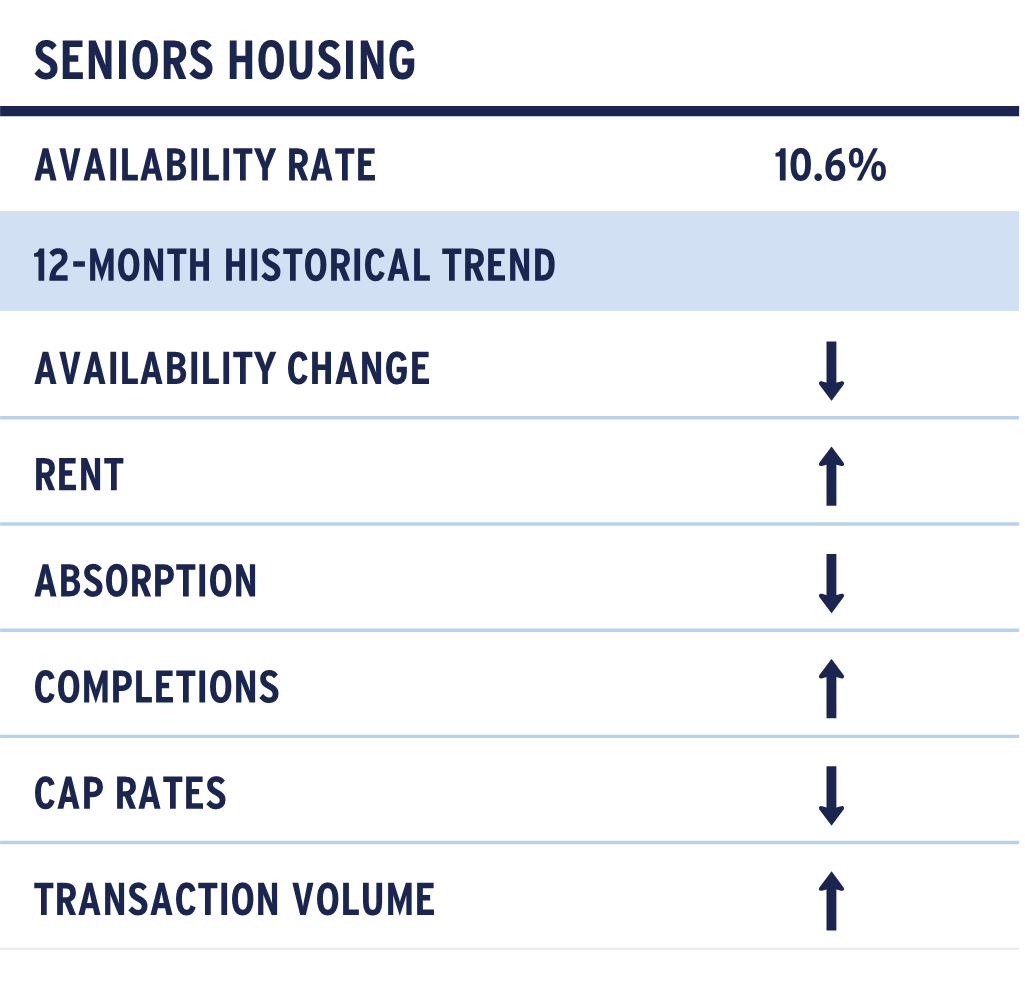

The seniors housing sector continued to post solid revenue and NOI gains through the fourth quarter, extending the upward trajectory established over the past several years. Move-ins once again exceeded resident turnover, driving net absorption to a level nearly twice the long‑term average. Although this pace was 23% lower than in the same period a year ago, it still surpassed all but two pre‑pandemic quarters, based on data from the National Investment Center for Seniors Housing & Care (NIC). This persistent demand underscores the sector’s resilience and ongoing rebound, supported by the limited number of new developments breaking ground, which has enabled operators to maintain strong pricing power.

Occupancy improvements were widespread across the seniors housing landscape, with NIC-monitored primary and secondary markets reaching 89.4% in the fourth quarter, an increase of 40 basis points from the prior quarter and 210 basis points above the pre‑pandemic mark of 87.3%. Both higher- and lower‑acuity product types supported this momentum, with lower‑acuity communities climbing past 91% occupancy, while higher‑acuity settings rose above their pre‑COVID levels, exceeding 89%. Collectively, these patterns highlight a compelling environment for operators to benefit from strengthening demand across the acuity spectrum.

FIGURE 1: YEARS OF RENT IN A MEDIAN HOME

Source: St. Louis Federal Reserve: NICMAP Primary and Secondary Markets 4Q2025

Rent increases have moderated from their inflation‑era highs, yet operators continue to secure mid‑ to high‑single‑digit rate adjustments. This has brought the “Years‑of‑Rent” metric for a median home back to levels last observed in 2012 (6.2 years), down from the peak of 7.9 years reached in mid‑2022. Revenue performance is generally aligning with or outperforming budget expectations, and operators are positioned to maintain pricing leverage through 2026. On the cost side, operating expense pressures have eased, helping support double‑digit NOI gains. Even so, labor expenses remain a major focal point, and operators continue refining workforce strategies to protect margins.

From a supply standpoint, conditions remain tight. New project starts continue to decline, constrained by limited access to financing and unfavorable development economics, particularly as many transactions have occurred at prices at or below current replacement cost, even for stabilized properties. Over 2025, groundbreakings totaled just over 9,500 units, equal to only 0.9% of the existing stock, marking the slowest pace since NIC began tracking the market. With roughly half of the nation’s seniors housing inventory now more than 25 years old, obsolescence is likely occurring faster than new product is coming online. At present, only 2.3% of inventory is under construction, while annual absorption is running at 2.8%, down gradually from the post‑pandemic peak of nearly 6% absorption. This sustained supply‑demand imbalance continues to favor incumbent operators and investors, supporting stronger fundamentals and reinforcing pricing and occupancy performance in the near term.

The sector’s needs‑driven demand profile continues to position it as one of the most resilient areas within commercial real estate. Over the near term, pricing power and broader operating fundamentals are expected to strengthen further, supported by powerful demographic trends. The leading edge of the Baby Boomer cohort is roughly 60% larger than today’s resident base, and neither existing inventory nor the development pipeline is positioned to fully absorb the surge in future demand. This demographic momentum represents a significant long‑term growth catalyst for seniors housing.

Capital markets continued to strengthen in 2025, marked by improved liquidity and increasing lender engagement. Fourth‑quarter transaction volume approached $5.5 billion, the second‑highest quarterly total in the past decade, surpassed only by 3Q 2021, and was largely fueled by increasing acquisitions from public REITs. Although private and institutional investors remained active participants, they were net sellers on balance. Rolling four‑quarter transaction totals were the highest recorded in ten years, more than twice the pace seen in 2023, signaling a meaningful uptick in market liquidity. Premium assets in major markets continued to draw robust bidder interest, while weaker properties saw limited demand or required higher cap rates, though these yields have begun to compress. Overall pricing has trended upward on a per‑unit basis, with cap rates generally ranging from the low‑5% to mid‑6% range.

Lenders have remained constructive on refinancing situations where borrowers can demonstrate a credible forward path and are selectively pursuing new originations. Traditional agency lenders, including Fannie Mae and Freddie Mac, are actively quoting transactions, and banks have begun reestablishing their presence in the market. Capital from debt funds has also become more accessible, particularly for value‑add strategies and assets that have not yet reached stabilization. Although credit spreads have tightened, lender risk appetites continue to vary widely. A deeper pool of capital is available for high‑quality, stabilized properties, whereas construction financing still encounters meaningful hesitation as many transactions remain at below replacement cost. Publicly listed REITs continue to access unsecured debt markets at increasingly favorable rates.

In conclusion, the seniors housing sector is performing broadly in line with expectations and offers one of the most compelling investment backdrops seen in recent years. Asset values are trending higher, and improved capital‑market conditions are adding meaningful liquidity to the transaction landscape. Strong and steadily improving fundamentals, supported by limited new supply and continued rent growth, are driving top‑line performance and enabling double‑digit NOI expansion. While ongoing risks such as labor cost pressures, aging physical product, and tighter financing channels remain important considerations, the sector’s long‑range outlook is decidedly positive. Demographic tailwinds are especially significant, with the population entering peak demand years projected to grow by more than 50% over the near term, creating a sustained runway for expansion.

For more information, please contact:

MICHAEL ACTON, CFA®

Managing Director, Head of Research & Strategy, North America

michael.acton@aew.com

+1.617.261.9577

JAY STRUZZIERY, CFA®

Head of Investor Relations

jay.struzziery@aew.com

+1.617.261.9326

This material is intended for information purposes only and does not constitute investment advice or a recommendation. The information and opinions contained in the material have been compiled or arrived at based upon information obtained from sources believed to be reliable, but we do not guarantee its accuracy, completeness or fairness. Opinions expressed reflect prevailing market conditions and are subject to change. Neither this material, nor any of its contents, may be used for any purpose without the consent and knowledge of AEW. There is no assurance that any prediction, projection or forecast will be realized.