European Real Estate Recovery Can Withstand Pressure From Middle East Conflict

- The conflict in the Middle East retains centre stage. Regardless of its short-term pressures, the long term prime European real estate recovery is forecasted to withstand its effects and stay on track with solid current income yields and projected rental growth offering resilience over our 5-year horizon.

- The latest GDP growth forecasts since the conflict started show an impact of 10bps p.a. relative to our base case with limited effect on long-term inflation and bond yields. However, our downside scenario would be reflective of a potential prolonged conflict resulting in a significantly lower GDP growth, higher inflation and bond yields.

- The fundamental strength of the occupier markets is supported by declining new supply across sectors, leading to projected lower vacancy rates for offices and logistics. These underpin solid prime 2026-30 rental growth forecasts of 2.4% p.a. and 2.1% p.a. in both the base case and downside scenarios, respectively.

- In our base case, even as government bond yields have risen, office yields are forecast to tighten by 40 bps over the next five years, followed by shopping centres, logistics and residential at 25bps, 24bps and 17bps, respectively. In the downside scenario, logistics and high street retail are forecast to show some yield widening.

- Recent pre-conflict investor sentiment was positive supporting solid 2025 transaction volume momentum. Despite the ongoing conflict and its negative immediate effects on current deals in progress, the pent-up investor demand is expected to drive long term volumes higher, once confidence returns.

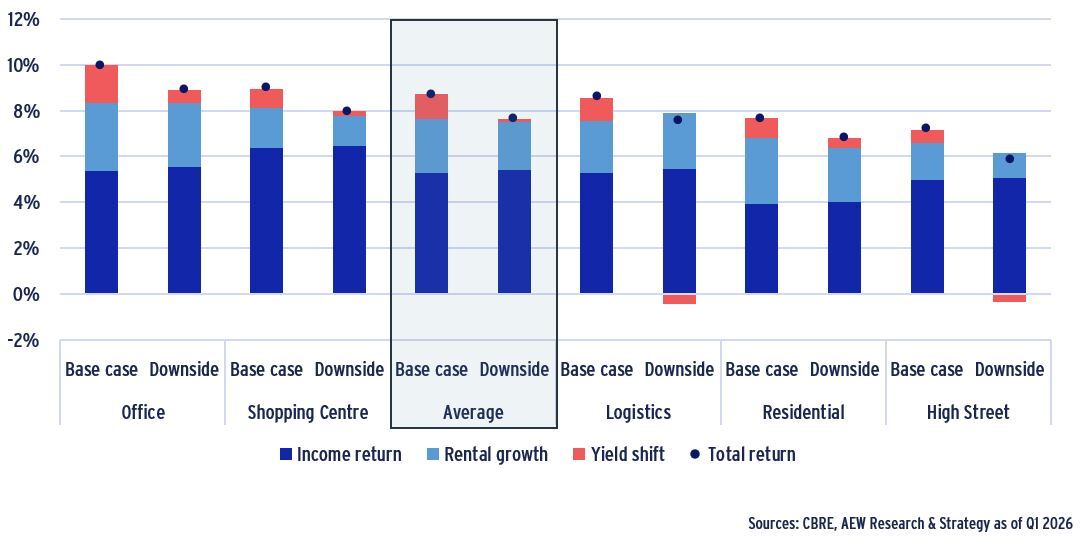

- Base case total returns for European real estate are projected at 8.7% p.a. in 2026-30. The downside scenario yields 7.6% p.a., removing just 1.1% p.a. from the base case and demonstrating the sector's ability to withstand the macroeconomic pressure from external shocks due to solid income yields and rental growth projections.

- Average European prime office markets are projected to have the highest returns at 10.0% p.a. Shopping centers come second with returns of 8.9% p.a., while logistics, residential and high street retail are expected to deliver 8.5% p.a., 7.7% p.a. and 7.2% p.a., respectively.

- Local office markets returns show the widest range of any sector with Zurich at 4.5% p.a. and Canary Wharf (Docklands) at 16.9%. Therefore, careful market selection is important regardless of sector average returns.

- Total returns in the base case comprise 5.3% p.a. income return, 2.4% p.a. of rental growth, while just 1.1% p.a. attributed to yield shift. Most of the limited damage to the total returns in the downside scenario is attributed to short-term yield widening with a partial reversal later in the 5-year forecasting period.

EUROPEAN ALL MARKETS PRIME TOTAL RETURN DECOMPOSITION FOR BASE CASE AND DOWNSIDE (2026-30 FORECAST), % P.A.

ECONOMIC BACKDROP – MIDDLE EAST CONFLICT TAKES CENTRE STAGE

MIDDLE EAST CONFLICT AFFECTS ENERGY & INFLATION

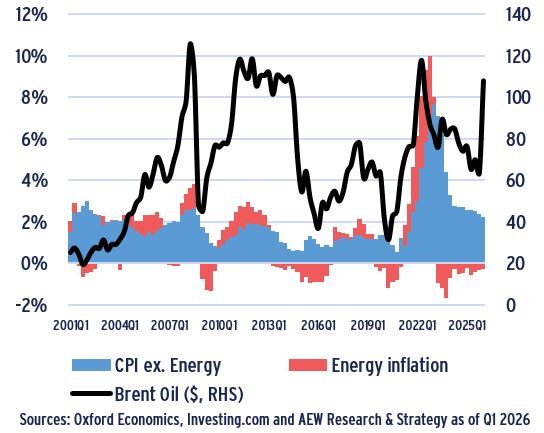

- On 28 February 2026, the US and Israel launched surprise airstrikes on Iran killing its political leader. As Iran retaliated, the military conflict spread to other gulf countries in March.

- As a result, access to the narrow strait of Hormuz has been restricted as insurance has become very costly and shippers don’t want to jeopardise their vessels, crews or cargos.

- Since 20% of global crude oil and natural gas is shipped through this strait, energy prices have spiked in response. This is expected push up consumer prices (CPI).

- The impact on CPI has been limited so far as strategic oil reserves have been released by various governments.

- For the moment, the price shock is expected to be temporary and milder than that following 2022 Ukraine invasion, which was a structural hit to Europe's energy supply.

- The restrained reaction of wholesale electricity markets to the recent surge in natural gas prices has been due to the higher share of renewables and increased hedging by utilities.

EUROZONE CPI INDEX & ENERGY COMPONENT (%, LHS) AND BRENT OIL PRICE ($/BARREL, RHS)

SWAP RATES HAVE PRICED IN HIGHER INFLATION

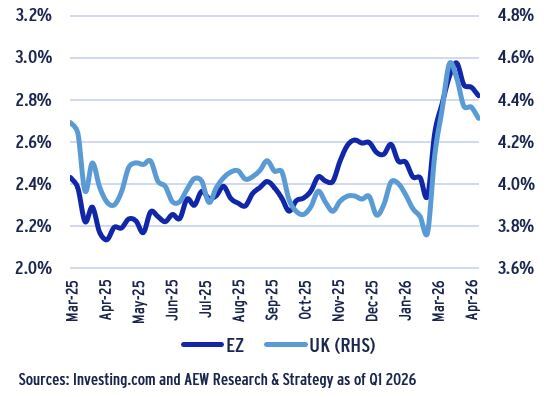

- As recent events triggered concerns for higher inflation, both Eurozone and UK swap rates increased since the start of the conflict by 40bps and 70bps, respectively

- This further emphasizes that 4.45% UK swap rates are significantly higher than the 2.75% Eurozone swap rates offering more attractive debt for Euro-denominated deals.

- 5-year swap pricing takes into account not only inflation expectations but also the potential for rate hikes by central banks, including the ECB and Bank of England.

- Even though rate hikes won’t directly reduce energy-related prices the dampening effect on growth is likely to affect other prices in the medium term

- The key issue for most real estate investors is that their investment horizon is typically 5-10 years, which implies they are isolated from short-term interest rate volatility.

- This is reflected in our 5-year forecast assumptions and methodology as will be discussed next.

5-YEAR SWAP RATES FOR EUROZONE (3-M EURIBOR) & UK (3-M SONIA), % P.A.

SUFFICIENT HEADROOM COMPARED TO DOWNSIDE

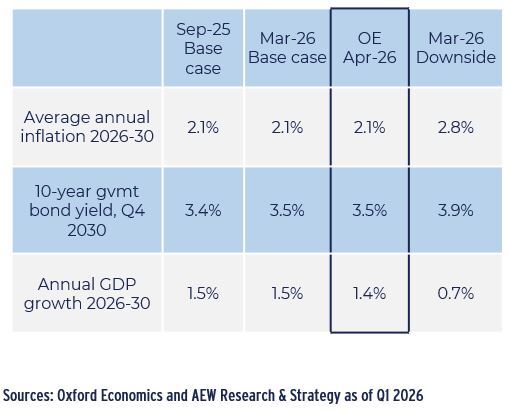

- Given the uncertainty related to the ultimate length and impact from the current middle east conflict it is useful to consider our base case scenario in relative terms.

- Oxford Economics’ latest updates reflecting events to date show only a modest on annual GDP growth but no material impact on annual inflation and 2030 bond yields.

- This disregards short term impacts, which is appropriate given the prevailing holding period of most investors.

- Our Mar-26 downside scenario offers sufficient headroom to allow for a 50% decline in GDP growth, a 33% increase in inflation and a15% increase in 2030 bond yields.

- In other words, the conflict would have to continue to escalate and trigger a long-term impairment for the gulf countries’ ability to restart oil and gas deliveries.

- Based on events to date, our Mar-26 downside is expected at a limited probability even if it is useful to be aware of it.

MACRO ASSUMPTIONS FOR 20-COUNTRY AVERAGE VARIOUS SCENARIOS

ECONOMIC BACKDROP – CONFLICT IMPACT EXPECTED TO BE LIMITED BY 2030

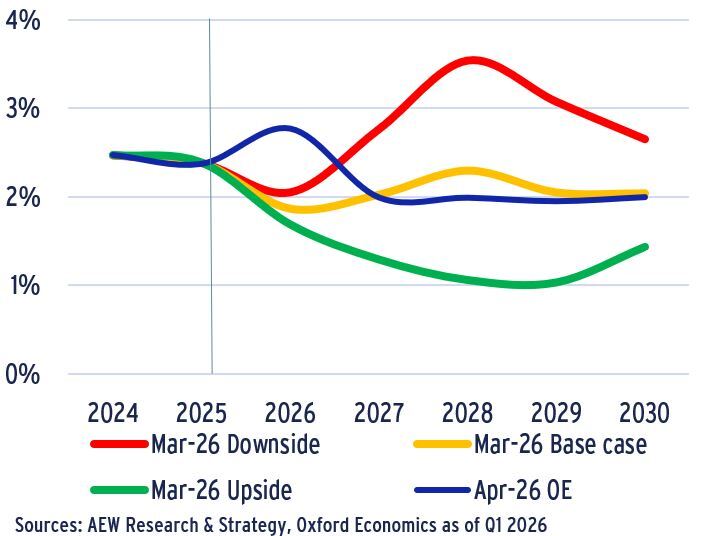

INFLATION IMPACT LEAVES HEADROOM FOR DOWNSIDE

- Oxford Economics lifted its 2026 projected inflation from 1.9% to 2.8% in April 2026. However, this is expected to revert back to 2% by 2027-30.

- Higher inflation will affect real household income, consumer spending and fixed investments. This in turn will reduce GDP growth even if the long-term impact is limited.

- If the conflict in the Middle East is both escalated and prolonged, the downside scenario might become relevant.

- This downside scenario assumes a spike in inflation of 3.5% in 2028 but a return to 2.6% by 2030.

- In both base case and downside scenarios, central banks are assumed to hike their policy rates.

- In fact, current Eurozone bond prices are already reflecting two ECB rate hikes with the latest geopolitical news.

- Given that rate hikes are not directly reducing energy prices, non-monetary policies (like price caps) will need to address this key driver of inflation.

INFLATION RATE (%, EUROPEAN AVERAGE ACROSS 20 COUNTRIES), % P.A.

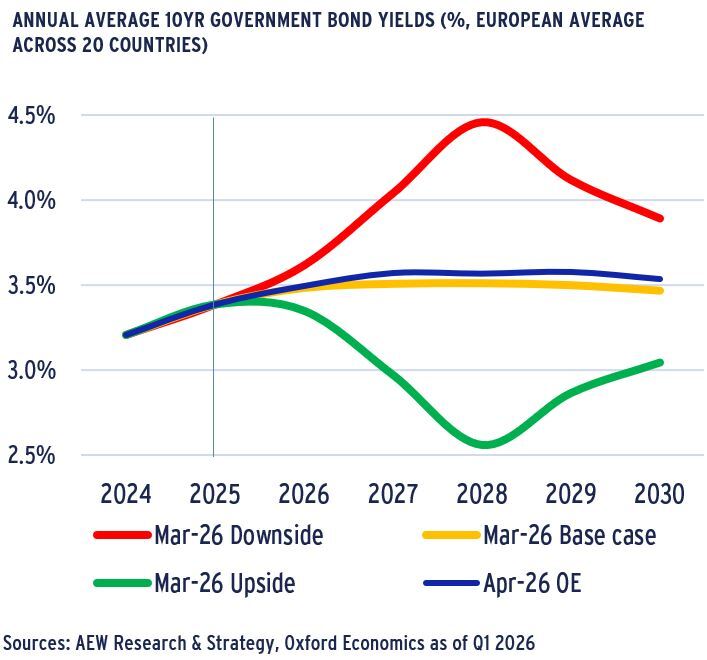

GOVERNMENT BONDS TO STAY FLAT IN BASE CASE

- Our Mar-26 base case scenario assumes that 2030 10-year bond yields remain near 3.5%, and the recent conflict has not yet changed the five-year outlook materially.

- The downside scenario assumes bond yields peak at 4.5% in 2028 but settle at 3.9% by 2030.

- Based on previous analysis, investors will price government bond yield changes with some delay into property yields.

- Also, historical correlations confirm that a 100bps movement in government bond yields corresponds to a 36bps move in prime European property yields.

- Most countries had periods of decoupling when government bond yields exceeded the prime property yields or moved in opposite directions.

- In our total return projections, interim changes in bond and property yields do not materially affect total returns as the yield at the end of the 5-year holding period is more crucial.

- Based on the mean reverting of bond (and property) yields the downside scenario’s impact is projected to be modest relative to the current short-term volatility.

ANNUAL AVERAGE 10YR GOVERNMENT BOND YIELDS (%, EUROPEAN AVERAGE ACROSS 20 COUNTRIES)

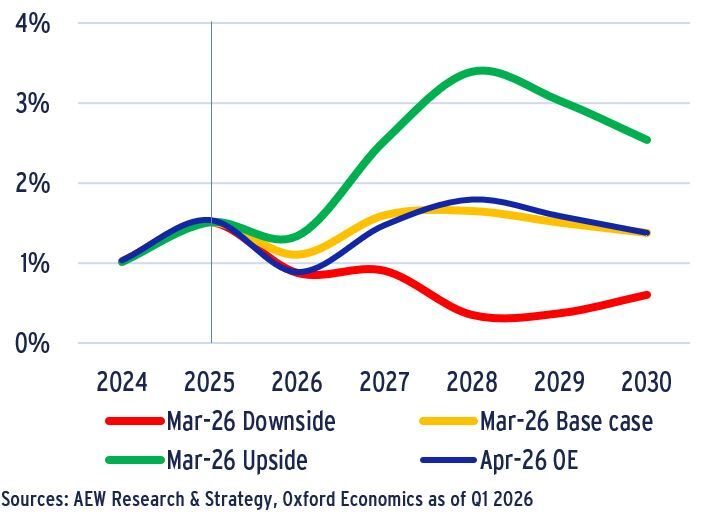

TOO EARLY TO REVISE BASE CASE GDP GROWTH

- Our property market models use Oxford Economics’ (OE) forecasts, which for the base case assumes of 1.5% GDP p.a. growth for Europe in 2026-30.

- Due to the conflict in the Middle East, OE has downward adjusted its 2026 GDP growth from 1.1% to 0.9%, which is in line with the downside for the year alone.

- However, long-term GDP forecasts for the full five years are likely to show much less adjustment as the inflation and interest rate shock is project to correct.

- As events stand now it remains too early to revise our base case for the full period or revert to the downside scenario.

- Our downside scenario is not recessionary across our full 20-country coverage, even if some individual nations might slip into this state for part of the period.

ANNUAL GDP GROWTH RATE (%, EUROPEAN AVERAGE ACROSS 20 COUNTRIES)

MARKET OVERVIEW – HIGHEST RENTAL GROWTH FOR RESIDENTIAL & OFFICES

LIMITED AND DECLINING SUPPLY IS KEY DRIVER FOR OCCUPIER MARKETS

- While demand is likely to be limited given modest GDP growth, European market fundamentals remain robust as new supply is forecast to decline in all property sectors.

- The logistics sector remains the most dynamic but supply is expected to grow by less than 5% pa over the next four years, compared to more than 6% over the past four years.

- Modern stock per capita have reached sufficient levels in most European countries.

- The office market is expected to see very limited new developments in the coming years, with less than 1% stock growth.

- Developments in the residential sector remain very limited with 0.5% supply growth expected in the coming years.

- Shopping center developments are not included in the analysis as most new developments are extensions of existing centres.

STOCK GROWTH BY SECTOR, PER ANNUM (%)

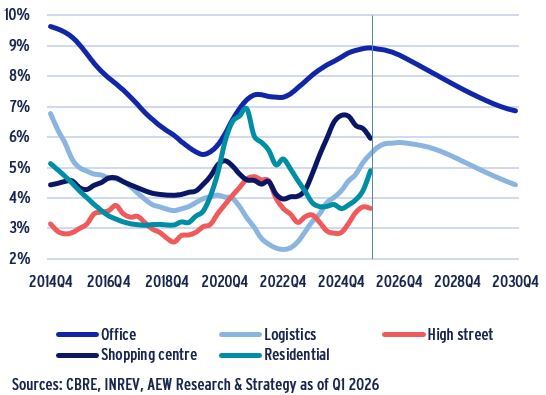

OFFICE & LOGISTICS VACANCY RATES PROJECTED TO COME DOWN

- European vacancy rates across property sectors have been declining since the pandemic, with the notable exception of 9% for offices and near 6% for logistics.

- However, based on CBRE’s projections, vacancy rates for these two sectors are expected to come down to below 7% and 4.5% by year end 2030.

- In both cases, this is triggered by lower new supply. For offices in particular there is been a solid pick up in letting activity, especially in some of the prime CBD sub-markets.

- For other sectors CBRE has no projections for vacancy rates and we use the INREV asset-level index (ALI) data to show vacancy ranges between 6% and 4% as of year-end 2025.

- Latest shopping centre vacancy stands at 6% while at below 4%, high street retail vacancy reflects the high quality of assets reported by investors to the ALI index.

- Residential vacancy, tracked by INREV, did record an increase but remains below 5% compared to the near 7% during COVID lockdowns.

VACANCY RATES PER SECTOR BASED ON THE INREV ASSET LEVEL INDEX (%, 4-QUARTER MOVING AVERAGE) – STABILISED ASSETS ONLY

SOLID OCCUPIER MOMENTUM EDGES PRIME RENTS UP

- Our latest 2026-30 base case forecast for prime rental growth across all sectors comes in at 2.4% p.a., a modest upgrade from 2.1% in our September 2025 base case.

- Offices have taken the top spot in our latest prime rental growth outlook with an average of 3.0% p.a.

- But secondary office rents remain under pressure as many occupiers prefer prime buildings in CBD locations.

- Prime residential rents are forecast to have growth of over 2.9% p.a. having been edged into second position due to realising stronger than expected rental growth in H2 2025.

- All sector-average ranges between a solid 2.1% p.a. in downside and 2.8% p.a. in the upside scenario.

- Shopping centres and high street retail have projected 2026-30 rental growth of 1.7% and 1.6% p.a., respectively.

- As before, sensitivity is relatively high for both retail sectors. Logistics’ scenario impact is explained by the historical ties between rental growth and inflation rather than GDP.

EUROPEAN AVERAGE PRIME RENTAL GROWTH BY PROPERTY TYPE OVER THE NEXT 5 YEARS (2025-29, % PA)

MARKET OUTLOOK – POSITIVE VOLUMES & SENTIMENT MOMENTUM EXPECTED TO SLOW

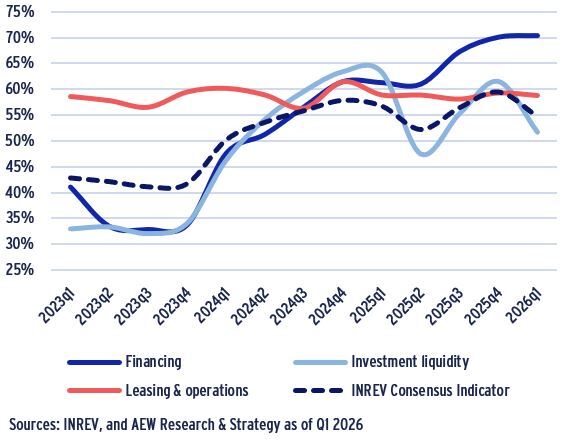

INVESTOR SENTIMENT MOVES SIDEWAYS

- At 55% sentiment among European managers and investors edged down in the latest Q1 2026 INREV sentiment survey, but remains well above the levels seen in 2023.

- Any result above 50% indicates a positive sentiment, which confirms a strong correlation with transaction volumes over the last three years – similar to what the IPE survey showed.#

- The various sub-indices offer some interesting additional insights, as we note a strong stability in the leasing and operation sub-index.

- This stability is surprising given the significant increase in office and logistics market vacancy rates. But it might be reflective of respondents’ institutional quality assets.

- Since 2023, the overall sentiment index has been lifted strongly by the financing and investment liquidity sub-indices, even if the latter seems to have partially reversed in 2025-26.

- This is in line with our European debt market analyses showing that refinancing challenges have eased.

INREV SENTIMENT INDEX RESULT WITH SELECTED SUB-INDICES , %

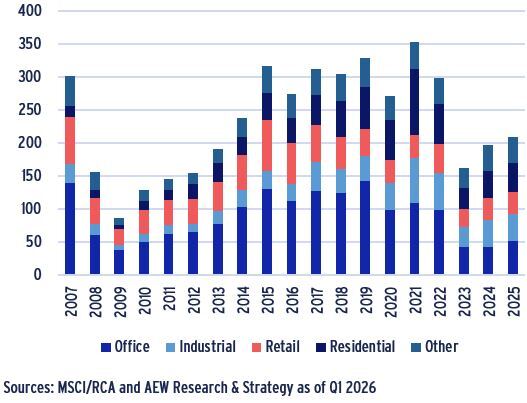

2025 VOLUME MOMENTUM LIKELY TO SLOW IN H1 2026

Full year 2025 transaction volumes across the main property types came in at €209bn. This was better than our previous €200bn projections and up 6% from the €197bn for 2024.

Even as the momentum has turned, some banks and servicers are reporting distressed sales as legacy lenders push for repayment and fund investors seek redemptions.

Given its reduced share in total volumes, bid-ask spreads for many potential office deals remain high even after its dramatic repricing in 2022-24.

The conflict in the Middle East has already affected existing negotiations as leveraged buyers would be eager to price in the increased swap rates affecting their costs of debt.

Even as some deals are delayed and investors wait for the uncertainty to pass, the pent-up investor demand is expected to build up.

Transaction volumes are likely to catch up to the recovery trend when investors’ confidence returns.

EUROPEAN ANNUAL INVESTMENT VOLUMES BY PROPERTY TYPE (€BN)

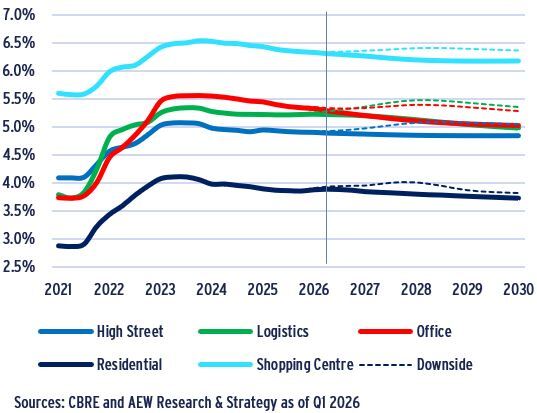

DOWNSIDE SHOWS 20-40BPS YIELD WIDENING FOR MOST SECTORS

- Given our base case projection for government bond yields, our property yields projections are unchanged from Sep-25.

- Since 2021, interest rates pushed prime property yields up for the all-sector average by 135bps over the 2022-24 period.

- At 190bps, office yields widened most of any sector by year-end 2024, followed closely by logistics and residential at 150 bps and 120 bps, respectively.

- Base case office yields are forecast to tighten by 40 bps over the next five years, followed by shopping centers, logistics and residential at 25bps, 24bps and 17 bps, respectively.

- In the case of a prolonged conflict in the middle east, the 40bps widening of government bond yields by 2030 in our downside scenario might be useful to consider.

- Across sectors, the impact on projected 2030 property yields ranges from 40bps for logistics to 9bps for residential for the downside scenario, with office and retail yields at 20-25 bps.

EUROPEAN AVERAGE PRIME YIELDS BY PROPERTY SECTOR – BASE CASE, %

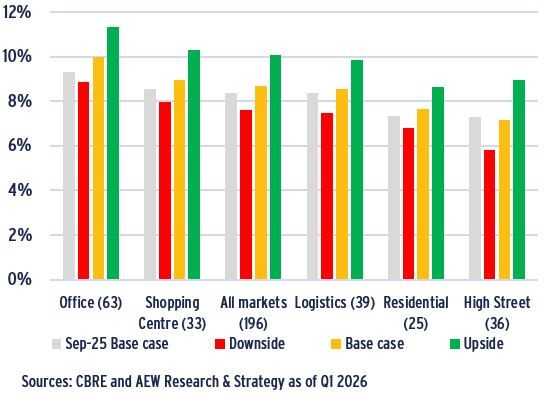

MARKET OUTLOOK – PRIME OFFICES RANK TOP EVEN IN DOWNSIDE SCENARIO

AT 10% P.A. OFFICES REMAINS TOP RANKED SECTOR

- All sector base case 2026-30 returns are projected at 8.7% p.a., with significant variation across sectors.

- Prime office markets are still projected to have the highest returns of any sector at 10.0% p.a. over the next five years.

- This is due to their bigger than previously expected 2025 repricing and stronger market rental growth.

- Shopping centre markets come in second place with returns of 8.9% p.a. on the back of their high current yields and rental growth projections.

- Our latest downside scenario shows returns at 7.6% p.a. on average across sectors with 10.1% in our upside scenario.

- Our latest return projections are primarily driven by higher current incomes as yields widened in the recent downcycle and capital value appreciation from rental growth.

- In the base case, projected yield tightening by year-end 2030 has been cut back given the latest bond yield projections limiting capital value growth from that source.

EUROPEAN AVERAGE PRIME TOTAL RETURNS BY PROPERTY TYPES (2026-30, % PA)

SECTOR AVERAGES REFLECT WIDE RANGE OF LOCAL MARKET RETURNS

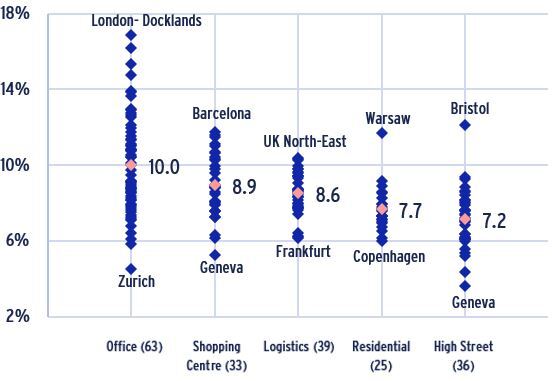

- Even if European office markets at 10% p.a. show the highest 2026-30 projected returns across sectors, there is a wide range of local market returns requiring careful selection.

- With Zurich at 4.5% p.a. and Canary Wharf (Docklands) at 16.9% p.a. the range for office returns is widest of any sector.

- For the 39 logistics segments, local market returns range from 6.2% p.a. for Frankfurt to 10.4% for UK North-east, which represents a 4% difference between highest and lowest.

- In the case of both residential and high street retail, single market outliers extend the range of local markets’ projected returns as for Warsaw residential and Bristol high street retail.

- This implies that a simple property sector and country allocation might not yield the best results for investors looking to optimize their risk-adjusted returns.

- Having projected returns on each of the 198 modeled market segments allows for a more precise selection.

EUROPEAN PRIME TOTAL RETURNS DISTRIBUTION BY SECTOR (2026-30, % PA)

DOWNSIDE SCENARIO REMOVED JUST 1.1% p.a. FROM BASE CASE RETURNS

- In the base case, our average 2026-30 all-sector total return is comprised 5.3% p.a. income return, 2.4% p.a. of rental growth and 1.1% p.a. attributed to yield shift.

- This compares to 5.4% p.a. of income return, 2.1% p.a. of rental growth and 0.1% p.a. from yield shift in the downside.

- Most of the damage to the returns in the downside scenario comes from the yield widening and occurs early with partial reversal later in our 5-year forecasting period .

- This means that our overall 5-year period total return in the downside scenario is 7.6% p.a. which is only 1.1% p.a. lower than the 8.7% p.a. forecasted in our base case.

- Across all sectors, rental growth is expected to mostly offset the yield widening of the downside scenario confirming resilience, especially for offices.

- In the downside scenario, logistics and residential markets are showing a negative impact from yield shifts on their total 2026-30 annual returns.

EUROPEAN PRIME TOTAL RETURN FORECAST AND ITS COMPONENTS (2026-30 % p.a.)

For more information, please contact:

HANS VRENSEN CFA, CRE

Managing Director, Head of Research & Strategy Europe

hans.vrensen@eu.aew.com

This material is intended for information purposes only and does not constitute investment advice or a recommendation. The information and opinions contained in the material have been compiled or arrived at based upon information obtained from sources believed to be reliable, but we do not guarantee its accuracy, completeness or fairness. Opinions expressed reflect prevailing market conditions and are subject to change. Neither this material, nor any of its contents, may be used for any purpose without the consent and knowledge of AEW. There is no assurance that any prediction, projection or forecast will be realized.