AEW's European Research & Strategy team present their latest report focused on the European office market:

- Over the next five years, office-base employment growth in Europe is expected to slow as working-age population is projected to shrink and is only partly offset by continuing urbanisation.

- Despite increasing concerns over the impact of AI on office-based employment, early US data signals are not as clear-cut as media headlines suggest. However, initial European data shows that AI has a negative impact on tech companies’ hires.

- In the short term, European AI adoption and its impact on office employment will be limited by soaring AI costs, limited data centres computing capacity as well as sovereignty concerns triggering a need for local EU solutions.

- Office vacancy rates continued to increase in Q1 2026, including in CBD markets, as cost-conscious occupiers increasingly focus on more affordable non-CBD locations. However, with less new supply and an increasing number of office conversions, overall vacancy is projected to come down from its 9% peak mid-year 2026 to 7% by 2030.

- Average 2026-30 prime headline rental growth is expected to reach 3.9% p.a. across all 63 covered European office submarkets. These projections are expected to remain robust at 3.7% p.a. even in our downside scenario.

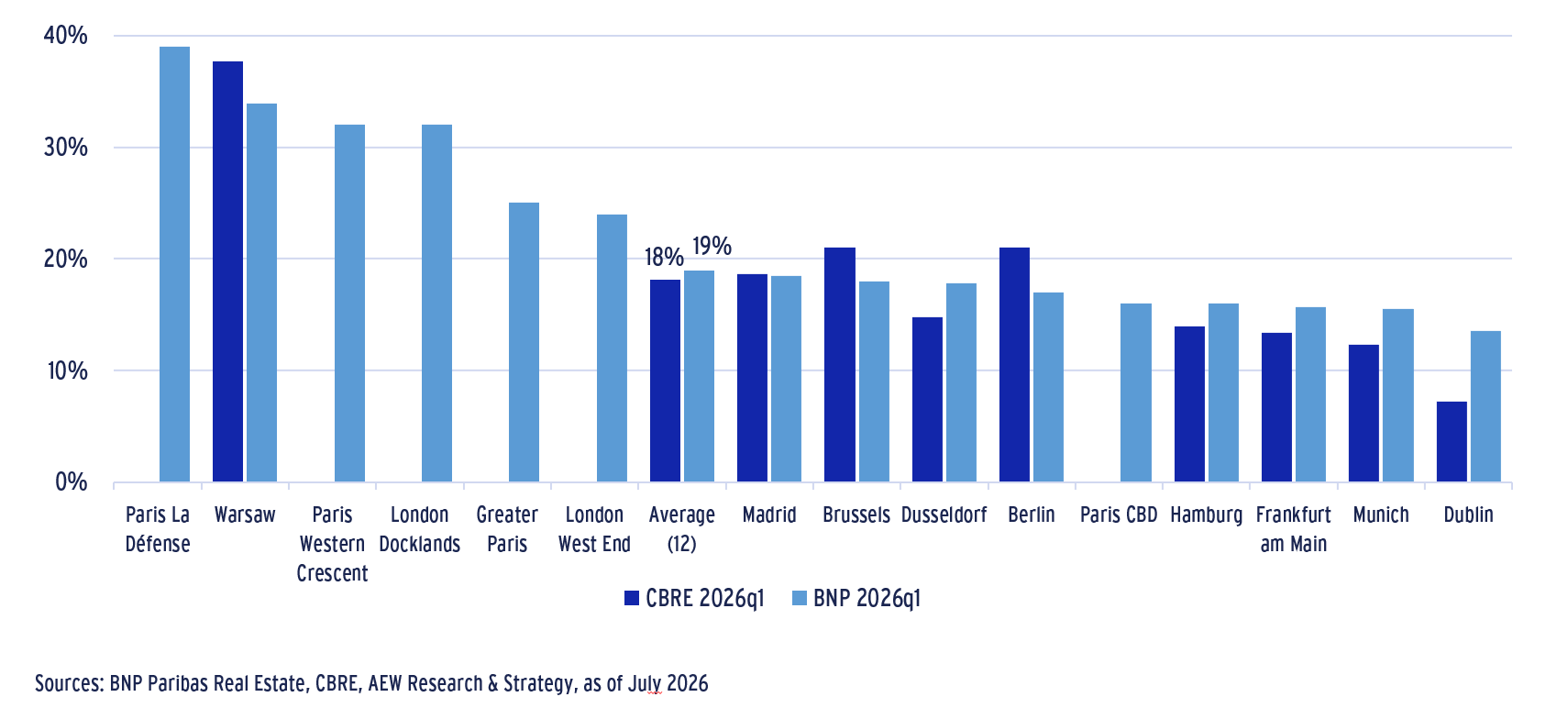

- While headline office rents have continued to grow, letting incentives (including free rent and tenant improvements) have increased in Europe since 2019. This is especially the case in peripheral non-CBD Paris and London markets, like La Défense and Docklands, where they reached near 40% of headline rents.

- 2026 office transaction activity has slowed down significantly since the start of the conflict in the Middle East due to higher financing costs and a renewed bid-ask spread as many buyers tried to renegotiate terms.

- With the negotiations continuing between the US and Iran to settle their conflict, oil prices and swap rates have stabilised somewhat. Assuming the peace process advances, a recovery in liquidity in H2 2026 could be expected.

- Office valuations reflect the ongoing bifurcation between best-quality offices having experienced increasing values, while offices facing structural vacancy and higher incentives have experienced significant value declines.

- The significant repricing recorded by the office sector in 2022-24 in combination with the near 4% p.a. expected rental growth, drive our latest prime office forecasts. Total returns are expected to reach 10% p.a. over the next five years across our 63 covered European markets.

INCENTIVES (RENT-FREE AND TENANT IMPROVEMENTS) AS % OF HEADLINE OFFICE RENTS ACROSS FULL LENGTH OF THE LEASE, BY MARKET

Please click on the links above to access the full report.

For more information, please contact:

HANS VRENSEN CFA, CRE

Managing Director, Head of Research & Strategy Europe

hans.vrensen@eu.aew.com

This material is intended for information purposes only and does not constitute investment advice or a recommendation. The information and opinions contained in the material have been compiled or arrived at based upon information obtained from sources believed to be reliable, but we do not guarantee its accuracy, completeness or fairness. Opinions expressed reflect prevailing market conditions and are subject to change. Neither this material, nor any of its contents, may be used for any purpose without the consent and knowledge of AEW. There is no assurance that any prediction, projection or forecast will be realized.