost pressures from the ongoing conflict in the Middle East, the long-term prime European logistics recovery is forecasted to withstand its effects and stay on track. Potential upside might come as occupiers switch their focus from just-in-time to just-in-case approach by adding more space to facilitate higher inventories.

- The latest GDP growth forecasts show only a very modest 10bps p.a. impact relative to our base case with limited effect on long-term inflation and bond yields. However, our downside scenario would be reflective of a potential prolonged conflict resulting in a significantly lower GDP growth, higher inflation and bond yields.

- E-commerce remains a big driver, but third-party logistics (3PL) providers now account for 44% of take-up. Competition and related consolidation in 3PL will step up based on Amazon’s recent move into the sector. In addition, growing manufacturing demand reflects Europe’s sovereignty push in defence, pharmaceuticals and energy.

- Recent tax changes applied on direct-to-consumer shipments from outside of the EU has already led Chinese and other e-retailers to switch to bulk import and local EU fulfillment hubs to improve costs and operational control.

- Short logistics development cycles allow it to respond quickly to changes in demand. Covid triggered strong take-up in 2021-22 as vacancy hit 2.4%. During 2023-25, increased supply pushing vacancy rates up to 5.4%. Going forward, new supply and demand are projected to be more balanced with vacancy projected at 4.3% by 2030.

- Our latest 2026-30 base case forecast for prime rental growth in the 35 logistics and 12 light industrial markets covered in our analysis both come in at 2.3% p.a. for the next five years. Any impact from our downside scenario on rental growth is expected to be modest.

- As in other sectors, higher interest rates pushed prime logistics yields from 3.7% to 5.3%. After the 2022-24 repricing and our revised base case with less bond yield tightening, prime logistics yields across all markets are expected to move in by only 20bps by 2030. This means current income and rental growth will be key for returns.

- Total (unlevered) returns across 35 European logistics markets are estimated at 8.5% p.a. for 2026-30 in our Mar-26 base case assuming no prolonged conflict in the Middle East. UK and CEE markets are expected to achieve the highest logistics total returns at 9.9% p.a. and 9.1% p.a., respectively.

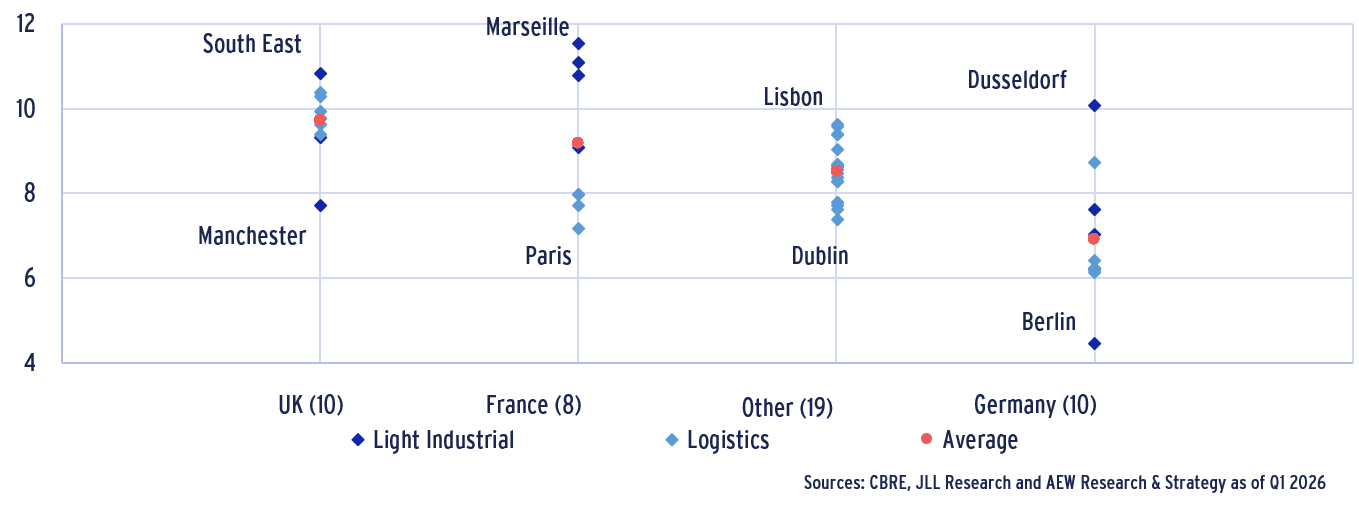

- 2026-30 projected annual returns across our covered logistics and light industrial markets range from 4.4% (Berlin) to 11.2% (Marseille), a 7% spread. Light industrial markets are showing solid resilience relative to logistics. Local market selection, with ample investable stock and liquidity are key to optimise risk‑adjusted returns.

EUROPEAN PRIME LOGISTICS & LIGHT INDUSTRIAL TOTAL MARKET-LEVEL RETURNS DISTRIBUTION BY COUNTRY (2026-30, % PA)

Please click on the links above to access the full report.

For more information, please contact:

HANS VRENSEN CFA, CRE

Managing Director, Head of Research & Strategy Europe

hans.vrensen@eu.aew.com

This material is intended for information purposes only and does not constitute investment advice or a recommendation. The information and opinions contained in the material have been compiled or arrived at based upon information obtained from sources believed to be reliable, but we do not guarantee its accuracy, completeness or fairness. Opinions expressed reflect prevailing market conditions and are subject to change. Neither this material, nor any of its contents, may be used for any purpose without the consent and knowledge of AEW. There is no assurance that any prediction, projection or forecast will be realized.